International Journal of Economics and Finance; Vol. 6, No. 10; 2014

ISSN 1916-971X E-ISSN 1916-9728

Published by Canadian Center of Science and Education

Modeling Volatility in the Gambian Exchange Rates: An

ARMA-GARCH Approach

Sambujang Marreh1,2, Olusanya E. Olubusoye3 & John M. Kihoro4

1

Pan African University, Institute of Basic Sciences Technology and Innovation, Nairobi, Kenya

2

School of Arts and Sciences, University of The Gambia, Brikama, The Gambia

3

Department of Statistics, University of Ibadan, Ibadan, Nigeria

4

Department of Computing and E-learning, Cooperative University College of Kenya, Nairobi, Kenya

Correspondence: Sambujang Marreh, Pan African University, Institute of Basic Sciences Technology and

Innovation, Nairobi, Kenya. Tel: 254-729-393-948. E-mail: smarreh@utg.edu.gm

Received: July 25, 2014

Accepted: August 14, 2014

Online Published: September 25, 2014

doi:10.5539/ijef.v6n10p118

URL: http://dx.doi.org/10.5539/ijef.v6n10p118

Abstract

This paper models the exchange rate volatility in the Gambian foreign exchange rates data. Financial time series

models that combined autoregressive moving average (ARMA) and generalized conditional heteroscedasticity

(GARCH) was explored theoritically and applied to the daily Euro and US dollars (USD) exchange rates against

the Gambian Dalasi (GMD) from 2003 through 2013. Based on Akaike information criteria, the ARMA(1,1)GARCH(1,1) and ARMA(2,1)-GARCH(1,1) were judged the best fitting models to the Euro/GMD and

USD/GMD return series respectively. Our empirical results revealed that the distribution of the return series was

heavy-tailed and volatility was highly persistent in the Gambian foreign exchange market.

Keywords: exchange rates, Gambia, returns, volatility, ARMA, GARCH

1. Introduction

In the last two decades, modelling exchange rates volatility has drawn much attention from researchers.

Exchange rate is one of the salient policy tools for many transitional economies. At the macroeconomic level,

exchange rate fluctuations can have significant impact on trade volume. At the microeconomic level it can affect

firms and individuals involved in international business. Governments especially in developing countries are

continuing to search for mechanisms to cope with the uncertainty that often characterises foreign exchange

markets.

According to Antonakakis and Darby (2012), developing countries are increasingly being regarded as alternative

destinations for foreign direct investments. This change has been accompanied by a huge increase in

international transfers, and in many cases by unexpected changes in exchange rate volatility. Such changes can

be very costly for investors as well as governments if they are unforeseen or inefficiently managed. Volatility of

an exchange rate can be termed as the variation of the price at which two different countries currencies are traded.

It is usually measured as the conditional variance or the conditional standard deviation. Volatility models are

important since they can observe the effect of economic factors on foreign exchange rates and, to policymakers

and governments in formulating policies related to money supply in the economy and those associated with

government expenditures and incomes (Alam & Rahman, 2012).

The Gambian economy is a small open economy in West Africa particularly in terms of basic macroeconomic

indicators. In terms of official exchange rate GDP measure, the economy is a total of 896 million US dollars

(WDI, 2013). Agriculture, including fisheries, is a dominant activity and contributed about 19.7% percent of

GDP in 2013, while industry though small accounts for 12.9% and the main sector of the economic, services

(mainly distributive trade, tourism, transportation and telecommunication) accounted for 67.7% of GDP in the

same year.

Given the small open and import dependent nature of the Gambian economy, the exchange rates is one of the

most important macroeconomic variables. This is manifested as government reserves are kept in foreign currency,

most imports and exports are paid in foreign currency and moreover, the remittances received by many

118

�www.ccsenet.org/ijef

International Journal of Economics and Finance

Vol. 6, No. 10; 2014

Gambians from abroad show that exchange rate is an important component of the monetary transmission process

in The Gambia. The volatility in this price has significant effects on people as well as on policy.

The floating exchange rate system was introduced in the Gambia in 1986 as part of the economic and

restructuring package program from the international monetary fund. This allows the exchange rate against

international currencies such as the US Dollar to be determined by the forces of demand and supply in the

currency market. The Central Bank often intervenes only to maintain the required level of reserves and to

smooth out volatility. There are fourteen banks operating in the Gambia of which thirteen are conventional

commercial banks and one is an Islamic bank. The major trading currency in the inter-bank foreign exchange

market is the US dollar, followed by the Euro and the British Pound. Prolonged volatility in exchange rate is an

indication of ineffectiveness of a central bank to perform its mandate of price stability, and the management of

the countries foreign exchange reserves (Maana et al., 2010).

