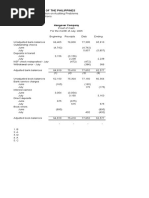

Financial Statements

Financial Statements

Download as doc, pdf, or txt

You might also like

- Pas 1 Presentation of Financial StatementsDocument8 pagesPas 1 Presentation of Financial StatementsR.A.100% (1)

- #3 Pas 1Document6 pages#3 Pas 1Shara Joy B. ParaynoNo ratings yet

- THEORIES PAS 1 and PAS 8Document28 pagesTHEORIES PAS 1 and PAS 8PatrickMendozaNo ratings yet

- 2022-2023 INTACC3 PAS 1 HandoutsDocument9 pages2022-2023 INTACC3 PAS 1 HandoutsJefferson AlingasaNo ratings yet

- IA3 1st HandoutDocument3 pagesIA3 1st HandoutUyara LeisbergNo ratings yet

- 02 Lec Financial StatementsDocument5 pages02 Lec Financial StatementsYoung MetroNo ratings yet

- What It Does:: With PfrssDocument7 pagesWhat It Does:: With PfrssOlive Jean TiuNo ratings yet

- cfasDocument23 pagescfasJade BarretNo ratings yet

- Chapter 14 Financial StatementsDocument12 pagesChapter 14 Financial Statementsmaria isabella100% (3)

- 12 PAS 1 Presentation of Financial Statements Part 1Document4 pages12 PAS 1 Presentation of Financial Statements Part 1Keanlyn UnwinNo ratings yet

- Pas 1Document5 pagesPas 1Christy CaneteNo ratings yet

- Module 3 - Updates in Financial Reporting StandardsDocument6 pagesModule 3 - Updates in Financial Reporting Standardsjoubert andres100% (1)

- FAR BULLET NOTES 6 - Presentation of Financial StatementsDocument5 pagesFAR BULLET NOTES 6 - Presentation of Financial StatementsDemon AlphaNo ratings yet

- NFRS IiiDocument105 pagesNFRS Iiikaran shahiNo ratings yet

- COMPANIES FINAL ACCOUNT FormatDocument11 pagesCOMPANIES FINAL ACCOUNT Formatselinawireko12No ratings yet

- IAS 1 - Financial StatementsDocument7 pagesIAS 1 - Financial StatementsJOEL VARGHESE CHACKO 2011216No ratings yet

- Pas 1 - Presentation of Financial StatementsDocument27 pagesPas 1 - Presentation of Financial StatementsJomel Serra Briones100% (1)

- Pas 1 Presentation of Financial Statements - 150413098Document28 pagesPas 1 Presentation of Financial Statements - 150413098wasitrizzaNo ratings yet

- Section 3 and 4Document6 pagesSection 3 and 4Alaine DobleNo ratings yet

- Chapter 3 - IAS 1Document10 pagesChapter 3 - IAS 1Bahader AliNo ratings yet

- Cfas Presentation of FSDocument27 pagesCfas Presentation of FSRogelio F Geronimo Jr.No ratings yet

- A Complete Set of Financial Statements ComprisesDocument9 pagesA Complete Set of Financial Statements Comprisesۦۦۦۦۦ ۦۦ ۦۦۦNo ratings yet

- Pas 1Document52 pagesPas 1Justine VeralloNo ratings yet

- Toa Pas 1 Financial StatementsDocument14 pagesToa Pas 1 Financial StatementsreinaNo ratings yet

- Presentation of Financial Statements (Copy) (Copy) - TaskadeDocument5 pagesPresentation of Financial Statements (Copy) (Copy) - Taskadebebanco.maryzarianna.olaveNo ratings yet

- Intacc (Non Current Assets Held For Sale-Changes On Equity) Reviewer.Document22 pagesIntacc (Non Current Assets Held For Sale-Changes On Equity) Reviewer.Roselynne GatbontonNo ratings yet

- UntitledDocument150 pagesUntitledRica Ella RestauroNo ratings yet

- PAS 1 Presentation of Financial Statements 2020Document30 pagesPAS 1 Presentation of Financial Statements 2020Jilian Kate Alpapara BustamanteNo ratings yet

- Acc 102 - Module 3aDocument12 pagesAcc 102 - Module 3aPatricia CarreonNo ratings yet

- INTACC 3.1LN Presentation of Financial StatementsDocument9 pagesINTACC 3.1LN Presentation of Financial StatementsAlvin BaternaNo ratings yet

- IPSAS 1 Financial Statement Present Including Cash)Document34 pagesIPSAS 1 Financial Statement Present Including Cash)zelalemNo ratings yet

