CFROI

CFROI

Download as pdf or txt

You might also like

- Proposals For Student Accomodation in DundeeDocument3 pagesProposals For Student Accomodation in DundeeAdelasoye TemiloluwaNo ratings yet

- Joe Hall - CROCI A Real Value Investment Process - April 2015Document29 pagesJoe Hall - CROCI A Real Value Investment Process - April 2015npapadokostasNo ratings yet

- Cfroi HoltDocument7 pagesCfroi Holtamro_baryNo ratings yet

- Valuing Using Industry MultiplesDocument11 pagesValuing Using Industry MultiplesSabina BuzoiNo ratings yet

- Wealth Creation Principles: The Measure of QualityDocument20 pagesWealth Creation Principles: The Measure of QualityFasila Shibin100% (1)

- Guggenheim ROIC PDFDocument16 pagesGuggenheim ROIC PDFJames PattersonNo ratings yet

- MFS Quality & ValueDocument4 pagesMFS Quality & ValueJeffrey WilliamsNo ratings yet

- 3-Statement Model PracticeDocument6 pages3-Statement Model PracticeWill SkaloskyNo ratings yet

- Eminence CapitalMen's WarehouseDocument0 pagesEminence CapitalMen's WarehouseCanadianValueNo ratings yet

- HOLT Wealth Creation Principles Don't Suffer From A Terminal Flaw, Add Fade To Your DCF Document-807204250Document13 pagesHOLT Wealth Creation Principles Don't Suffer From A Terminal Flaw, Add Fade To Your DCF Document-807204250tomfriisNo ratings yet

- Modern China EssayDocument5 pagesModern China Essayapi-358096422No ratings yet

- Merits of CFROIDocument7 pagesMerits of CFROIfreemind3682No ratings yet

- Measuring The Moat PDFDocument70 pagesMeasuring The Moat PDFFlorent CrivelloNo ratings yet

- EDHEC Valuation Manual PDFDocument40 pagesEDHEC Valuation Manual PDFradhika1992100% (1)

- When Entry Multiples Don't Matter - Andreessen Horowitz PDFDocument12 pagesWhen Entry Multiples Don't Matter - Andreessen Horowitz PDFbrineshrimpNo ratings yet

- Cashflow.comDocument40 pagesCashflow.comad9292No ratings yet

- One Job: Counterpoint Global InsightsDocument25 pagesOne Job: Counterpoint Global Insightscartigayan100% (1)

- GiantsDocument17 pagesGiantsCondro TriharyonoNo ratings yet

- Lecture 2Document24 pagesLecture 2Bình Minh100% (1)

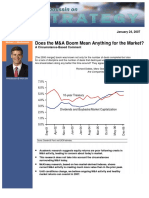

- Mauboussin - Does The M&a Boom Mean Anything For The MarketDocument6 pagesMauboussin - Does The M&a Boom Mean Anything For The MarketRob72081No ratings yet

- Reformulation - Analysis of SCFDocument17 pagesReformulation - Analysis of SCFAkib Mahbub KhanNo ratings yet

- Corporate Strategy and Shareholder Value: Howard E. JohnsonDocument24 pagesCorporate Strategy and Shareholder Value: Howard E. Johnsonprabhat127100% (1)

- Thefutureofequityresearch 2016Document118 pagesThefutureofequityresearch 2016Lanre Jonathan IgeNo ratings yet

- CS MarketNeutral HOLT Notes PDFDocument3 pagesCS MarketNeutral HOLT Notes PDFMichael Guan100% (1)

- Michael Mauboussin - Surge in The Urge To Merge, M&a Trends & Analysis 1-12-10Document15 pagesMichael Mauboussin - Surge in The Urge To Merge, M&a Trends & Analysis 1-12-10Phaedrus34No ratings yet

- MS - Good Losses, Bad LossesDocument13 pagesMS - Good Losses, Bad LossesResearch ReportsNo ratings yet

- Atoms, Bits, and Cash - The ABCs of Investing in The New EconomyDocument28 pagesAtoms, Bits, and Cash - The ABCs of Investing in The New Economypjs15No ratings yet