This paper models the volatility in the Gambian exchange rate returns data. We explore properties of the

Gambian daily exchange rate data and examine ARMA–GARCH models that are suitable to model the returns.

Specifically, an autoregressive moving average is specified as the mean equation while the residuals are fitted

with a symmetric GARCH process. This paper contributes in two ways. First, to our knowledge, no work has

been done on modeling volatility in the Gambian exchange rates, thus the attempt to fill this Gap. Second, we

apply the ARMA (P,Q)–GARCH(p,q) model which is different from previous studies. Many studies assumed that

returns follow a pure GARCH process with a constant mean. This assumption might not be plausible as it is

restrictive that the observed series is a realization of a noise.

A Quasi-maximum likelihood (QML) estimation method is used to estimate our model. Exploratory analysis of

the returns indicates that they are heavy-tailed. Our findings suggest that volatility is highly persistent and the

estimated model fits the exchange rate returns data well. The remainder of this paper is organized as follows:

Section two discusses relevant literature, section three discusses the theoritical framework of the ARMA–

GARCH model considered, section four covers methodology, section five discusses the estimated results, and

section six gives the summary and conclusion.

2. Literture Review

Since the seminal works of Engel (1982) and Bollerslev (1986), generalized autoregressive conditional

heteroscedastic (GARCH) processes have received considerable attention in the analysis of financial time series.

Engel describe the conditional variance by a simple quadratic function of its lagged values, while Bollerslev

modeled the conditional variance to be determined by its own lagged values and the square of the lagged values

of the innovations or shocks. These time series models are known to capture several essential features of

financial series such as leptokurticity and volatility clustering. Empirical studies have shown that such processes

are successful in modeling time series. For example in the context of foreign exchange rate markets see earlier

works by (Bailie & Bollerslev, 1989; Hsieh, 1989). Many of the drivers of dynamics in exchange rate returns and

volatility can best be identified in high frequency data. For more details see (Andersen & Bollerslev, 1998a,b).

According to Choy (2002), knowledge of volatility and its estimation can ensure mitigation of long term risk of

any investment which assists in promoting economic growth since investment is the main channel of increasing

real output and employment.

The GARCH in mean was used by Ryan and Worthington (2004) to investigate the sensitivity of the Australian

Bank stock returns to market interest rate and foreign exchange rate risk. Their results suggest that bank stock

returns is mostly determined by market risk, together with short and medium term interest and foreign exchange

rates.

In Ghana, Adjasi et al. (2008) investigated the influence of exchange rate volatility on stock market returns by

using the exponential GARCH model. They established that there exists a negative relationship between

exchange rate volatility and stock market returns. They argue that a depreciation of the local currency results to

an increase in stock market returns in the long run. Olowe (2009) examines the volatility of Naira/ US Dollar

exchange rates in Nigeria using monthly data over the period 1970 to 2007. Six different univariate GARCH

models were fitted to the data. The paper concluded that all the models show that volatility is persistent for both

the fixed exchange rate period and the floating regime era, and the best performing models are the Asymmetric

Power ARCH and Threshold Symmetric GARCH.

Kamal et al. (2012) modeled exchange rate volatility of the Pakistani Rupee and the US Dollar using three

ARCH type models namely: GARCH in mean model, Exponential GARCH and Threshold ARCH Models.

According to the results of their study, it was concluded that EGARCH model was the best model in explaining

the volatility behavior of exchange rate data of Pakistani Rupee against the US Dollar. A comparative study to

119

�www.ccsenet.org/ijef

International Journal of Economics and Finance

Vol. 6, No. 10; 2014

establish whether the univariate volatility models used widely in modelling and forecasting exchange rate

volatility in developed countries were equally successful when applied to data from developing countries was

done by (Antonakakis & Darby, 2012). Three developing countries were selected and four developed countries.

All exchange rates were against the US Dollar. They found that for developed countries the Fractionally

Integrated GARCH model was superior to the other models whereas in the case of developing countries the

Integrated GARCH model fitted the data better.

All these studies assume that the series follows a GARCH process. This implies the mean equation in their

GARCH models is termed as a constant. To the best of our knowledge, no study on exchange rates is done on

modelling volatility using ARMA-GARCH models. However, these models have been successfully applied to

the energy markets notably the oil and electricity markets. For examples, see (Hickey et al., 2012; Mohammadi

& Su, 2010). Therefore, we investigate whether such models can adequately describe exchange rate price

behavior in the Gambian foreign exchange market.

