Prevalence of investor and analyst presentations on investor

relations webpages – an industry analysis

L Esterhuyse

University of South Africa

Corresponding author:

Dr. L Esterhuyse

University of South Africa

E-mail address:

esterl@unisa.ac.za

Keywords:

Information Asymmetry, Investor and Analyst Presentations, NonTextual Cues, Johannesburg Stock Exchange, Investor Relations

ABSTRACT

Recent behavioural research indicate that non-textual cues are relayed during investor and

analyst presentations that influences investors’ judgement. The first objective of this study was

to investigate to what extent Johannesburg Stock Exchange (JSE) listed companies provide

media from these presentations on their investor relations webpages. A second objective was

to determine whether industry differences exist in the availability and usability of these

presentations on the webpages. Findings indicate that although many companies provided

PDFs of slides and handouts of presentations, very few provided audio or visual recordings of

these events. No significant industry association could be discerned, although Basic

Resources companies performed best. This study highlights that JSE-listed companies were

not making the most of available investor communication channels to convey subtle nontextual information cues. Institutional investors and analysts participating in presentations

have informational advantages over retail investors who have to rely on textual reports, if any.

INTRODUCTION

Verbal communication is used daily by billions of people for various purposes. Laughlin (1995:

78) suggests that we “use language to make public what we are doing and why we are doing

it and, where we need to convince”. If language is used for general communication, then

accounting is “a special-purpose tool for communicating about financial status and

performance” (Bloomfield, 2008: 433). Investors use value-relevant information provided by

companies themselves, investment analysts and the financial press to make buy, hold or sell

decisions.

Information is the lifeblood of the capital markets. Investors risk their hard-earned capital in

the markets in great measure based on information they receive from their target companies.

They need reliable information on a timely basis. They want it in language they can

understand, and they should receive it in formats they can easily use for analysis. (DiPiazza

Jnr & Eccles, 2002: 9).

Hedlin (1999) argues that companies use the internet for communicating with investors in

ways that cannot be achieved with printed reports alone. This can be achieved by providing

audio and video information on the website, as well as hyperlinks between information, e.g.

loans in the balance sheet linked to the note describing duration and interest rates. Institutional

30

�investors, such as pension funds and insurance companies have access to analysts’ reports

about the prospects and risks of the companies they invest in. Institutional investors are invited

to presentations by the company to the investment community. Analysts have conference calls

with management after release of periodic results where there are question-and-answer

sessions about the results and future prospects of the company. Historically, retail investors

were not privy to these information sessions.

Following financial scandals such as Enron and Parmelat, regulations have been implemented

in most equity markets since the early 2000s to provide equal and simultaneous access to

information to all shareholders. The Organisation for Economic Co-operation and

Development (OECD) proposes in their G20/OECD Principles of Corporate Governance that

“simultaneous reporting of material or required information to all shareholders in order to

ensure their equitable treatment” is an important principle (OECD, 2015: 37). They also

caution that “In maintaining close relations with investors and market participants, companies

must be careful not to violate this fundamental principle of equitable treatment” (OECD, 2015:

37).

Changes in internet technology now enables companies to archive audio and visual recordings

of results announcements and roadshows with institutional investors on their websites where

it is accessible by anyone. This is in line with the OECD’s principle that “Channels for

disseminating information provide for equal, timely and cost-efficient access to relevant

information by users” (OECD, 2015: 44).

The purpose of this paper is thus to determine to what an extent Johannesburg Stock

Exchange (JSE) listed companies provide archives of interactions with institutional investors

and analysts on their investor relations (IR) webpages. This analysis also entails noting the

format in which this information is provided and the ease of use (or usability) of the information

provided. Secondly, it investigated whether industry differences exist in the prevalence of the

presentations on the IR webpages. The study was executed by visiting webpages of a sample

of JSE-listed companies and comparing it to best practices for investor presentations on the

internet. Companies were coded by industry and analyses of variances were conducted to

determine if significant industry variances exist. The rest of the paper consists of the literature

review, the research questions, the methodology followed, the discussion of results, practical

recommendations to management and conclusions.

LITERATURE REVIEW

This study’s theoretical foundation is based on the theories around information asymmetry.

Shareholders of a large listed company are not involved in the day-to-day management of the

company, and hence they lack detailed knowledge of the company's operations, strategies,

markets and finances. In the case of a company, there are two forms of information

asymmetry. The first form arises between different investors in the company, for example,

when existing shareholders want to sell their shareholding because they are aware of certain

adverse trading conditions, but potential buyers of this shareholding are not aware of these

conditions. A second form of information asymmetry occurs between the owners of a company

(current and potential shareholders) and its managers (the board of directors and other

managers). Companies communicate with the capital market participants to reduce

information asymmetry.

