Introduction of Standard Chartered Bank History

Introduction of Standard Chartered Bank History

Download as docx, pdf, or txt

You might also like

- Standard CharteredDocument27 pagesStandard CharteredGulraiz Hamid100% (1)

- Consumer Behaviour Towards Mutual FundDocument169 pagesConsumer Behaviour Towards Mutual FundShanky Kumar100% (1)

- Ch02 TB Loftus 3e - Textbook Solution Ch02 TB Loftus 3e - Textbook SolutionDocument12 pagesCh02 TB Loftus 3e - Textbook Solution Ch02 TB Loftus 3e - Textbook SolutionTrinh LêNo ratings yet

- You Can Trust The Communists (To Be Communists) Fred C. SchwarzDocument104 pagesYou Can Trust The Communists (To Be Communists) Fred C. Schwarzfeliksch100% (1)

- Chapter 2Document10 pagesChapter 2maherchowdhury91No ratings yet

- Final Project Report of SCBDocument32 pagesFinal Project Report of SCBseth_eshita087499100% (3)

- Standard Chartered BBank Bangladesh.Document23 pagesStandard Chartered BBank Bangladesh.Suvir SahaNo ratings yet

- Sales Promotion and Customer Awareness of The Services, Standerd Charterd Finance Ltd. by Shiv Gautam - MarketingDocument67 pagesSales Promotion and Customer Awareness of The Services, Standerd Charterd Finance Ltd. by Shiv Gautam - MarketingRishav Ch100% (1)

- Project Report STANDARD CHARTERED BANKDocument51 pagesProject Report STANDARD CHARTERED BANKashishgarg100% (2)

- Business and Organisation Structure of Standard Chartered BankDocument17 pagesBusiness and Organisation Structure of Standard Chartered BankHumaira Shafiq0% (1)

- Standard Chartered BankDocument22 pagesStandard Chartered Bank12ekNo ratings yet

- Standard Chartered BankDocument17 pagesStandard Chartered BankShakil KhanNo ratings yet

- Standard Chartered Bank PakistanDocument19 pagesStandard Chartered Bank PakistanMuhammad Mubasher Rafique100% (1)

- Acknowledgement: Miss - Deepa Nair (Exim Proffessor)Document25 pagesAcknowledgement: Miss - Deepa Nair (Exim Proffessor)Avani ShahNo ratings yet

- Standard Chartered BankDocument37 pagesStandard Chartered BankFiOna SalvatOre100% (1)

- SCBLPDocument18 pagesSCBLPKamran Ali AbbasiNo ratings yet

- Standard Charted BankkDocument28 pagesStandard Charted BankkKomal SheikhNo ratings yet

- Report SCBDocument3 pagesReport SCBmostaindu07No ratings yet

- EVALUATION OF MUTUAL FUND INDUSTRY (Akbar)Document61 pagesEVALUATION OF MUTUAL FUND INDUSTRY (Akbar)AKBARKHAN7777No ratings yet

- Internship Report On Sme Banking and Procedures of Standard Chartered BankDocument59 pagesInternship Report On Sme Banking and Procedures of Standard Chartered BankSaif Azman67% (3)

- Research Project ReportDocument77 pagesResearch Project ReportsumitNo ratings yet

- Collection of Data by Conducting Interviews of Officials of The Bank Frequent Visits Internet Search Study of Bank's Annual ReportsDocument19 pagesCollection of Data by Conducting Interviews of Officials of The Bank Frequent Visits Internet Search Study of Bank's Annual ReportsFarjana Islam MouNo ratings yet

- Standard Chartered BankDocument4 pagesStandard Chartered BankSumeet MetaiNo ratings yet

- Standard Chartered HR Intern Report BangladeshDocument65 pagesStandard Chartered HR Intern Report BangladeshNeeloy Hoque50% (4)

- Chapter-3 Canara Bank Profile Origin of Canara BankDocument6 pagesChapter-3 Canara Bank Profile Origin of Canara BankSubramanya DgNo ratings yet

- Standard Chartered BankDocument19 pagesStandard Chartered BankShahbaaz PatelNo ratings yet

- Standard Chartered Bank ProfileDocument8 pagesStandard Chartered Bank ProfileNeeloy HoqueNo ratings yet