3. Theoritical Framework

Empirical research on return distribution has been a subject of discussion among researchers since the 1960s.

Badrinath and Chatterjee (1988) and Rachev et al. (2005) have found that the distribution of returns is not

characterized by normality but by the stylied facts of fat-tails, high peakedness (excess Kurtosis) and skewness.

Although it is generally accepted that distribution of exchange rates are leptokurtic and skewed, there is no

unanimity regarding the best stochastic model to capture these empirical studies.We outline the ARMA-GARCH

model below.

3.1 Mean and Variance Equation

In this paper, the mean equation is modeled with an ARMA process. The mean equation used serves as a filter for

the returns. The residuals are then fitted with a GARCH process. Assuming that the returns, r1 ,..., rn are

generated by a strictly stationary nonanticipative solution of the ARMA (P, Q)–GARCH(p, q) order given by

rt − µ = ai (rt −i − µ ) − b j ε t − j + ε t

P

Q

i =1

j =1

ε t = σ t zt

(1)

σ t2 = ω + α i ε t2−i + β j σ t2− j

q

p

i =1

j =1

where p ≥ 0, q > 0, ω > 0, µ is the mean of mean of the return series and zt is an independent and identically

distributed white noise process. Assuming that the orders P, Q, p and q are known, the parameter vector is

denoted by

ϕ = (ϑ ' , θ ')' = (a1 ,..., a P , b1 ,..., bQ , θ '),

where θ ' = (ω , α 1 ,...,α q , β1 ,..., β p ) .

3.2 Estimation of the ARMA(P,Q)–GARCH (p,q) Model

In the absence of normality, Weiss (1986) and, Bollerslev and Wooldridge (1992) have shown that in GARCH

models, maximizing the Gaussian likelihood produces QML estimator that are consistent and asymtotically normally distributed provided that the conditional mean and variance equation are correctly specified. For our case,

we use the ARMA-GARCH process of equation (1) under mild conditions and show the QML estimator (Francq

& Zakoian, 2004).

The parameter space is given by

Φ ⊂ ℜ P + Q +1 × (0,+∞ ) × [0,+∞ ) p + q .

The true value of the parameter is given by

ϕ 0 = (ϑ0 ' ,θ 0 ')' = (a 01 ,..., a 0 P , b01 ,..., b0Q ,θ 0 ').

(2)

With the Gaussian quasi-maximum likelihood conditional on initial values when, for q ≥ Q, then the initial

values are obtained as

~

~

~ 2

~ 2

r1 ,..., r1− (q − Q )− P , ε − q + Q ,..., ε 1− q , σ 0 ,..., σ 1− p ,

the last p of these values are positive and may depend on the parameter or on the observations. For any

120

ϑ , the

�www.ccsenet.org/ijef

In

nternational Jouurnal of Econom

mics and Finance

Vol. 6, No. 10; 2014

~ 2

~

values ε t (ϑ ), t = −q + Q + 1,..., n , and then for any θ, the values of σ t (θ ) for t = 1,..., n is computed

d from

ε t = ε t (ϑ ) = rt − µ − ai (rt −i − µ ) + b j ε t − j

~

Q

P

~

~

σ t = σ t (θ ) = ω + α i ε t −i + β i σ t −i .

i =1

~ 2

~ 2

q

(3)

j=1

~2

i =1

p

~ 2

(4)

j =1

Howeverr, when q < Q,, the fixed inittial values are

~ 2

~ 2

r1 ,..., r1−(q −Q )− P , ε 0 ,..., ε 1−Q , σ 0 ,..., σ 1− p .

Conditionnal on these innitial values, the

t Gaussian L

Log–likelihoo

od is obtained as

~

I n (ϕ ) = n

−1

Lt , Lt = Lt (ϕ ) =

n

t =1

~2

σ t (θ )

+

Log

L

~ 2

σ t (θ )

~2

ε t (ϑ )

(5)

A quasi-m

maximum likkehood estimaator of the paarameter vecttor is defined as any meassurable solutiion of the

equation

~

~

ϕ n = arg m

min I n (ϕ ), ϕ ∈ Φ.

(6)

For the cconsistency annd asymtotic normality prooperties of thiis estimator see

s details froom (Francq & Zakoian,

2010).

4. Methoodology

4.1 Data and Descriptiive Statistics

p

consists of daily exchhange rates off the Gambian Dalasis againnst the Euro and

a the US

The data used in this paper

T data coverr the period fr

from May 200

03 to May 2013. It consistss of 3653 obsservations.

dollar forr ten years. The

The data represents thhe average daiily spot pricess exchange raates at which the

t banks buyy and sell these foreign

currenciees. The data were

w

obtained

d from the C

Central Bank of The Gam

mbia courtesy of AONDA historical

exchangee rate databasee (available at www.oanda.ccom).