Akerlof (1970) demonstrated how information asymmetry in the form of uncertainty regarding

quality could lead to adverse selection where the under-informed buyer would only be willing

to pay a lower average price for a product or service in an attempt to minimise potential future

losses (in case the product/service turns out to be of low quality). Akerlof (1970) further found

that the number of market participants declines when information about quality is uncertain or

scarce, which in turn implies that a seller may have to accept a lower price in conditions of

31

�illiquidity or in an inactive market. The discount on the optimal price (which could have been

achieved between two fully informed participants) is referred to as the cost of information

asymmetry. It follows then that management of a company would want to disclose more

information to the capital market to indicate the good quality of the company, its management

and its prospects in order to improve the share price and its trading liquidity.

Spence (1973) added to Akerlof’s (1970) work by showing how management could incur

signalling costs by voluntarily communicating more information to under-informed parties

(current and potential shareholders, and debt providers). Examples of these signalling costs

include paying a dividend (signalling confidence about the future cash flow generation

capability of the company), employing a Big 4-audit firm (signalling high quality reporting

mechanisms), or holding investor days to communicate with investors and analysts, or

investing in a good IR website and annual report (signalling transparency). Holland, Krause,

Provencher and Seltzer (2018: 263) comment that “[t]ransparency has long been considered

a normative goal for organizations to pursue in the interest of acting ethically, demonstrating

accountability, and building positive reputational and experiential relationships with

stakeholders”. How, what, to whom and when a listed company communicates with the capital

market is regulated by the exchange on which its equity is listed.

Comparing the disclosure regime of the SEC to the JSE

Historically, institutional investors (investment funds, pension funds), block-holders, and

analysts had access to sources of information such as analyst presentations (via road shows),

conference calls, and one-on-one meetings with the management of the investee company,

while private or individual shareholders did not have such access. These “back room” or

private channels of communication were criticised for denying individual (or private)

shareholders access to relevant information (exacerbating information asymmetry between

investors) and for delays before privileged (value relevant) information was made public

(Solomon & Soltes, 2015; Bushee, Matsumoto, & Miller, 2004). The Securities and Exchange

Commission (SEC) in the US, and the Johannesburg Stock Exchange (JSE) Listings

Requirements addressed the issue of unequal access with revised regulations in the early

2000s.

Regulation Fair Disclosure (US)

Following the financial scandals of Enron and Worldcom, the SEC in the US implemented

Regulation Fair Disclosure (known as Reg FD) on 23 October 2000 (SEC, 2000). This

prohibits companies from privately disclosing value-relevant information to selected securities

markets professionals without simultaneously disclosing the same information to the public.

Rule 101(e) stipulates that the company’s website and the internet (for example, webcasting

or a conference call) may be used as part of a process to provide equal and simultaneous

access to material information (SEC, 2000).

Various researchers have studied the effect of Reg FD on voluntary disclosure via private

channels. Ke, Petroni and Yu (2008) established that transient institutional investors (shorthorizon) previously sold off shares a quarter before bad news broke (after a series of quarterly

earnings increases). However, after Reg FD came into effect, the abnormal selling off before

the breaking of bad news stopped. Like Ke at al. (2008), Ramalingegowda (2014) reported

that long-horizon institutional investors sold off significantly fewer investments in companies

where bankruptcy was imminent after the implementation of Reg FD than before. In the period

before Reg FD, these investors would use their private information to project potential

bankruptcy, and sell their holdings at least a quarter before the bankruptcy filing took place.

Other studies found that the public information environment was enriched after Reg FD came

into effect. Lee, Strong and Zhu (2014) found that the mispricing of US stocks declined after

32

�the implementation of Reg FD. This effect was stronger for companies that had a poor

information environment before the regulation was implemented. Kirk and Vincent (2014)

reported that companies with established professional IR departments more than doubled

their public disclosure after the implementation of Reg FD. These companies also experienced

a post-Reg FD increase in analyst following, institutional shareholders, and liquidity.1

Despite some of the positive findings described here, other researchers had lingering doubts

about whether the private disclosure channels had really been shut off. Soltes (2014:259)

comments:

Despite the passage of Reg FD, analysts can still become more informed by

speaking with management. While Reg FD restricts managers’ ability to convey

material information, analysts are legally permitted to acquire pieces of

nonmaterial information from management. When used in conjunction with an

analyst’s other sources of information, this information may become material in an

information ‘mosaic’.

Brown, Call, Clement and Sharp (2015), found that information gathered by sell-side analysts

during private conversations (mostly telephone calls) with management was more useful for

their earnings forecast accuracy than their own primary research (Brown et al., 2015: 10). One

can conclude that despite the implementation of Reg FD in the US, retail shareholders in the

US might still not face a level playing field with analysts and institutional investors.

Disclosure regulations of the JSE

Similar to Reg FD, the JSE also prohibits companies from releasing information that might

influence the share price to selected parties only. This is stipulated in Regulations 3.4 to 3.8

of the JSE Listings Requirements, which came into effect on 1 September 2003 (JSE, 2011).