- In Defense of Shareholder ValueDocument11 pagesIn Defense of Shareholder ValueJaime Andres Laverde ZuletaNo ratings yet

- Capital Allocation Outside The U.SDocument83 pagesCapital Allocation Outside The U.SSwapnil GorantiwarNo ratings yet

- Still Powerful - The Internet's Hidden OrderDocument17 pagesStill Powerful - The Internet's Hidden Orderpjs15No ratings yet

- Yacktman PresentationDocument34 pagesYacktman PresentationVijay MalikNo ratings yet

- Bank ValuationsDocument20 pagesBank ValuationsHenry So E DiarkoNo ratings yet

- BBVA OpenMind Libro El Proximo Paso Vida Exponencial2Document59 pagesBBVA OpenMind Libro El Proximo Paso Vida Exponencial2giovanniNo ratings yet

- Michael Mauboussin - Seeking Portfolio Manager Skill 2-24-12Document13 pagesMichael Mauboussin - Seeking Portfolio Manager Skill 2-24-12Phaedrus34No ratings yet

- On Streaks: Perception, Probability, and SkillDocument5 pagesOn Streaks: Perception, Probability, and Skilljohnwang_174817No ratings yet

- Roe To CfroiDocument30 pagesRoe To CfroiSyifa034100% (2)

- Public To Private Equity in The United States: A Long-Term LookDocument82 pagesPublic To Private Equity in The United States: A Long-Term LookYog MehtaNo ratings yet

- Accretion Dilution ModelDocument10 pagesAccretion Dilution ModelQuýt BéNo ratings yet

- Q&A With Bluegrass CapitalDocument9 pagesQ&A With Bluegrass CapitalPook Kei JinNo ratings yet

- Bottom-Up EV Calculation (Finatics)Document5 pagesBottom-Up EV Calculation (Finatics)Jessica KaryonoNo ratings yet

- Competitive Advantage PeriodDocument6 pagesCompetitive Advantage PeriodAndrija BabićNo ratings yet

- Clear Thinking About Share RepurchaseDocument29 pagesClear Thinking About Share RepurchaseVrtpy CiurbanNo ratings yet

- Holt Cfroi ModelDocument8 pagesHolt Cfroi ModelJosephNo ratings yet

- ValueXVail 2013 - Chris KarlinDocument26 pagesValueXVail 2013 - Chris KarlinVitaliyKatsenelsonNo ratings yet

- Dangers of DCF MortierDocument12 pagesDangers of DCF MortierKitti WongtuntakornNo ratings yet

- Company ValuationDocument216 pagesCompany ValuationHuy Vu Chi100% (1)

- Valuation Final PPT 2015Document48 pagesValuation Final PPT 2015roopesh gowdaNo ratings yet

- Becton Dickinson BDX Thesis East Coast Asset MGMTDocument12 pagesBecton Dickinson BDX Thesis East Coast Asset MGMTWinstonNo ratings yet

- Where's The Bar - Introducing Market-Expected Return On InvestmentDocument17 pagesWhere's The Bar - Introducing Market-Expected Return On Investmentpjs15No ratings yet

- Death, Taxes and Reversion To The Mean - ROIC StudyDocument20 pagesDeath, Taxes and Reversion To The Mean - ROIC Studypjs15100% (1)

- Competitive Advantage in Investing: Building Winning Professional PortfoliosFrom EverandCompetitive Advantage in Investing: Building Winning Professional PortfoliosNo ratings yet

- Capital Structure and Profitability: S&P 500 Enterprises in the Light of the 2008 Financial CrisisFrom EverandCapital Structure and Profitability: S&P 500 Enterprises in the Light of the 2008 Financial CrisisNo ratings yet

- Summary of Bruce C. Greenwald, Judd Kahn & Paul D. Sonkin's Value InvestingFrom EverandSummary of Bruce C. Greenwald, Judd Kahn & Paul D. Sonkin's Value InvestingNo ratings yet

- Behind the Curve: An Analysis of the Investment Behavior of Private Equity FundsFrom EverandBehind the Curve: An Analysis of the Investment Behavior of Private Equity FundsNo ratings yet