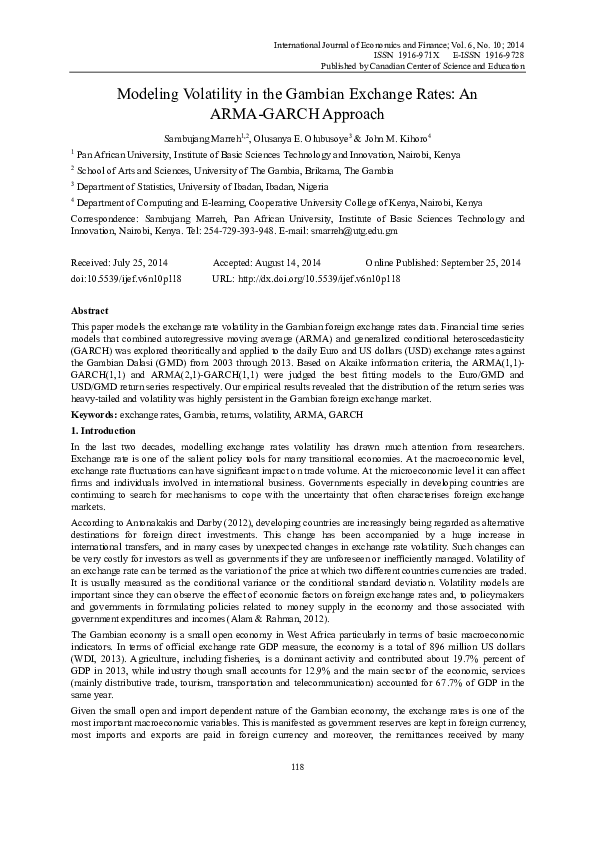

In figure (1), we noticeed that the vaariation in the daily series of

o the Euro an

nd USD currenncies against the Dalasi

is not connstant over tim

me. This is terrmed as nonsttationarity and

d it is widely observed

o

in m

many applied time

t

series

data. Thee movement iss an upward trrend and indiccates that the Dalasi againsst these internnational curren

ncies have

been deprreciating overr the last decad

de. This couldd be attributed

d to many factors. One of w

which include the

t diminishing naature of the country’s re-exp

port trade due to harmonizaation of extern

nal tariffs in thhe region and efficiency

improvem

ments in comppeting port faccilities, notablyy in Senegal.

Figure 1. D

Daily exchange rates plots

121

�www.ccsenet.org/ijef

In

nternational Jouurnal of Econom

mics and Finance

Vol. 6, No. 10; 2014

Since ourr daily exchannge rate series in this study is non stationary as shown in the Augmeented Dickey-Fuller and

Phillips-P

Perron test of stationarity in

n table 1, we nneed to transfform the origin

nal series to reender it statio

onary. This

will enabble us apply thhe time seriess models withhout violating

g the underlyin

ng theory. Wee apply the lo

ogarithmic

transform

mation to convvert the prices to returns. Leet the daily excchange rate seeries be denoteed by, yt, then

n

y

rt = ln t = ln( y t ) − ln( y t −1 ) ,

y t −1

where rt iis the return at

a time t, yt is the exchangee rate price at time

t

t and yt-1 is the exchannge rate at timee t-1.

The returrns series appeear stationary

y over time annd fluctuating around mean zero as show

wn in figure (2

2). We can

also obseerve the volattility clusterin

ng in the plotts. This is ev

vident as perio

od of high voolatility is folllowed by

periods oof low volatilitty thus confirm

ming one of thhe main featurres of stationary financial tim

me series dataa.

Figure 2. L

Logarithmic reeturns plots

Table 1 ggives the statioonarity test reesults for the ddaily and retu

urn series. Botth the Augmeented Dickey-F

Fuller and

the Philliips-Perron testt confirms thee presence of unit root in both

b

daily seriies at the 1% significance level

l

since

their p-vaalues are greatter than or equ

ual to it. For th

the returns, bo

oth tests suggeests stationaritty at the 1%, 5%

5 and 10%

as the p-vvalues associaated with the test

t are all sm

maller than thee respective significance levvels. Thereforre, the null

hypothesees of the preseence of unit ro

oot for each oof the retuns seeries is rejecteed, thus confirrming stationaarity of the

series.

