Market Macro Myths Debts Deficits and Delusions

Market Macro Myths Debts Deficits and Delusions

Download as pdf or txt

You might also like

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- OakTree Real EstateDocument13 pagesOakTree Real EstateCanadianValue100% (1)

- Einhorn Consol PresentationDocument107 pagesEinhorn Consol PresentationCanadianValueNo ratings yet

- ch09 Accounting Systems Solution ManualDocument10 pagesch09 Accounting Systems Solution ManualLindsey Clair RoyalNo ratings yet

- James Montier WhatGoesUpDocument8 pagesJames Montier WhatGoesUpdtpalfiniNo ratings yet

- GMO Quarterly Letter-My Sister's Pension Assets 0412 GMO-GranthamDocument11 pagesGMO Quarterly Letter-My Sister's Pension Assets 0412 GMO-GranthamMarko AleksicNo ratings yet

- Jgletter All 3q09Document14 pagesJgletter All 3q09ZerohedgeNo ratings yet

- Stocks Have Rallied and Will Now Return Less. Hip Hip Hooray! But Now What?Document5 pagesStocks Have Rallied and Will Now Return Less. Hip Hip Hooray! But Now What?saif_shakeelNo ratings yet

- The End of An Era: Uarterly EtterDocument10 pagesThe End of An Era: Uarterly EtterthickskinNo ratings yet

- 7YrForecasts 111Document1 page7YrForecasts 111maxiannozziNo ratings yet

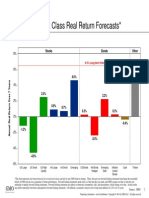

- 7-Year Asset Class Real Return Forecasts : As of May 31, 2019Document1 page7-Year Asset Class Real Return Forecasts : As of May 31, 2019Tim TruaxNo ratings yet

- Grantham 4-25-11 Letter Part 1Document19 pagesGrantham 4-25-11 Letter Part 1wompyfratNo ratings yet

- Grantham Quarterly Dec 2011Document4 pagesGrantham Quarterly Dec 2011careyescapitalNo ratings yet

- 7YrForecasts 813Document1 page7YrForecasts 813CanadianValueNo ratings yet

- GMO Capital Q3 2013 Letter To InvestorsDocument15 pagesGMO Capital Q3 2013 Letter To InvestorsWall Street WanderlustNo ratings yet

- GMO 7 Year Asset Class Forecast Apr 14Document1 pageGMO 7 Year Asset Class Forecast Apr 14CanadianValueNo ratings yet

- GMO 7-Year Forecast - Feb '12Document1 pageGMO 7-Year Forecast - Feb '12Douglas RattrayNo ratings yet

- GMO Grantham Quarterly Apr10Document14 pagesGMO Grantham Quarterly Apr10careyescapitalNo ratings yet

- Q2 2007 GmoDocument8 pagesQ2 2007 GmoGonçalo Callé Lucas MendesNo ratings yet

- Gmo Quarterly LetterDocument16 pagesGmo Quarterly LetterAnonymous Ht0MIJ100% (2)

- Hussman Funds 2009-07-27Document2 pagesHussman Funds 2009-07-27rodmorley100% (2)

- HMMM Mar 18 2012aDocument24 pagesHMMM Mar 18 2012aginunnNo ratings yet

- Hussman Funds - Stocks Extreme Conditions and Typical Outcomes - May 2, 2011Document6 pagesHussman Funds - Stocks Extreme Conditions and Typical Outcomes - May 2, 2011KoalaCapitalSICAVNo ratings yet

- Family Dollar-Ackman Pres-Ira Sohn Conf-5!25!11Document42 pagesFamily Dollar-Ackman Pres-Ira Sohn Conf-5!25!11kessbrokerNo ratings yet

- GMO Grantham July 09Document6 pagesGMO Grantham July 09rodmorleyNo ratings yet

- GMO 2009 1st Quarter Investor LetterDocument14 pagesGMO 2009 1st Quarter Investor LetterBrian McMorris100% (2)

