Uco Bank

Uco Bank

Download as ppt, pdf, or txt

You might also like

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- Customer Satisfaction On HDFC BankDocument106 pagesCustomer Satisfaction On HDFC BankgoswamiphotostatNo ratings yet

- Dhanalaxmi Bank Final Project Report by YkartheekgupthaDocument75 pagesDhanalaxmi Bank Final Project Report by YkartheekgupthaYkartheek GupthaNo ratings yet

- Cumulative Deposit SchemeDocument9 pagesCumulative Deposit Schemehisri6350No ratings yet

- Routing (ABA) : 061120084: Page 1 of 1Document1 pageRouting (ABA) : 061120084: Page 1 of 1Sayed Ariful AshrafNo ratings yet

- Project Report On PSB Bank For Intership TrainingDocument23 pagesProject Report On PSB Bank For Intership TrainingSrishti SinghNo ratings yet

- Dhanlaxmi Bank Project Report-AsifDocument56 pagesDhanlaxmi Bank Project Report-AsifUtkarsha Dhoundiyal100% (1)

- Fixed DepositDocument37 pagesFixed DepositMinal DalviNo ratings yet

- Retail Products and Services of State Bank of IndiaDocument81 pagesRetail Products and Services of State Bank of IndiaNishant Singh50% (2)

- "A Study of Home Loan Appraisal Process" "The Kolhapur Urban Co-Operative Bank LTD., Kolhapur"Document4 pages"A Study of Home Loan Appraisal Process" "The Kolhapur Urban Co-Operative Bank LTD., Kolhapur"Aditya JagtapNo ratings yet

- Book Report Bank of BarodaDocument13 pagesBook Report Bank of BarodaYash HemnaniNo ratings yet

- Comparitive Analysis of Mutual Fund of HDFC and Icici: Submitted To:-Department of Business AdministrationDocument22 pagesComparitive Analysis of Mutual Fund of HDFC and Icici: Submitted To:-Department of Business AdministrationRashi GuptaNo ratings yet

- Axis Mutual Fund Project ReportDocument37 pagesAxis Mutual Fund Project ReportVikas PabaleNo ratings yet

- Hinduja Leyland Finance LTDDocument42 pagesHinduja Leyland Finance LTDparamjeet99100% (6)

- Gold Loan ProjectDocument71 pagesGold Loan Projectsagirahamedb3No ratings yet

- Dhanlaxmi BankDocument95 pagesDhanlaxmi BankNidhi Mehta0% (2)

- Factors Influencing The Investment Decision of The Customers in Banking Sector, ChennaiDocument11 pagesFactors Influencing The Investment Decision of The Customers in Banking Sector, ChennaiChandru SivaNo ratings yet

- Service Quality Analysis of SBIDocument38 pagesService Quality Analysis of SBIAkhil BhatiaNo ratings yet

- Personal Load in SbiDocument42 pagesPersonal Load in SbiNitinAgnihotriNo ratings yet

- Customer Satisfaction and Brand Loyalty in Big BasketDocument73 pagesCustomer Satisfaction and Brand Loyalty in Big BasketUpadhayayAnkurNo ratings yet

- Customer Satisfaction Towards Retail Lending of UCO Bank in ChandigarhDocument72 pagesCustomer Satisfaction Towards Retail Lending of UCO Bank in Chandigarhshivkmrchauhan0% (1)

- Corporate Salary Account Report For HDFC BankDocument42 pagesCorporate Salary Account Report For HDFC BankShubhranshu SumanNo ratings yet

- Indian Bank ProjectDocument41 pagesIndian Bank ProjectAbhishek Pandey0% (1)

- Comparative Study of Mutual FundDocument65 pagesComparative Study of Mutual Fundsimantt100% (2)

- DocumentDocument46 pagesDocumentKaivalya JogNo ratings yet

- Final Project of Home LoanDocument63 pagesFinal Project of Home Loansheetalvaviya6439No ratings yet

- NSDL CDSLDocument20 pagesNSDL CDSLVinod Pandey50% (2)

- THEJASWINI ProjectDocument112 pagesTHEJASWINI Projectswamy yashuNo ratings yet

- Types of Loans: Executive SummaryDocument3 pagesTypes of Loans: Executive SummarynishthaNo ratings yet