Table 1. A

Augmented dickey–fuller

d

and philips–p

–perron tests for

f unit root

Augmennted – Dickey Fu

uller Test

Daiily Series

Returns

Euro/GMD

USD/GMD

Euro/GMD

D

USD/GMD

D

T Statistic

Test

-3.7078

-1.818

-15.9198

-15.4906

P-value

0.0236

0.6554

<0.001

<0.001

P

Philips – Perron teest

T Statistic

Test

-40.2401

-12.7666

-3733.33

-3714.41

P-value

0.01

0.3978

<0.001

<0.001

The desccriptive statistiics carried ou

ut on the origginal and returrn series are shown

s

in tablle 2. The average daily

exchangee rate of the Euuro and USD against the D

Dalasi from 20

003 to 2013 is 39.391 and 226.947 respecttively. The

excess kuurtosis of the daily

d

series iss 0.419 and 1. 0645 respectively. This imp

plies the distrribution of thee Euro and

122

�www.ccsenet.org/ijef

International Journal of Economics and Finance

Vol. 6, No. 10; 2014

USD against the Dalasi has approximately the same kurtosis as that of a normal distribution which known to be 3.

The excess kurtosis of the returns indicates that they are heavy-tailed (28.973 and 33.319 for the Euro/GMD and

USD/GMD respectively). The excess kurtosis tells us by how much the kurtosis of a variable differs from that of

a normally distributed variable. Therefore, the exact kurtosis of the variables is the value shown in table 2 plus 3.

The mean of both return series is close to zero. The Jarque-Bera test at 1%,5% and 10% significance rejects the

null hypothesis, confirming the departure from normality of the daily and return series for each currency (critical

values are 9.21, 5.99 and 4.61 respectively). The Ljung-Box statistics up to lags 5 allows us to conclude lack of

randomness in the data, which signifies high presence of serial correlation since the p-values are less than 1%, 5%

and 10% significance levels.

Table 2. Descriptive statistics

Daily

Returns

Euro/GMD

USD/GMD

Euro/GMD

USD/GMD

Mean

39.391

26.947

0.00012

0.00008

Median

35.33

27.047

0.00004

0

Maximum

45.647

33.631

-0.18778

0.18781

Minimum

24.024

16.999

-0.22725

-0.22975

Standard Deviation

3.213

2.854

0.01589

0.01532

Excess kurtosis

0.491

1.065

28.973

33.319

Skewness

-0.066

-0.728

-0.57349

-0.657

Jarque Bera Statistic

39.3786

495.2008

122007

169187.4

Jarque Bera P-value

<0.0001

<0.0001

<0.0001

<0.0001

Ljung Box Statistic

17155.91

17621.01

233.959

307.8463

Ljung Box P-value

<0.0001

<0.0001

<0.0001

<0.0001

Number of Observations

3653

3653

3652

3652

4.1 Model Selection

The selection of the best ARMA model to fit the returns as the mean equation is based on the Akaike Information

Criteria (AIC). Several ARMA models were fitted and evaluated based on this criterion. Therefore, AIC is a

measure of the goodness-of-fit of an estimated statistical model. In general, AIC is defined as

AIC = −2 log(L ) + 2k

where log(L) is the maximized likelihood of the parameters for the estimated model, k is the number of

parameters and the term 2k is a penalty as an increasing function of the number of estimated parameters. Given

any two estimated models, the model with the lower value of AIC is the one to be preferred.

In table 3, nine ARMA models were fitted for each of the returns. The ARMA(1, 1) and ARMA(2, 1) appears to

be the best candidates for the mean equation of the Euro/GMD and USD/GMD returns respectively since they

have the AIC lowest values. The mean equations are necessary to remove serial dependence and produce

independent and identically distributed residuals.

Table 3. AIC of several ARMA model for the mean equation

ARMA Model

Euro/GMD Returns

USD/GMD Returns

(0,1)

-19548.1

-19937.71

(0,2)

-19609.1

-20021.65

(1,0)

-19468.2

-19794.08

(1,1)

-19614.3

-20023.81

(1,2)

-19613.2

-20024.09

(2,0)

-19556.3

-19926.8

(2,1)

-19613.2

-20024.23

(2,2)

-19610.9

-20022.11

The ARCH test for heteroscedasticity is conducted on the residuals from the mean equation and the results are

shown in table (4). It is concluded that the residuals from the fitted ARMA (1, 1) and ARMA (2,1) models at the

123

�www.ccsenet.org/ijef

In

nternational Jouurnal of Econom

mics and Finance

Vol. 6, No. 10; 2014

various laags rejects the null hypoth

hesis of no AR

RCH effects. This is becasue the p-valuues obtained are

a all less

than the significant levels

l

at 1%, 5% and 100% respectively. This sug

ggests that a GARCH model

m

may

appropriaately describe the conditional volatility prrocess.