If information is released, it should be released via a public medium accessible to everybody

at the same time. Furthermore, Regulation 3.46 of the JSE Listings Requirements determines

that after publishing announcements via the Stock Exchange News Service (SENS),

companies are allowed to post the information on their websites and in the general news

media (JSE, 2011). The use of the company website as a channel for disseminating

information is also supported by the OECD (2015: 44).

The prohibition of private disclosure was recently reinforced with specific guidance on how

management should handle discussions with financial journalists and investment analysts

without releasing value-relevant information by chance (JSE, 2015). Of particular relevance

are the following guidelines:

•

•

During discussions with analysts, issuers are allowed to expand on information

already in the public domain or discuss the markets/industry in which they

operate, provided that such expanded disclosure does not qualify as price

sensitive information. Therefore, issuers must decline to answer questions from

analysts where the answer would lead to divulging price sensitive information. In

responding to certain comments or views from analysts which appear to be

inaccurate, issuers should respond with information drawn from information

released publicly to the market through SENS (JSE, 2015:2).

Issuers must not correct draft reports from analysts which are sent to them with

a view to commenting on financial figures and/or assumptions. The issuer may

consider the financial figures and/or assumptions and discuss them with the

analyst, in broad terms and without providing any price sensitive information.

1

For a comprehensive discussion of the many studies on the effect of Reg FD, see the literature review

by Lee et al. (2014).

33

�•

•

Issuers can of course correct information in relation to financial figures and/or

assumptions that do not constitute price sensitive information and drawn from

information released publicly to the market through SENS (JSE, 2015:3).

Body language: Spokespersons must be mindful of body language when

answering questions. As an example, the shake of a person’s head in a ‘yes’ or

‘no’ gesture or showing thumbs up or down in a ‘positive’ or ‘negative’ gesture,

does constitute communication when answering questions although not in a

verbal format (JSE, 2015:3).

Responding to financial projections and reports: Issuers must confine comments

on financial projections by analysts to errors in factual information and underlying

assumptions that do not constitute price sensitive information. Avoid any

response which may suggest that the current projections of an analyst are

incorrect (JSE, 2015:4).

The JSE further recommends that companies institute a written policy for handling confidential

and price sensitive information (JSE, 2015: 3). Provisions against insider trading are also

contained in sections 77 to 82 of the Financial Markets Act, No. 19 of 2012 (RSA, 2012). The

JSE’s Regulations 3.4 to 3.8 and 3.46 paved the way for the company’s website to become a

channel for simultaneous “publication” (after publication via SENS) of value-relevant

information, as well as a “repository” of previous SENS and other news releases.

Corporate governance of boards in South Africa was also strengthened by the principles

contained in the King III Code of Governance Principles, effective from 1 March 2010 (IoD,

2009). Principle 8.4 requires that “Companies should ensure equitable treatment of

shareholders” and Recommended Practice 8.4.2 specifically requires that “The board should

ensure that minority shareholders are protected”. In terms of communication, Principle 8.5

states that “Transparent and effective communication with stakeholders is essential for

building and maintaining their trust and confidence”. Recommended Practice 8.5.3 proposes

that “The board should adopt communication guidelines that support a responsible

communications programme”. In the spirit of King III, I argue that a responsible company would

protect the interests of its minority shareholders (including retail or private shareholders) by

communicating in a way that does not disadvantage them, in this case by providing access to

media and other recordings of interactions with institutional investors and analysts.

Effect of tone and other non-textual cues on investor judgement

The regulations described above necessitate disclosures in written format first (or only), by

posting a SENS text announcement and then announcements in the financial press. Various

studies, however, indicate audio and visual communication have an effect on investor

judgment about a company. Basoglu and Hess (2014: 82) manipulated corporate IR

webpages in a 2 x 2 experiment (high vs no online media content, while keeping financial

information constant) and found significantly increased trust and perceptions of investment

quality in companies with a higher media content on their IR webpages. Lee (2016) analysed

the conference calls of US companies and found that where management stuck to a

predetermined script and lacked spontaneity in answering questions, it invoked a negative

sentiment with the analysts that results in a downward forecast of future earnings (Lee, 2016:

247). Borochin, Cicon, DeLisle and Price (2018) analysed the tone of management and the

analysts’ discussions in quarterly earnings conference calls of US companies. It was found

that where the tone (e.g. positivity) differs between management and analysts, it contributes

to market uncertainty (Borochin et al, 2018: 15). Investors were also less willing to invest when

the CEO was humble during a conference call vis-à-vis bragging, but the opposite occurred

when the communication channel was Twitter (Grant, Hodge & Sinha, 2018: 7).

34

�PROBLEM INVESTIGATED

Assuming retail investors have access to the same textual information as institutional investors

and analysts (reports, press announcements), prior studies indicate that other information

cues might be conveyed during results announcements, conference calls, investor roadshows

etc. that affect investors’ judgements (Borochin et al, 2018; Grant, Hodge & Sinha, 2018; Lee,

2016; Basuglo & Hess, 2014). By providing an audio and/or video recording of these

presentations on their IR webpages, companies are increasing transparency and levelling the

playing field for retail investors. The purpose of this study was to determine whether, and to

what extent, JSE-listed companies archive these recordings and related information on their

IR webpages.