- HMMM 20 November 2012Document37 pagesHMMM 20 November 2012richardck61No ratings yet

- HMMM Jul 08 2012Document27 pagesHMMM Jul 08 2012teidukasNo ratings yet

- Hay ManDocument24 pagesHay ManZerohedge100% (1)

- 2012 09 09ahmmmDocument27 pages2012 09 09ahmmmrichardck61No ratings yet

- Wally Weitz Letter To ShareholdersDocument2 pagesWally Weitz Letter To ShareholdersAnonymous j5tXg7onNo ratings yet

- HMMM May 15 2011Document24 pagesHMMM May 15 2011patra_kpNo ratings yet

- Second Quarter 2010 GTAA EquitiesDocument68 pagesSecond Quarter 2010 GTAA EquitiesZerohedge100% (1)

- Second Quarter 2010 GTAA Fixed IncomeDocument32 pagesSecond Quarter 2010 GTAA Fixed IncomeZerohedge100% (1)

- Guru Focus Interview With Arnold VandenbergDocument16 pagesGuru Focus Interview With Arnold VandenbergVu Latticework Poet100% (2)

- Asset Allocation With A Case Study PDFDocument24 pagesAsset Allocation With A Case Study PDFAdriano FragosoNo ratings yet

- By Ben Carlson: The Only Rational Deployment of Our IgnoranceDocument33 pagesBy Ben Carlson: The Only Rational Deployment of Our IgnoranceBen CarlsonNo ratings yet

- Third Quarter 2010 GTAA EquitiesDocument70 pagesThird Quarter 2010 GTAA EquitiesZerohedge100% (1)

- The Hardest Market EverDocument65 pagesThe Hardest Market EverBen Carlson100% (1)

- What Became of the Crow?: The inside story of the greatest gold discovery in historyFrom EverandWhat Became of the Crow?: The inside story of the greatest gold discovery in historyNo ratings yet

- Market Macro Myths Debts Deficits and DelusionsDocument13 pagesMarket Macro Myths Debts Deficits and DelusionsScott DauenhauerNo ratings yet

- An Antidote To Deficit PhobiaDocument4 pagesAn Antidote To Deficit PhobiaSergio OlarteNo ratings yet

- The Absolute Return Letter 0911Document9 pagesThe Absolute Return Letter 0911bhrijeshNo ratings yet

- "Investment Environment and Your Savings": Paul Krugman (Nobel Laureate)Document7 pages"Investment Environment and Your Savings": Paul Krugman (Nobel Laureate)api-236467720No ratings yet

- The Number 1 Reason YOU Became A SlaveDocument7 pagesThe Number 1 Reason YOU Became A SlavevomitNo ratings yet

- Economic PortfolioDocument24 pagesEconomic Portfoliowilliam garciaNo ratings yet

- David Graeber After The JubileeDocument5 pagesDavid Graeber After The JubileeBharat GujarNo ratings yet

- Randall Wray: Alternative Paths To Modern Money TheoryDocument18 pagesRandall Wray: Alternative Paths To Modern Money TheoryAnonymous rXnC47No ratings yet

- Grip of DeathDocument11 pagesGrip of Deathjawadahmad4uNo ratings yet

- BankNotes Feb 2012Document12 pagesBankNotes Feb 2012Michael HeidbrinkNo ratings yet

- The Deficit MythDocument15 pagesThe Deficit MythKuchayRiyazNo ratings yet

- Balance Sheets, The Transfer Problem, and Financial CrisesDocument8 pagesBalance Sheets, The Transfer Problem, and Financial Crisesvib89jNo ratings yet

- A DECADE OF SQUANDERED OPPORTUNITY by JM MinorDocument55 pagesA DECADE OF SQUANDERED OPPORTUNITY by JM MinorDesmond Sullivan100% (1)