- Godrej PDFDocument15 pagesGodrej PDFJyoti JangidNo ratings yet

- Manusha K N 1vw15mba16 - A2 - A2 PDFDocument90 pagesManusha K N 1vw15mba16 - A2 - A2 PDFmahanth gowdaNo ratings yet

- BibliographyDocument15 pagesBibliographyGoNo ratings yet

- Questionnaire: Services of Private Sector Banks and Public Sector Bank" I AmDocument4 pagesQuestionnaire: Services of Private Sector Banks and Public Sector Bank" I Amaxay12_kimcos10No ratings yet

- Nvestor Awareness & Preferences Towards Chit Funds With Reference To Neeladri Chits Hyderabad.Document12 pagesNvestor Awareness & Preferences Towards Chit Funds With Reference To Neeladri Chits Hyderabad.GayatriThotakuraNo ratings yet

- A Summer Project Report On Banking and SchemesDocument79 pagesA Summer Project Report On Banking and Schemessimran jeet67% (12)

- SBI State Bank of IndiaDocument25 pagesSBI State Bank of IndiaGurmeet Singh100% (2)

- EMI CalculatorDocument6 pagesEMI CalculatorPhanindra Sarma100% (1)

- A Study of Consumer Satisfaction Towards Sbi BankDocument58 pagesA Study of Consumer Satisfaction Towards Sbi BankNaresh KumarNo ratings yet

- Synopsis of Financial Analysis Canara BankDocument2 pagesSynopsis of Financial Analysis Canara BankManjunath ShettyNo ratings yet

- Bank of BarodaDocument75 pagesBank of BarodaVicky SinghNo ratings yet

- 10 - Chapter 3 KVB ShodhgangaDocument50 pages10 - Chapter 3 KVB ShodhgangaPankaj SinghNo ratings yet

- Strategy and Efforts of A Public Sector Bank For Financial InclusionDocument10 pagesStrategy and Efforts of A Public Sector Bank For Financial InclusionKhushi PuriNo ratings yet

- IntroductionDocument19 pagesIntroductionAmrapali JagtapNo ratings yet

- Funds Flow Statement of Reliance CommunicationDocument65 pagesFunds Flow Statement of Reliance CommunicationDr.P. Siva Ramakrishna100% (1)

- Loan & Credit Facility Provided by Different BanksDocument72 pagesLoan & Credit Facility Provided by Different Bankskaushal2442No ratings yet

- Minor Project ON 'Plastic Money of HDFC Bank''Document67 pagesMinor Project ON 'Plastic Money of HDFC Bank''ankushbabbarbcomNo ratings yet

- Final Project-Indian Banking and EconomyDocument64 pagesFinal Project-Indian Banking and EconomyShweta Yashwant ChalkeNo ratings yet

- CP ProjectDocument63 pagesCP ProjectJITENDRA VISHWAKARMANo ratings yet

- Mms Semester-Iv Project On Functional Specialisation Synopsis Name: Roll NoDocument2 pagesMms Semester-Iv Project On Functional Specialisation Synopsis Name: Roll Noharish nayakNo ratings yet

- Project Work BajajDocument49 pagesProject Work BajajSurendra Kumar MullangiNo ratings yet

- Analysis of Housing Finance Schemes of HDFC Bank ICICI Bank PNB SBI BankDocument85 pagesAnalysis of Housing Finance Schemes of HDFC Bank ICICI Bank PNB SBI BanksindhukotaruNo ratings yet

- UCO BankDocument128 pagesUCO BankRitesh TyagiNo ratings yet

- Sbi Project On DepositsDocument47 pagesSbi Project On DepositsSai Sekhar0% (1)

- Project Presentation On "Reverse Mortgage in India": Presenter: Shaikh Azharoddin Shakeel. Roll No.03 Mms-IiDocument17 pagesProject Presentation On "Reverse Mortgage in India": Presenter: Shaikh Azharoddin Shakeel. Roll No.03 Mms-IiAzharNo ratings yet

- Canara Bank KGFDocument106 pagesCanara Bank KGFJayanth RajNo ratings yet

- Project Guidelines For M. ComDocument35 pagesProject Guidelines For M. ComMuhammad Ayyaz Iftikhar0% (1)

- Awareness and Preference For Mutual FundsDocument3 pagesAwareness and Preference For Mutual Fundsamitnpatel10% (1)

- Cumulative Deposit SchemeDocument16 pagesCumulative Deposit SchemearctickingNo ratings yet