RESEARCH OBJECTIVES

The first research objective was to determine to what extent JSE-listed companies use their

IR webpages to archive investor presentations. Apart from posting value-relevant information

via the JSE SENS and press releases (JSE, 2011), companies are not under any obligation

to archive investor presentations in any format. This paper argues that willingness to do so,

speaks to the company’s commitment to be transparent and accessible to retail shareholders

as well as to institutional investors. The second research objective was to determine whether

industry differences exist in the prevalence of investor and analyst presentations on the IR

webpages.

RESEARCH METHODOLOGY

This study used secondary data collected during a larger study. The websites of 205 JSElisted companies were visited during July to mid-September 2012 to collect the data2. This

period is of interest as it coincided with the first or second financial years after the

implementation of King III with its requirements for equitable treatment of all shareholders and

transparent communication (IoD, 2009).

Websites were analysed, based on best practice recommendations by the Investor Relations

Society (IRS) in the UK (IRS, 2012) as well as that of Loranger and Nielsen (2009). The

presence of an item or format type was coded “1” and the absence of it “0”. A score/percentage

was obtained by dividing the number of available items by the total best practice criteria for

that category. Separate scores were obtained for presentations relating to Results

Announcements (six criteria), Conference Calls (four criteria), Roadshows (five criteria) and

Annual General Meetings (AGMs) (six criteria). Usability features for presentations on the

websites were also assessed (eight criteria). Lastly, an overall presentation score/percentage

was calculated for all presentation types and usability of the available formats (denominator =

29).

Industry data for each company was obtained from the IRESS database. Telecommunications

(three companies), oil and gas (two companies), and health services (seven companies) had

too few cases to justify being in separate industry classes. These companies’ main segments

were reviewed in their annual reports, and reclassified into industrial, technology, or consumer

services. The final statistical analyses were therefore done with six industry classifications.

Statistical analyses were conducted in SPSS 24.

2

Selective investor relations data were initially reported in Esterhuyse & Wingard (2016). Refer to

Esterhuyse & Wingard (2016) for more detail about the sampling process.

35

�RESULTS AND DISCUSSION

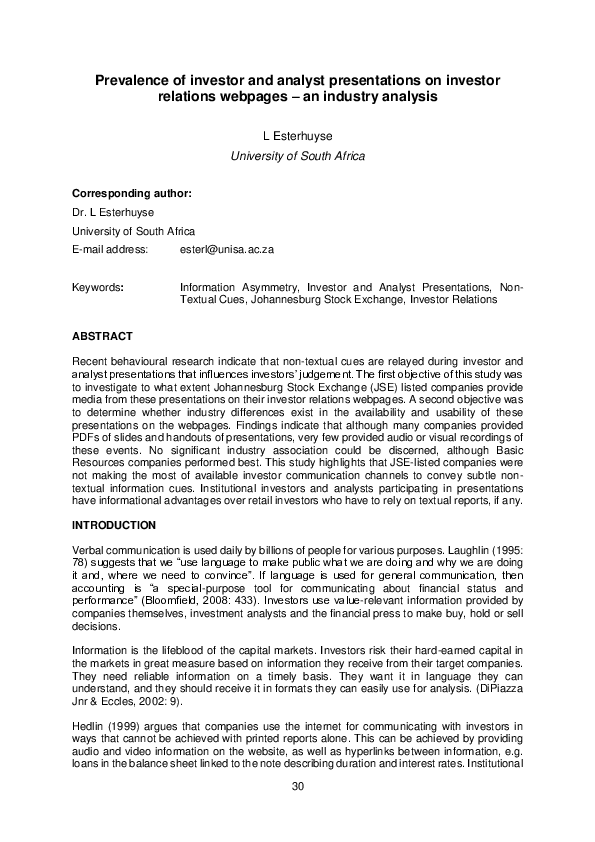

The mean score for the prevalence of investor and analysts presentations on IR webpages of

the 205 JSE-listed companies came to 19.90 per cent. Thirty-one companies scored zero with

no presentation formats available on their websites. It is encouraging that 85 per cent of

companies did provide some information relating to investor presentations, although it is clear

that best practices are not followed. The highest presentation score was 69.97 per cent for

Sasol Ltd. From the frequency distribution in Figure 1, we can see that the distribution is

positively skewed and with quite a wide standard deviation of 16.81 per cent. The mode is

composed of 38 companies that achieved presentation scores of between 20 and 25 per cent.