- APC 403 PFRS For SEs (Section 3)Document7 pagesAPC 403 PFRS For SEs (Section 3)AnnSareineMamadesNo ratings yet

- 08 Handout 1 (CFAS)Document12 pages08 Handout 1 (CFAS)laurencedechosa907No ratings yet

- IPSAS 1 For 2022 SeptDocument5 pagesIPSAS 1 For 2022 SeptWilson Mugenyi KasendwaNo ratings yet

- Pas 1 - Presentation of Financial StatementsDocument30 pagesPas 1 - Presentation of Financial StatementsRoxanne GiananNo ratings yet

- Financial StatementsDocument13 pagesFinancial Statementsmhel cabigonNo ratings yet

- Ias 1 Presentation of Financial Statements-2Document7 pagesIas 1 Presentation of Financial Statements-2Pia ChanNo ratings yet

- Cash Basis IPSASDocument18 pagesCash Basis IPSASBlade HasanNo ratings yet

- Objective of IAS 1Document8 pagesObjective of IAS 1mahekshahNo ratings yet

- Auditing Problem - Correl 2 Exercise 1: Name: Date: Professor: Section: ScoreDocument17 pagesAuditing Problem - Correl 2 Exercise 1: Name: Date: Professor: Section: ScorePrincesNo ratings yet

- IAS 1_ Presentation of Financial StatementsDocument6 pagesIAS 1_ Presentation of Financial StatementsUtban AshabNo ratings yet

- Financial Statement Presentation. Theory of Accounts GuideDocument20 pagesFinancial Statement Presentation. Theory of Accounts GuideCykee Hanna Quizo LumongsodNo ratings yet

- TOAMOD2 Financial Statement PresentationDocument20 pagesTOAMOD2 Financial Statement PresentationCukeeNo ratings yet

- Government Accounting: Accounting For Non-Profit OrganizationsDocument39 pagesGovernment Accounting: Accounting For Non-Profit OrganizationsmoNo ratings yet

- Objective of PAS 1Document7 pagesObjective of PAS 1kristelle0marisseNo ratings yet

- CFAS - Philippine Accounting StandardsDocument39 pagesCFAS - Philippine Accounting StandardsZerille Lynnelle Villamor Simbajon100% (1)

- Cfas Notes Salisid: Chapter 03: Presentation of Financial StatementsDocument11 pagesCfas Notes Salisid: Chapter 03: Presentation of Financial StatementsBerdel PascoNo ratings yet

- Chapter 14 Financial StatementsDocument12 pagesChapter 14 Financial StatementsAngelica Joy Manaois100% (1)

- Chapter 14 Financial StatementsDocument82 pagesChapter 14 Financial StatementsKate CuencaNo ratings yet

- Statement of Financial PositionDocument48 pagesStatement of Financial Positionnot funny didn't laughNo ratings yet

- CFAS-Unit-1-Module-2Document25 pagesCFAS-Unit-1-Module-2alessandroandypascoyNo ratings yet

- Presentation of FSDocument9 pagesPresentation of FSrose anneNo ratings yet

- LkasDocument24 pagesLkasRommel CruzNo ratings yet

- Sme Discussion TemplateDocument5 pagesSme Discussion TemplateLeahmae OlimbaNo ratings yet

- Acc 304 - Module 1 - Published Finanancial Reports and AccountsDocument4 pagesAcc 304 - Module 1 - Published Finanancial Reports and Accountsjimoh kamiludeenNo ratings yet

- Ias 1 - IcanDocument51 pagesIas 1 - IcanLegogie Moses AnoghenaNo ratings yet

- Ias 34Document4 pagesIas 34OLANIYI DANIELNo ratings yet

- Pas 1Document12 pagesPas 120220025082No ratings yet

- PRTC 1st Preboard Solution GuideDocument48 pagesPRTC 1st Preboard Solution GuideAnonymous Lih1laax100% (2)

- AP 59 FinPB - 5.06Document8 pagesAP 59 FinPB - 5.06Anonymous Lih1laaxNo ratings yet

- PRTC - Final PREBOARD Solution Guide (2 of 2)Document37 pagesPRTC - Final PREBOARD Solution Guide (2 of 2)Anonymous Lih1laaxNo ratings yet

- Single Entry FormulasDocument3 pagesSingle Entry FormulasDexter DeeNo ratings yet

- Practical Accounting 1Document14 pagesPractical Accounting 1Anonymous Lih1laaxNo ratings yet

- IM Ch3-7e - WRLDocument49 pagesIM Ch3-7e - WRLAnonymous Lih1laax0% (1)