Table 4. A

ARCH Test for

f heterosced

dasticity at 5%

% significancce level

Euuro ARMA(1,1) Residual

R

US

SD ARMA(2,1) Residuals

R

Laag

Test Statiistic

P-value

e

4

144.51

<0.001

Critical Vaalue

9.488

8

241.96

6

<0.001

15.5077

122

246.64

4

<0.001

21.0266

4

145.52

2

<0.001

9.488

8

224.04

4

<0.001

15.5077

122

231.2

2

<0.001

21.0266

Note. The A

ARCH statistic tesst the null hypoth

hesis of no condittional heteroscedaasticity.

From thee graphs of thee autocorrelation function oof the residuaals in Figure 3, it is seen thaat there existss only two

significannt spikes at arround lags 2 and 7 for both series. The PA

ACFs exhibitss several signiificant notably

y at lags 6

and 15. F

For the ACFss and PACFs in

i both residuuals it clearly

y indicates an exponential ddeclining of the

t spikes.

This sugggests a GARC

CH process is an

a ideal candiidate to modell the residual. From the grapphs, it is obseerved there

is no patttern of seasonnal lags being present. Thuss, the assumpttion of no seaasonality in thhe returns is pllausible to

assume.

Figgure 3. ACF AND

A

PACF pllots of the resiiduals from th

he mean equattion

GARCH amon

ng competing models is bassed on the AIIC as well.

The technnique used in selecting the appropriate G

In empiriical applications, only smalll lag for p andd q are often used.

u

Typically

y, GARCH (1 , 1), GARCH (1, 2) and

GARCH (2, 1) are adeequate in modeling volatilitiies in financiaal time series over

o long sam

mple periods (Bollerslev

et al., 19992).

In table 55, we include other GARCH models to check if they could be favourable modeels in modelin

ng the heteroscedassticity in our data. It is ev

vident from tthe table thatt the GARCH

H (1,1) comess out to be th

he best in

modelingg the residuals in both return

n series.

Table 5. A

AIC GARCH

H Model fitted

d to the residuuals

(1,0)

(1,1)

(1,2)

(2,0)

(2,1)

(2,2)

Residuals 1

-5.19612

-5.2114

-5.21018

-5.19603

-5.2109

-5.21139

Residuals 2

-5.20023

-6.22128

-5.21931

-6.20015

-5.22092

-5.22124

124

�www.ccsenet.org/ijef

International Journal of Economics and Finance

Vol. 6, No. 10; 2014

Therefore, based on the analysis and selection criteria, we apply the ARMA(1,1)-GARCH(1,1) to the Euro/GMD

returns whilst the USD/GMD is fitted with an ARMA(2,1)-GARCH(1,1).

5. Empirical Results

We estimate the selected models using the Quasi-maximum likelihood estimation method. The estimated coefficients for both the conditional mean and variance are contained in Tables (6). In both returns, the autoregressive

and moving average terms sum to a number less than 1, which is consistent with a stationary ARMA process.

The AR (1) and MA (1) terms are statistically significant at the 1%, 5% and 10% for both exchange rates. The

coefficient for AR (2) is not significant at the 1% for the USD/GMD returns.

The sum of the GARCH parameters is approximately equal to one for all the models i.e., α1 + β1 ≈ 1. This shows

that volatility is persistent in our exchange rate data which is consistent with the findings of Beg and Anwar

(2012) for the U.K. pound/ U.S dollar daily exchange rates. The coefficient α1 captures the influence of new

shocks on volatility. Estimates of this parameter are statistically significant for both currencies and positive. The

estimate, α 1 , from the fitted model is close to 0.085 for both returns. The parameter β1, measures persistence of

volatility shocks and is positive as well as statistically significant. For both returns, value of β1 is close to 1

(around 0.93), indicating that old shocks to exhange rate prices tend to persist, instead of dying out quickly. This

implies that economic shocks especially those of external have long standing effects on exchange rate volatility

in the Gambia.