FIGURE 1:

Frequency distribution of presentation scores

35

Mean

38

40

31 30

30

13

15

13 13 12

8

10

6

3

5

6

3

2

0

Presentation Score

Source: Own from SPSS

TABLE 1:

Availability of presentations per industry

Basic Materials

Consumer Goods

Consumer Services

Technology

No

presentations

Presentations

Total

5

11.9%

16.1%

0

0.0%

0.0%

8

19.0%

25.8%

8

20.0%

25.8%

6

12.8%

19.4%

4

33.3%

37

88.1%

21.3%

22

100.0%

12.6%

34

81.0%

19.5%

32

80.0%

18.4%

41

87.2%

23.6%

8

66.7%

42

100.0%

20.5%

22

100.0%

10.7%

42

100.0%

20.5%

40

100.0%

19.5%

47

100.0%

22.9%

12

100.0%

36

70%

65%

60%

55%

50%

45%

40%

35%

30%

25%

20%

15%

10%

5%

0

0%

No of companies

20

Industrials

Min

0.00%

Max

68.97%

Std Dev

16.81%

27

25

Financials

19.90%

�Total sample

No

presentations

12.9%

31

15.1%

100.0%

Presentations

Total

4.6%

174

84.9%

100.0%

5.9%

205

100.0%

100.0%

The 1st row in every industry represents the number of companies with/without presentations.

The 2nd row represents the proportion of companies in that industry with/without presentations.

The 3rd row represents the proportion of companies in the column with/without presentations (shaded).

Source: Own from SPSS

I now turn to a discussion of the results of the different types of investor and analyst

presentations. Companies release their periodic financial results via press releases and in

many cases via webcasts by management. Table 2 indicates that just under half of the sample

provided at least a PDF copy of the press release in the financial press on their website. Next

popular was the Powerpoint slides of the results announcement at 40.49 per cent. Only about

a fifth of the companies provided an audio or video track of the results announcement, and

only eleven companies provided a transcript of the presentation. The means score for Results

Announcements on IR webpages is 25.93 per cent, driven mostly by the Basic Materials and

Consumer Goods industries, as can be seen from Figure 2. The lowest mean score is in the

Technology industry at 19.4 per cent. However, a one-way ANOVA indicates no significant

differences between the industries for Results Announcements (F(5, 199) = 1.647, p = 0.149)

assuming equal variances.

TABLE 2:

Results announcements on websites

Criteria

Results announcements as audio

Results announcements as video

Results announcements as PPT

Results announcements as PDF of press release

Results announcements as HTML of press release

Results announcement audio track transcription

Mean score

Available

45

41

83

99

40

11

(N = 205) %

21.95

20.00

40.49

48.29

19.51

5.37

25.93

Source: Own from SPSS

FIGURE 2:

Industry means for results announcements

Source: Own from SPSS

Many companies hold separate conference calls with analysts the day after the results were

announced, or for other announcements. From Table 3 we can see that the prevalence of

archiving these calls on the company’s website is very low. Only ten companies provided a

37

�podcast/audio recording of the conference call and only four had it transcribed. From Figure 3

we can see that once again, the Basic Materials industry is doing the best, and the Technology

industry was second best. The one-way ANOVA, rejecting equal variances, indicates that

there were no significant industry differences (Welch F(5, 199) = 1.825, p = 0.121).

TABLE 3:

Conference calls on websites

Criteria

Available

(N = 205) %

Dial in to conference call with analysts

10

4.88

Dial in to conference calls for other events

8

3.90

Podcast of conference call available

10

4.88

Conference call transcribed

4

1.95

Mean

3.90

Source: Own from SPSS

FIGURE 3:

Industry means for conference calls

Source: Own from SPSS

A company’s AGM is open to all registered shareholders or their proxies. This is an important

event as the results for the past year are discussed and directors and auditors are up for reelections and re-appointment. Other business decisions might also be voted upon at the AGM.

Table 4 indicates that very few companies provide a recording of the AGM on their website.

As with the Results Announcement, the most prevalent item is the PDF of the handout or

booklet. Only six companies provided the results of the voting that took place on their website

and even less provided an audio or video recording of events. This is disappointing, as one

would think that companies could at least provide recordings for the AGM as important

decisions are made regarding the management of the company. Figure 4 indicates that the

Consumer Goods and Industrial companies performed better in this area. The one-way

ANOVA, rejecting equal variances, indicates that there were no significant industry differences

(Welch F(5, 199) = 0.542, p = 0.744).

38

�TABLE 4:

AGMs on websites

Criteria

Available

(N = 205) %

AGMs as audio

3

1.46

AGMs as video

2

0.98

AGM's PPT

5

2.44

AGM's PDF of handout/booklet

10

4.88

Results of voting: For/Against

6

2.93

AGM audio track transcription

1

0.49

Mean

2.20

Source: Own from SPSS

FIGURE 4:

Industry means for AGMs

Source: Own from SPSS

Roadshows, or investor conferences, are held by companies to “sell” their company as an

investment proposition to institutional investors. This might be undertaken if the company is

looking for capital to fund expansion plans. The prevalence of these type of presentations on

the IR webpages is considerably more. Table 5 indicates that a third of companies posted their

Powerpoint presentation on their website and a further 16.59 per cent made the

handout/booklet available. A few companies did provide an audio or video recording, but only

five provided the transcription. The mean score for Roadshows is 13.37 per cent, which is still

low.