- Standard Chartered BankDocument12 pagesStandard Chartered BankNikita JainNo ratings yet

- Standard Chartered GroupDocument9 pagesStandard Chartered GroupALI100% (1)

- Foreign-Banks in Pakistan (Financial Institutions)Document7 pagesForeign-Banks in Pakistan (Financial Institutions)Zubair BhattiNo ratings yet

- Standard Chartered Bank of PakistanDocument29 pagesStandard Chartered Bank of PakistanMian Ali Raza RafiqNo ratings yet

- Standard Chartered Bank Nepal MISDocument23 pagesStandard Chartered Bank Nepal MISManishDangolNo ratings yet

- A Study On Attrition Rate in Standard Chartered Bank Jaat BudhiDocument78 pagesA Study On Attrition Rate in Standard Chartered Bank Jaat Budhikhrn_himanshuNo ratings yet

- Canara Bank: A Brief Profile of The BankDocument14 pagesCanara Bank: A Brief Profile of The BankAppu Moments MatterNo ratings yet

- Standard Chartered BankDocument56 pagesStandard Chartered BankTarekNo ratings yet

- Strategic Human Resource Management Practices of Standard Chartered BankDocument39 pagesStrategic Human Resource Management Practices of Standard Chartered BankM.Zuhair Altaf63% (19)

- History: The Chartered BankDocument7 pagesHistory: The Chartered Bankketakm99No ratings yet

- SCB Assignment by MGTDocument27 pagesSCB Assignment by MGTfarahNo ratings yet

- Canara Bank ProfileDocument13 pagesCanara Bank ProfileRaveendra BatageriNo ratings yet

- Executive SummaryDocument83 pagesExecutive Summarysimranarora2007No ratings yet

- Where To Invest-Ulip or Mutual Funds: An Investor'S GuideDocument91 pagesWhere To Invest-Ulip or Mutual Funds: An Investor'S GuidetalupurumNo ratings yet

- Anking Ndustry IN Angladesh: 1.1 Industry BackgroundDocument31 pagesAnking Ndustry IN Angladesh: 1.1 Industry BackgroundpixytanyNo ratings yet

- Financial Statement Analysis of Bank AsiDocument37 pagesFinancial Statement Analysis of Bank AsiFahim AlamNo ratings yet

- ReportDocument9 pagesReportLakshya AggarwalNo ratings yet

- Section 2 ReferencedDocument6 pagesSection 2 ReferencedAwesum Allen MukiNo ratings yet

- Investment Banking AssignmentDocument4 pagesInvestment Banking AssignmentsssssssNo ratings yet

- Letter of Transmittal: Subject: Submission of Standard Chartered Bank Reports For The Course of Human ResourceDocument13 pagesLetter of Transmittal: Subject: Submission of Standard Chartered Bank Reports For The Course of Human Resourcetaseen rajNo ratings yet

- Report NBP WorkingDocument7 pagesReport NBP WorkingAnnie DollNo ratings yet

- Job Satisfaction of Employees: A Study On Standard Chartered BankDocument29 pagesJob Satisfaction of Employees: A Study On Standard Chartered BankStacy D'SouzaNo ratings yet

- Canara BankDocument18 pagesCanara BankparkarmubinNo ratings yet

- Prime Commercial Bank LimitedDocument48 pagesPrime Commercial Bank LimitedakhlaqNo ratings yet

- History: Late Sri Ammembal Subbarao PaiDocument13 pagesHistory: Late Sri Ammembal Subbarao PaiurmiNo ratings yet

- Islamic Banking Project On BankIslami PaDocument15 pagesIslamic Banking Project On BankIslami PaAleena FayyazNo ratings yet

- Algerian Islamic Banks: The Role of Relationships Marketing Tactics and Customer LoyaltyFrom EverandAlgerian Islamic Banks: The Role of Relationships Marketing Tactics and Customer LoyaltyNo ratings yet

- Accounting, Auditing and Governance for Takaful OperationsFrom EverandAccounting, Auditing and Governance for Takaful OperationsNo ratings yet

- Takaful Islamic Insurance: Concepts and Regulatory IssuesFrom EverandTakaful Islamic Insurance: Concepts and Regulatory IssuesRating: 4 out of 5 stars4/5 (1)