Table 6. Estimates of the conditional mean and variance equation

Euro/GMD

USD/GMD

Parameter

ARMA(1,1) – GARCH(1,1)

ARMA(2,1) – GARCH(1,1)

AR(1)

0.0579

0.4815

(<0.001***)

(<0.001***)

AR(2)

-0.0764

(0.0199**)

MA(1)

ω

α1

β1

-0.7479

-0.7542

(<0.001***)

(<0.001***)

0

0

-0.152

(0.003***)

0.0913

0.0871

(<0.001***)

(<0.001***)

0.9261

0.9262

(<0.001***)

(<0.001***)

LM-ARCH Test on Residuals

Test Statistic

2.3441

4.134

P-value

0.9987

0.9806

Note. The values in parenthesis are the p-values of the coefficients. *** represent significance at the 1%,5%, 10% levels, while

significance at 5% and 10% respectively. The ARCH-LM test is up to 20 lags.

**

denotes

The LM-ARCH test results together with AIC and BIC for the residuals is also given. The ARCH test for

heteroscedasticity accepts the null hypothesis of no ARCH effects in the residuals because the p-values are all

greater than than 1%, 5% and 10% respectively. Moreover, if the model is successful in modeling the return

series well, then there should be minimal or no autocorrelation left in the standardized residuals. The graphs in

Figure 4, shows that the standardized residuals are white noise and the autocorrelation function of the squared

residuals indicates that there is no significant autocorreation in the residuals of the estimated models.This suggest

that the model fits our data well.

125

�www.ccsenet.org/ijef

In

nternational Jouurnal of Econom

mics and Finance

Vol. 6, No. 10; 2014

Figure 4. Sttandardized reesiduals plots

onditional vaariance which is an unbiassed estimate oof the true conditional

The volaatilities estimaated as the co

variance from the estim

mated models are plotted annd shown in Figure

F

5. In alll the plots thee volatility paattern does

not exhibbit constant inncrease or decrease but insttead a mixturee of periods of high volatiliity followed by

b periods

of low voolatility. This suggests that the Gambian foreign exchaange rates durring the last teen years have witnessed

significannt instability.

Figure 5. E

Exchange ratee volatilities

usion

6. Conclu

The properties of the Gambian

G

exchange rate dataa have been ex

xplored and a suitable ARM

MA-GARCH model

m

was

formulateed and applieed to it. Bassed on AIC criterion, thee ARMA(1,1)-GARCH(1,11) was applied to the

Euro/GM

MD returns andd for the USD

D/GMD returnns, an ARMA

A(2,1)-GARCH

H(1,1) was fitttted to it. The theory on

Quasi-maaximum likeliihood estimatiion of ARMA

A-GARCH waas evaluated before applyingg the model to estimate

volatilitiees in the Gambbian exchangee rates. The suum of the GA

ARCH parameters, α1 and β11 were found to be very

close to 11, suggesting that

t volatility in the exchannge rates is hig

ghly persistentt.

The volattility in the Gambian

G

exchaange rates wittnessed signifi

ficant instability during the last decade in

n the form

of deprecciation of the currency. Thiis suggests thhat exchange rate

r volatility (which is asssociated with exchange

126

�www.ccsenet.org/ijef

International Journal of Economics and Finance

Vol. 6, No. 10; 2014

rate risk) in the Gambian market is high. This risk is important to understand as it affect transactional account

exposure related to receivables (export contracts), payables such as import contracts and repartriation of

dividends. It also impact revenues on domestic sales and inputs and also, on operating cost. Therefore, the results

of this paper provides an avenue for understanding the volatility associated with the Gambian foreign exchange

market which provides a good avenue to relevant authorities and other parties in managing currency risk. It may

be of interest to future researchers to use a Multivariate GARCH model that could include fundamental

macroeconomic variables such as interest and inflation rates and also, to explore the concept of regime switching

to increase the overall fit of the models.

Acknowledgments

The authors would like to thank the African Union Commission through PAUISTI for providing financial and

logistical support during the course of conducting this research. Special appreciation also goes to the Central

Bank of The Gambia for granting us access to their library resources.

References

Adjasi, C., Harvey, S., & Adyapong, D. (2008). Effects of exchange rate volatility on the Ghana stock exchange.

African Journal of Accounting, Economics, Finance and Banking Research, 3, 28–47.

Alam, Z. M., & Rahman, A. M. (2012). Modeling volatility of bdt/usd exchange rate with GARCH models.

Journal of Economics and Finance, 3(11).

Andersen, T. G., & Bollerslev, T. (1998a). Answering the skeptics: Yes, standard volatility models do provide

accurate forecasts. International Economics Review, 39(4), 885–905. http://dx.doi.org/10.2307/2527343

Andersen, T. G., & Bollerslev, T. (1998b). Deutsche mark-dollar volatility: Intraday activity patterns, macroeconomic announcements and larger dependencies. Journal of Finance, 53(1), 219–265.

http://dx.doi.org/10.1111/0022-1082.85732

Antonakakis, N., & Darby, J. (2012). Forecasting volatility in developing countries. MPRA Paper.