- Macro PoloDocument14 pagesMacro PoloZerohedgeNo ratings yet

- David Ndii Open Letter To President Uhuru KenyattaDocument5 pagesDavid Ndii Open Letter To President Uhuru KenyattaBarrack OkothNo ratings yet

- GMO - James Montier - Is Austerity The Road To RuinDocument5 pagesGMO - James Montier - Is Austerity The Road To RuinthebigpicturecoilNo ratings yet

- Let's Talk About Our Future. Now!Document28 pagesLet's Talk About Our Future. Now!saitamNo ratings yet

- Paper-Richard KooDocument92 pagesPaper-Richard Koomatri.kushNo ratings yet

- Sonia Gandhi: InflationDocument6 pagesSonia Gandhi: InflationAditya SanyalNo ratings yet

- EeuuDocument3 pagesEeuuSol RuizNo ratings yet

- Understanding EconomicsDocument121 pagesUnderstanding EconomicsDharmesh Kher100% (2)

- KaseFundannualletter 2015Document20 pagesKaseFundannualletter 2015CanadianValueNo ratings yet

- Stan Druckenmiller Sohn TranscriptDocument8 pagesStan Druckenmiller Sohn Transcriptmarketfolly.com100% (1)

- Stan Druckenmiller The Endgame SohnDocument10 pagesStan Druckenmiller The Endgame SohnCanadianValueNo ratings yet

- Charlie Munger 2016 Daily Journal Annual Meeting Transcript 2 10 16 PDFDocument18 pagesCharlie Munger 2016 Daily Journal Annual Meeting Transcript 2 10 16 PDFaakashshah85No ratings yet

- The Stock Market As Monetary Policy Junkie Quantifying The Fed's Impact On The S P 500Document6 pagesThe Stock Market As Monetary Policy Junkie Quantifying The Fed's Impact On The S P 500dpbasicNo ratings yet

- Greenlight UnlockedDocument7 pagesGreenlight UnlockedZerohedgeNo ratings yet

- Munger-Daily Journal Annual Mtg-Adam Blum Notes-2!10!16Document12 pagesMunger-Daily Journal Annual Mtg-Adam Blum Notes-2!10!16CanadianValueNo ratings yet

- Hussman Funds Semi-Annual ReportDocument84 pagesHussman Funds Semi-Annual ReportCanadianValueNo ratings yet

- 'Long Term or Confidential (KIG Special) 2015Document12 pages'Long Term or Confidential (KIG Special) 2015CanadianValueNo ratings yet

- Weitz - 4Q2015 Analyst CornerDocument2 pagesWeitz - 4Q2015 Analyst CornerCanadianValueNo ratings yet

- Whitney Tilson Favorite Long and Short IdeasDocument103 pagesWhitney Tilson Favorite Long and Short IdeasCanadianValueNo ratings yet

- Einhorn Q4 2015Document7 pagesEinhorn Q4 2015CanadianValueNo ratings yet

- Investor Call Re Valeant PharmaceuticalsDocument39 pagesInvestor Call Re Valeant PharmaceuticalsCanadianValueNo ratings yet

- Starboard Value LP AAP Presentation 09.30.15Document23 pagesStarboard Value LP AAP Presentation 09.30.15marketfolly.com100% (1)

- Letter To Clients and ShareholdersDocument3 pagesLetter To Clients and ShareholdersJulia Reynolds La RocheNo ratings yet

- Absolute Return Oct 2015Document9 pagesAbsolute Return Oct 2015CanadianValue0% (1)

- Sec V Prosperity - Com, Inc (Pci)Document1 pageSec V Prosperity - Com, Inc (Pci)Park Chael Reose EonniNo ratings yet

- Financing Energy Efficiency in Residential Buildings Experiences From Germany - Model For India?Document12 pagesFinancing Energy Efficiency in Residential Buildings Experiences From Germany - Model For India?Urban Community of PracticeNo ratings yet