39

�TABLE 5:

Roadshows on websites

Criteria

Available

(N = 205) %

Roadshows as audio

17

8.29

Roadshows as video

13

6.34

Roadshow's PPT

68

33.17

Roadshows PDF of handout/booklet

34

16.59

Roadshow audio track transcription

5

2.44

Mean

13.37

Source: Own from SPSS

From Figure 5 we can see that Technology are once again performing poorly. The one-way

ANOVA, rejecting equal variances, indicates that there were indeed significant industry

differences (Welch F(5, 199) = 3.494, p = 0.007). The Games-Howell post-hoc tests reveal

that the significant differences in means arise between the Basic Resources and Technology

industries.

FIGURE 5:

Industry means for roadshows

Source: Own from SPSS

The last grouping of criteria relate to the usability of the formats of the presentations. ISO

9241-11 (ISO, 1998) defines usability as “the extent to which a system can be used by

specified users to achieve a specified goal with effectiveness, efficiency and satisfaction in a

specified context of use”. Using the information on the website should be easy for visitors. The

results are available in Table 6. About a quarter of the companies in the sample complied with

the criteria relating to indicating the length of the webcast recording, splitting the audio/video

file in smaller sections and using auto detect to determine the visitor’s media player. With this

information available on the website, visitors can decide upfront if they want to download large

files or not. A fifth of companies had their Powerpoint slides of the presentation run

synchronously with the audio/video of the speaker, which makes it easier to follow. Half of the

companies grouped all materials of the same event together so that visitors do not need to

“jump around” on the website to find it. About sixty per cent of the sample complied with the

criteria relating to the handouts/slides. Overall, usability was the area where companies scored

the best, with a sample mean of 40.73 per cent.

40

�TABLE 6:

Usability of presentation files

Criteria

Available

(N = 205) %

Webcast: Duration/length

51

24.88

Webcast: Divided in sub-sections

49

23.90

Webcast: Use auto detect for player

52

25.37

PPT slides synchronised to audio track

45

21.95

Groups materials of same event together

101

49.27

PPT or booklets' default font size readable

126

61.46

Total number of pages/slides and current progress

122

59.51

Avoids dark colours for background

122

59.51

Mean

40.73

Source: Own from SPSS

From Figure 6 we can see that Basic Materials once again performed the best with a score of

51.2 per cent. Financial companies had the second highest score with a mean of 42.5 per

cent. Technology companies again achieved the lowest compliance score of only 29.2 per

cent. The one-way ANOVA, assuming equal variances, indicates that there were no significant

industry differences (F(5, 199) = 1.563, p = 0.172).

FIGURE 6:

Industry means for usability

Source: Own from SPSS

41

�FIGURE 7:

Industry means for total presentation score

Source: Own from SPSS

Lastly, Figure 7 provides an industry analysis of the total presentation score. From the

previous discussions of the different types of investor presentations, it is not surprising to see

that the Basic Materials industry had the highest mean score of 25.7 per cent and that the

Technology industry had the lowest mean score of 13.8 per cent. Esterhuyse and Wingard

(2016: 227) also reported that six of the top ten online IR scores in their comprehensive study

were obtained by Basic Materials companies. Finally, the one-way ANOVA, assuming equal

variances, indicates that there were no significant industry differences (F(5, 199) = 1.771, p =

0.120) in the prevalence of investor and analyst presentations on IR webpages for the sample

of JSE-listed companies.

PRACTICAL MANAGERIAL IMPLICATIONS AND RECOMMENDATIONS

The low mean score of 19.90 per cent and the fact that 31 companies had no information

regarding presentations or meetings with investors is worrying. One of the key roles of the

CEO, CFO and Investor Relations Officer (IRO) is to communicate with the capital market.

Although the sample companies may comply with the letter of the JSE Listings Requirements

regarding disclosure of value-relevant information via SENS and press releases, it seems that

most are not concerned with being more transparent and accessible to retail investors by also

making available on the company’s IR webpages information communicated via other fora.

By perpetuating a state of information asymmetry, it seems that many boards of JSE-listed

companies are not complying with good corporate governance in terms of King III’s (IoD, 2009)

Principle 8.5, which states that “Transparent and effective communication with stakeholders

is essential for building and maintaining their trust and confidence”. It is interesting to note that

Steinhoff International was included in this study and performed very poorly.