- BP Unit 4Document7 pagesBP Unit 4Nandhini VirgoNo ratings yet

- Corporation BankDocument31 pagesCorporation BankShruti Das50% (2)

- Detailed N It 66Document86 pagesDetailed N It 66sanjay kumarNo ratings yet

- Current AccountsDocument77 pagesCurrent AccountsVijay AnuNo ratings yet

- Notes For CBSEDocument11 pagesNotes For CBSEBinoy TrevadiaNo ratings yet

- Executive SummaryDocument15 pagesExecutive SummaryAmit DwivediNo ratings yet

- BFMDocument97 pagesBFMStuti MehrotraNo ratings yet

- Documents To Be Carried at The Time of The Visa InterviewDocument3 pagesDocuments To Be Carried at The Time of The Visa Interviewroopakv1990No ratings yet

- Brac Internship Report On Al Arafah Islami BankDocument44 pagesBrac Internship Report On Al Arafah Islami BankMd Tajwar Rashid TokyNo ratings yet

- SSC CGL Mains Mock - 3CDocument26 pagesSSC CGL Mains Mock - 3ChvvfnnbrsrNo ratings yet

- MEGA Facility Management TenderDocument23 pagesMEGA Facility Management TenderSaurabh JainNo ratings yet

- The Critically Analysis Customer Experience With Respective Personal Loan Disbursement Process.Document52 pagesThe Critically Analysis Customer Experience With Respective Personal Loan Disbursement Process.Isha GovindNo ratings yet

- Chaitanya Axis StatementDocument3 pagesChaitanya Axis StatementalthafNo ratings yet

- PDFDocument6 pagesPDFVigNeshNo ratings yet

- Final Project (Gayatri) PDFDocument52 pagesFinal Project (Gayatri) PDFGayatriThotakura0% (1)

- Government of India: Central Public Works DepartmentDocument52 pagesGovernment of India: Central Public Works DepartmentreddytlnNo ratings yet

- Sunil Panda Commerce Classes: Before Exam Practice Questions For Term 2 Boards Accounts-Not For Profit OrganisationDocument3 pagesSunil Panda Commerce Classes: Before Exam Practice Questions For Term 2 Boards Accounts-Not For Profit OrganisationHigi SNo ratings yet

- Bank AsiaDocument77 pagesBank AsiaAshiq Ali ChowdhuryNo ratings yet

- Sharekhan ProjectDocument53 pagesSharekhan Projectamitmaurya188% (8)

- Unit 1 Trade and Supporting Services BankingDocument9 pagesUnit 1 Trade and Supporting Services BankingSimra RiyazNo ratings yet

- A Project On Analysis of "HDFC BANK & ICICI BANK"Document38 pagesA Project On Analysis of "HDFC BANK & ICICI BANK"vikas_rathour01No ratings yet

- Closing of Bank AccountDocument15 pagesClosing of Bank AccountGurpreet Singh100% (3)

- 3 Form BDocument45 pages3 Form BDevNo ratings yet

- Opening of AccountsDocument6 pagesOpening of AccountswubeNo ratings yet

- Piyush Karmakar Iob Report - Compressed PDFDocument40 pagesPiyush Karmakar Iob Report - Compressed PDFKaran DwivediNo ratings yet

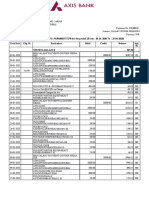

- Statement of Axis Account No:912010049541859 For The Period (From: 30-04-2022 To: 29-05-2022)Document5 pagesStatement of Axis Account No:912010049541859 For The Period (From: 30-04-2022 To: 29-05-2022)Rahul BansalNo ratings yet

- Master of Business Administration: A Dissertation ReportDocument67 pagesMaster of Business Administration: A Dissertation ReportRaja SekharNo ratings yet

- Instruments of Tax SavingDocument10 pagesInstruments of Tax Savinganilpipaliya117No ratings yet

- Advantages and Disadvantages of GlobalizationDocument19 pagesAdvantages and Disadvantages of GlobalizationSiddharth Senapati100% (1)

- What Is A Bank AccountDocument6 pagesWhat Is A Bank AccountJan Sheer ShahNo ratings yet

- Motor Vehicle Claims Thesis With JudgementsDocument28 pagesMotor Vehicle Claims Thesis With JudgementsAbhijit TripathiNo ratings yet