- Sales TerritoryDocument24 pagesSales Territorysimpybansal1990100% (1)

- Traco Cable WCM ProjectDocument77 pagesTraco Cable WCM ProjectAjeesh K RajuNo ratings yet

- Jaro EducationDocument17 pagesJaro EducationfathimaNo ratings yet

- Equity Research Interview QuestionsDocument5 pagesEquity Research Interview Questions87rakesh0% (1)

- EP List - OKT DEC 2018 - Eng PDFDocument32 pagesEP List - OKT DEC 2018 - Eng PDFdusankg1No ratings yet

- Credit Risk: Credit Relationship Manager Chief Risk Officer Disagree Over The Proposal Have To Wait LongerDocument3 pagesCredit Risk: Credit Relationship Manager Chief Risk Officer Disagree Over The Proposal Have To Wait LongerAfriyantiHasanahNo ratings yet

- Sesa Goa: Performance HighlightsDocument12 pagesSesa Goa: Performance HighlightsAngel BrokingNo ratings yet

- Porter's Five Model AnalysisDocument5 pagesPorter's Five Model AnalysisSamia ShahidNo ratings yet

- The Nature of Accounting: Things A CompanyDocument10 pagesThe Nature of Accounting: Things A CompanyKeempee Ian GaviranNo ratings yet

- Ratio Analysis:: Internship ReportDocument5 pagesRatio Analysis:: Internship ReportsahhhhhhhNo ratings yet

- Telecom Industry in IndiaDocument21 pagesTelecom Industry in IndiaVaibhav PatelNo ratings yet

- 40 SitaraDocument2 pages40 SitaraTIN_CUP_87100% (1)

- FinanceAssignment2 V 2Document8 pagesFinanceAssignment2 V 2Victor MirandaNo ratings yet

- Presentation On Export ProceduresDocument24 pagesPresentation On Export ProceduresSumit SainiNo ratings yet

- The European Investment Bank Proposes Two New EIBURS Sponsorships Within Its EIB-Universities Research ActionDocument3 pagesThe European Investment Bank Proposes Two New EIBURS Sponsorships Within Its EIB-Universities Research ActionOana MunteanuNo ratings yet

- Doing Business in RPDocument80 pagesDoing Business in RPRichard BalaisNo ratings yet

- 2019 Level II IFT Study PlannerDocument22 pages2019 Level II IFT Study PlannermanishNo ratings yet

- Valuation of SecuritiesDocument43 pagesValuation of SecuritiesVaidyanathan Ravichandran100% (1)

- Rahul Mutual FundDocument8 pagesRahul Mutual FundGauravChhokarNo ratings yet

- Allianz - Wikipedia, The Free EncyclopediaDocument7 pagesAllianz - Wikipedia, The Free Encyclopediahgosai30No ratings yet

- Final TOS BUSINESS FINANCEDocument2 pagesFinal TOS BUSINESS FINANCEIan Varela100% (3)

- Strategic Management of Coca ColaDocument84 pagesStrategic Management of Coca ColaAnjum hayatNo ratings yet

- Wienerberger - Annual Report 2013Document190 pagesWienerberger - Annual Report 2013kaiuskNo ratings yet

- Simulation SlidesDocument46 pagesSimulation SlidesMalick Toguyeni100% (2)

- Abstract The Research Article Is Titled As Comparative Study On Performance of SelectedDocument3 pagesAbstract The Research Article Is Titled As Comparative Study On Performance of SelectedKumar ankitNo ratings yet

- Sme Symposium Programme Booklet 2017 Caa31032017 David Wanted Photo ChangeDocument23 pagesSme Symposium Programme Booklet 2017 Caa31032017 David Wanted Photo Changeapi-309215991No ratings yet

- Brand ExtensionsDocument21 pagesBrand ExtensionsLance BarnesNo ratings yet