- What Is GPD and Why Is It So ImportantDocument3 pagesWhat Is GPD and Why Is It So ImportantJaycel BayronNo ratings yet

- NCL Industries Limited: Pay Slip For The Month of May - 2021Document1 pageNCL Industries Limited: Pay Slip For The Month of May - 2021Siva KrishnaNo ratings yet

- Brics The Rise of Sleeping GiantDocument6 pagesBrics The Rise of Sleeping GiantMarcelo Borges ValleNo ratings yet

- Human Resource Management Policy at SquareDocument4 pagesHuman Resource Management Policy at SquareAhanafNo ratings yet

- Contract DocumentDocument45 pagesContract DocumentEngineeri TadiyosNo ratings yet

- Business Plan 2024-2025Document16 pagesBusiness Plan 2024-2025lioneltran1289No ratings yet

- AsmeDocument3 pagesAsmeGaurav GuptaNo ratings yet

- The Karnataka Bank Limited Ulwe: Date: 16-05-2023Document53 pagesThe Karnataka Bank Limited Ulwe: Date: 16-05-2023Amit SinghNo ratings yet

- Ways To Preserve, Conserve and Protect Our EnvironmentDocument4 pagesWays To Preserve, Conserve and Protect Our EnvironmentMonic RomeroNo ratings yet

- NAILTA Amicus BriefDocument24 pagesNAILTA Amicus BriefOAITANo ratings yet

- Manajemen Kinerja Organisasi Dinas Koperasi Dan Usaha Mikro Kecil Dan Menengah (Umkm) Kota Pekanbaru Oleh: Aay SutinahDocument13 pagesManajemen Kinerja Organisasi Dinas Koperasi Dan Usaha Mikro Kecil Dan Menengah (Umkm) Kota Pekanbaru Oleh: Aay SutinahAnonymous 14Fqg8g68No ratings yet

- Political Economy of East Asian Development: András Székely-DobyDocument45 pagesPolitical Economy of East Asian Development: András Székely-Dobyto PhoNo ratings yet

- Professional Practice and EthicsDocument20 pagesProfessional Practice and EthicsHarshene Krishnamurhty100% (1)

- House For Rent in Gikondo-ManualDocument8 pagesHouse For Rent in Gikondo-ManualDebbie CarterNo ratings yet

- P1-2B 6081901141Document3 pagesP1-2B 6081901141Mentari Anggari67% (3)

- DIR 2DeclarationAarchieDocument10 pagesDIR 2DeclarationAarchieRich KomplianceNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument3 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceSakethNo ratings yet

- Varo Bank Account Statement: Date Description Amount BalanceDocument5 pagesVaro Bank Account Statement: Date Description Amount Balancetastefulkreationsllc45No ratings yet

- Types of ContractsDocument36 pagesTypes of ContractsmohammednatiqNo ratings yet

- James Joshua 0056340585 20230515035054Document7 pagesJames Joshua 0056340585 20230515035054Igwe4No ratings yet

- Biography of DR - Veghese Kurien: Kajal IsraniDocument15 pagesBiography of DR - Veghese Kurien: Kajal IsraniDhavalNo ratings yet

- 1551936059645Document13 pages1551936059645Samita PatawariNo ratings yet

- Lesson Plan Subject: Social Science-Political Science Class: X Month: November No of Periods: 9 Chapter: Manufacturing IndustriesDocument10 pagesLesson Plan Subject: Social Science-Political Science Class: X Month: November No of Periods: 9 Chapter: Manufacturing Industriesrushikesh patil100% (1)

- Hunar Se Rozgar TakDocument70 pagesHunar Se Rozgar TakSunil KumarNo ratings yet

- Agro Chems MrKCSabharwalDocument13 pagesAgro Chems MrKCSabharwalapi-3833893No ratings yet

- Resume IBD WSO StyleDocument1 pageResume IBD WSO StyleTesticleElephantitisNo ratings yet

- Prerne Quiz Circular 2023002Document4 pagesPrerne Quiz Circular 20230021debaNo ratings yet

- How Com Graph STDDocument21 pagesHow Com Graph STDDanae Pérez ArenasNo ratings yet