It is recommended that the IROs familiarise themselves with best practices (IRS, 2012;

Loranger & Nielsen, 2009) for hosting Results Announcements, Conference Calls, AGMs and

Roadshows, including usability aspects surrounding archiving these communications on the

website. Although PDF copies of Powerpoint presentations or handouts are provided by more

companies, very few companies provided audio or video recordings. That means that

institutional investors and analysts that attend these presentations, or dial in to the conference

calls, are privileged to receive non-textual cues that prior research indicated influence

investment decisions, yet this is not available to retail investors. Bandwidth has increased

during the last few years, enabling even retail investors to download and listen to/view media

files with ease on their laptops and smartphones. Furthermore, by archiving recordings and

other material related to these investor and analyst presentations, they are also available for

42

�future use by institutional investors and analysts that did not attend the presentations, or

decided at a later stage to research the company as a potential investment.

CONCLUSIONS, LIMITATIONS AND DIRECTIONS FOR FUTURE RESEARCH

Information asymmetry arises when one party has qualitatively better information than another

party, and in some cases receives it earlier than another party. Information asymmetry can

arise between management of the company and all current and potential investors.

Information asymmetry also occurs between investors themselves, based on their access to

information provided by management and own research efforts. In order to reduce information

asymmetry, companies communicate additional information voluntarily. The first objective of

this study was to determine the prevalence of investor and analyst presentations on IR

webpages as one means of communicating information to capital market participants.

Although PDF slides and handouts were provided in many cases, very few JSE-listed

companies provided audio and/or video recordings of these presentations and conference

calls. The second objective was to determine whether industry classification played a role in

the prevalence of investor and analyst presentations on companies’ IR webpages. Results

indicate that although the Basic Resources industry performed the best in most areas, and the

Technology industry the worst, there was no statistically significant difference in the

association of presentation score and industry.

This study contributes to the literature about alternative disclosure channels used by

companies to reduce information asymmetry in the capital market and compliance with

corporate governance guidelines for communication practices to be equitable. Although Hedlin

(1999) propagated for companies to employ the unique features of the internet to enhance

their communication with investors beyond that which can be achieved with written text, only

a few companies listed on the JSE made use of this channel. Institutional investors and

analysts may still gather additional signals from these investor presentations based on

behavioural cues in the verbal communication from management and questions asked by

analysts. Preventing retail investors from accessing the same verbal and non-verbal cues as

institutional investors and analysts, even if by omission rather than deliberate intent, is also a

contravention of the spirit of good corporate governance practices.

Future areas for research can be gleaned from the limitations of this study. The websites of

the JSE-listed companies were surveyed in 2012. Companies could have improved their IR

practices in the meantime and a follow-up study is recommended. The current study

investigated industry differences in trying to explain the prevalence or absence of investor

presentations on the IR webpages. Future studies could endeavour a more comprehensive

analysis by incorporating other elements that are associated with disclosure quality in general,

such as size (market capitalisation), ownership concentration, foreign ownership, listing on

more than one exchange, and auditor quality.

SELECTED REFERENCES

Akerlof, G. 1970. The market for “lemons”: Quality uncertainty and the market mechanism.

The Quarterly Journal of Economics, 84 (3): 488–500. DOI: 10.1007/978-1-349-24002-9_9.

Basoglu, K. and Hess, T. 2014. Online Business Reporting: A Signalling Theory Perspective.

Journal of Information Systems, 28 (2): 67–101. DOI: 10.2308/isys-50780.

Bloomfield, R. 2008. Accounting as the Language of Business. Accounting Horizons, 22 (4):

433–436. DOI: 10.2308/acch.2008.22.4.433.

43

�Borochin, P., Cicon, J., DeLisle, J. and Price, M. 2018. The effects of conference call tones

on market perceptions of value uncertainty. Journal of Financial Markets, In press. DOI:

10.1016/j.finmar.2017.12.003.

Brown, L.D., Call, A.C., Clement, M.B. and Sharp, N.Y. 2015. Inside the “Black Box” of Sell

Side Financial Analysts. Journal of Accounting Research, 53 (1): 1–47. DOI: 10.1111/1475679X.12067.

Bushee, B.J., Matsumoto, D.A. and Miller, G.S. 2004. Managerial and investor responses to

disclosure regulation: The case of Reg FD and conference calls. The Accounting Review, 79

(3): 617–643.

DiPiazza Jnr., S.A. and Eccles, R.G. 2002. Building Public Trust – The future of corporate

reporting. New York: Johan Wiley and Sons.

Esterhuyse, L. and Wingard, C. 2016. An exploration of the online investor relations (IR)

practices of companies listed on the Johannesburg Stock Exchange (JSE). South African

Journal of Economic and Management Sciences, 19 (2): 215–231.

Grant, S., Hodge, F. and Sinha, R. 2018. How disclosure medium affects investor reactions to

CEO bragging, modesty, and humblebragging. Accounting, Organizations and Society, In

press. DOI: 10.1016/j.aos.2018.03.006.

Hedlin, P. 1999. The Internet as a vehicle for investor relations: the Swedish case. European

Accounting Review, 8 (2): 373–381. DOI: 10.1080/096381899336104.