Badrinath, S. G., & Chatterjee., S. (1988). On measuring skewness and elongation in common stock distributions:

The case of the market index. Journal of Busness, 61, 451–472. http://dx.doi.org/10.1086/296443

Bailie, R. T., & Bollerslev, T. (1989). The message in daily exchange rates: A conditional variance tale. Journal

of Business and Economic Statistics, 7(3), 297–305.

Beg, R. A., & Anwar, S. (2012). A case study of the UK pound/U.S. dollar exchange rate returns. North

American Journal of Economics and Finance, 23, 165–184. http://dx.doi.org/10.1016/j.najef.2012.02.001

Bollerslev, T. (1986).Generalized autoregressive conditional heteroscedasticity. Journal of Econometrics, 31,

307–327. http://dx.doi.org/10.1016/0304-4076(86)90063-1

Bollerslev, T., & Wooldridge, J. M. (1992). Quasi-maximum likelihood estimation and inference in dynamic

models

with

time-varying

covariances.

Econometric

Reviews,

11(2),

143–172.

http://dx.doi.org/10.1080/07474939208800229

Bollerslev, T., Chou, T. Y., & Kroner, K. F. (1992). ARCH modelling in finance: A selective review of the theory

and

empirical

evidence.

Journal

of

Econometrics,

52,

5–59.

http://dx.doi.org/10.1016/0304-4076(92)90064-X

Choy, M. (2002). The developments of debt mmarket in Peru (p. 11). Bank for International Settlement (BIS).

Engel, R. F. (1982). Autoregressive conditional heteroscedasticity with estimates of the United Kingdom

inflation. Econometrica, 50(4), 987–1007. http://dx.doi.org/10.2307/1912773

Francq, C., & Zakoian, J. M. (2004). Maximum likelihood estimation of pure GARCH and ARMA-GARCH

processes. Bernoulli, 10(4), 605–637. http://dx.doi.org/10.3150/bj/1093265632

Francq, C., & Zakoian, J. M. (2010). GARCH Models: Structure, Statistical Inference and Financial

Applications (1st ed.). Wiley and Sons Inc. http://dx.doi.org/10.1002/9780470670057

Hickey, T., Loomis, D. G., & Mohammadi, H. (2012). Forcasting hourly electricity prices using

ARMAX-GARCH models: An application to MISO hubs. Energy Economics, 34, 307–315.

http://dx.doi.org/10.1016/j.eneco.2011.11.011

Hsieh, D. A. (1989). Modeling heteroscedasticity in daily foreign exchange rates. Journal of Business and

Economic Statistics, 7(3), 301–317.

127

�www.ccsenet.org/ijef

International Journal of Economics and Finance

Vol. 6, No. 10; 2014

Kamal, Y., Ul-Haq, H., & Khan, M. M. (2012). Modelling exchange rate volatility using generalized autoregressive conditional heteroscedasticity (GARCH) type models: Evidence from Pakistan. African Journal of

Business Management, 6(8), 2830–2838.

Maana, I., Mwita, P. N., & Odhiambo, R. (2010). Modelling the volatility of exchange rates in the kenya markets.

African Journal of Business Management, 4(7), 1401–1408. http://dx.doi.org/10.1016/j.eneco.2010.04.009

Mohammadi, H., & Su, L. (2010). International evidence on crude oil price ddynamic: Application of

ARIMA-GARCH models. Energy Economics, 32, 1001–1008.

Olowe, R. A. (2009). Modelling Naira/Dollar exchange rate volatility: Application of GARCH and asymmetric

models. International Journal of Busines Research Papers, 5(3), 378–398.

Rachev, S. T., Menn, C., & Fabozzi, J. M. (2005). Fat Tailed and Skewed Asset Distributions. New York: Wiley.

Ryan, S. K., & Worthington, A. C. (2004). Market, interest rates and foreign exchange rate risk in australian

banking. a GARCH-m approach. International Journal of Applied Business and Economic Research, 2(4),

81–103.

WDI. (2013). World Development Indicators. World bank.

Weiss, A. A. (1986). Asymtotic theory for arch models: Estimation and testing. Econometric Theory, 2(1), 107–

131. http://dx.doi.org/10.1017/S0266466600011397

Copyrights

Copyright for this article is retained by the author(s), with first publication rights granted to the journal.

This is an open-access article distributed under the terms and conditions of the Creative Commons Attribution

license (http://creativecommons.org/licenses/by/3.0/).

128