Holland, D., Krause, A., Provencher, J. and Seltzer, T. 2018. Transparency tested: The

influence of message features on public perceptions of organizational transparency. Public

Relations Review, 44 (2): 256–264. DOI: 10.1016/j.pubrev.2017.12.002.

Institute of Directors (IoD). 2009. King Code of Governance Principles for South Africa 2009.

Johannesburg: IoD. [Online] Available from http://www.iodsa.co.za/resource/

collection/94445006-4F18-4335-B7FB-7F5A8B23FB3F/King_III_Code_for_

Governance_Principles.pdf [Accessed 15 June 2018].

International Organization for Standardization (ISO). 1998. 9241-11 Ergonomic Requirements

for Office Work with visual Display Terminals (VDTs). Part 11: Guidance on Usability. Geneva:

ISO.

Investor Relations Society of the UK (IRS). 2012. Best practice guidelines corporate websites

updated March 2012. London: IRS of the UK. [Online]

Available from

http://www.irs.org.uk/files/Best_Practice_Guidelines_Corporate_ websites_2012_FINAL.pdf

[Accessed on 27 May 2012].

IoD – see Institute of Directors.

IRS – see Investor Relations Society of the UK

ISO – see International Organization for Standardizarion

Johannesburg Stock Exchange (JSE). 2011. JSE Limited listings requirements. 2nd ed.

(Service Issue 14). Durban: LexisNexis. [Online] Available from https://www.jse.co.za/content/

JSEAnnouncementItems/Service%20Issue%2014(2).pdf [Accessed on 28 October 2011].

44

�Johannesburg Stock Exchange (JSE). 2015. Guidance letter: discussions with journalists and

investment

analysts.

Johannesburg:

JSE.

[Online]

Available

from:

https://www.jse.co.za/content/JSEGuidanceLettersItems/Guidance%20Letter%20Analysts%

20October%202015.pdf [Accessed on 7 April 2016].

JSE – see Johannesburg Stock Exchange

Ke, B., Petroni, K. and Yu, Y. 2008. The Effect of Regulation FD on Transient Institutional

Investors’ Trading Behavior. Journal of Accounting Research, 46 (4): 853–883. DOI:

10.1111/j.1475-679X.2008.00296.x.

Kirk, M. and Vincent, J. 2014. Professional Investor Relations within the Firm. The Accounting

Review, 89 (4): 1421–1452. DOI: 10.2308/accr-50724.

Laughlin, R. 1995. Empirical research in accounting: alternative approaches and a case for

“middle-range” thinking. Accounting, Auditing and Accountability Journal, 8 (1): 63–87. DOI:

10.1108/09513579510146707.

Lee, E., Strong, N. and Zhu, Z. 2014. Did Regulation Fair Disclosure, SOX, and Other Analyst

Regulations Reduce Security Mispricing? Journal of Accounting Research, 52 (3): 733–774.

DOI: 10.1111/1475-679X.12051.

Lee, J. 2016. Can Investors Detect Managers’ Lack of Spontaneity? Adherence to Predetermined Scripts during Earnings Conference Calls. The Accounting Review, 91 (1) :229–

250. DOI: 10.2308/accr-51135.

Loranger, H. and Nielsen, J. 2009. Designing websites to maximise investor relations.

Usability guidelines for Investor Relations (IR) on corporate websites. Freemont, CA: Nielsen

Norman Group.

OECD – see Organisation for Economic Co-operation and Development

Organisation for Economic Co-operation and Development (OECD). 2015. G20/OECD

Principles of corporate governance. Paris: OECD Publishing. [Online] Available from

https://www.oecd-ilibrary.org/docserver/9789264236882en.pdf?expires=1525687233andid=idandaccname=ocid72025909andchecksum=8C24411E

119581C68E58515AC8E7FAB0 [Accessed on 23 April 2018].

Ramalingegowda, S. 2014. Evidence from impending bankrupt firms that long horizon

institutional investors are informed about future firm value. Review of Accounting Studies, 19

(2): 1009–1045. DOI: 10.1007/s11142-013-9271-6.

Republic of South Africa (RSA). 2012. Financial Markets Act, No. 19 of 2012. Pretoria:

Government Printer.

RSA – see Republic of South Africa

SEC – see Securities and Exchange Commission

Securities and Exchange Commission (SEC). 2000. Selective disclosure and insider trading.

Release 33-7881. Washington, DC: Securities and Exchange Commission.

Solomon, D. and Soltes, E. 2015. What are we meeting for? The consequences of private

meetings with investors. The Journal of Law and Economics, 58 (2): 325–355. DOI:

10.1086/684038.

45

�Soltes, E. 2014. Private Interaction Between Firm Management and Sell‐Side Analysts.

Journal of Accounting Research, 52 (1): 245–272. DOI: 10.1111/1475-679X.12037.

Spence, M. 1973. Job market signalling. The Quarterly Journal of Economics, 87 (3): 356–

374. DOI: 10.2307/1882010.

46

�

Leana Esterhuyse

Leana Esterhuyse