- Marketing of Consumer Financial Products: Insights From Service MarketingFrom EverandMarketing of Consumer Financial Products: Insights From Service MarketingNo ratings yet

- Banking India: Accepting Deposits for the Purpose of LendingFrom EverandBanking India: Accepting Deposits for the Purpose of LendingNo ratings yet

- Bankins System in India HistoryDocument9 pagesBankins System in India HistoryHappy SinghNo ratings yet

- PaySlip (October)Document2 pagesPaySlip (October)karansharma690No ratings yet

- FIN 301 B Porter Rachna Soln.Document3 pagesFIN 301 B Porter Rachna Soln.Seema KiranNo ratings yet

- StatementDocument4 pagesStatementlorielys0909No ratings yet

- Comparison Between Ulips and Traditional PlanDocument4 pagesComparison Between Ulips and Traditional Planpayal_31No ratings yet

- Chinese Yuan SolutionDocument1 pageChinese Yuan SolutionTrang QuynhNo ratings yet

- Week 6 Tutorial Answers (PAVLON, DD & ECHO)Document6 pagesWeek 6 Tutorial Answers (PAVLON, DD & ECHO)ZHUN HONG TANNo ratings yet

- Acct Statement XX0311 07062022Document4 pagesAcct Statement XX0311 07062022RAJKUMAR NAYAKNo ratings yet

- Capm & AptDocument23 pagesCapm & AptBhakti Bhushan MishraNo ratings yet

- Glossary of Real Estate TerminologiesDocument46 pagesGlossary of Real Estate TerminologiesJen Manrique100% (1)

- Small Enterprises Fesability StudiesDocument19 pagesSmall Enterprises Fesability StudiesMina Samy abd el zaherNo ratings yet

- Excel Sheet With Final Accounts Question, No Adjustments , And Templates for Financial Statements..Xlsx Worked OutDocument7 pagesExcel Sheet With Final Accounts Question, No Adjustments , And Templates for Financial Statements..Xlsx Worked OutmarriettaconslateNo ratings yet

- Chapter 9: Cash in SafeDocument5 pagesChapter 9: Cash in SafeKumera Dinkisa ToleraNo ratings yet

- Branch Teller: Use SCR 008765 Deposit Fee Collection State Bank CollectDocument1 pageBranch Teller: Use SCR 008765 Deposit Fee Collection State Bank CollectNishchay Kumar RaiNo ratings yet

- Bank Management System: International Journal of Engineering Research in Computer Science and Engineering (Ijercse)Document6 pagesBank Management System: International Journal of Engineering Research in Computer Science and Engineering (Ijercse)Andenet TesfahunNo ratings yet

- Audit of Liabilities-Part 1 - SolutionsDocument13 pagesAudit of Liabilities-Part 1 - SolutionsNicko Angelo E. CrisostomoNo ratings yet

- Know Your Money HandbookDocument29 pagesKnow Your Money HandbookAnonymous cS9UMvhBqNo ratings yet

- SPR NutshellDocument6 pagesSPR NutshellZenith JinaNo ratings yet

- Hedge Fund Investment StrategiesDocument386 pagesHedge Fund Investment Strategiesjk kumar100% (1)

- SOC Credit Card MayDocument20 pagesSOC Credit Card MayBDT Visa PaymentNo ratings yet

- Instructions:: Assignmnet 2 - Chapter 7 (Petty Cash & Bank Reconciliation)Document5 pagesInstructions:: Assignmnet 2 - Chapter 7 (Petty Cash & Bank Reconciliation)Success LibraryNo ratings yet

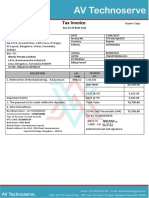

- AV Tech 04 2023 Invoice Kaviyarasan.Document1 pageAV Tech 04 2023 Invoice Kaviyarasan.Director LMNo ratings yet

- Cash Flow Statement Classification of ActivitiesDocument4 pagesCash Flow Statement Classification of ActivitiesAanchal MahajanNo ratings yet

- 2021 PDFDocument9 pages2021 PDFNekhavhambe MartinNo ratings yet

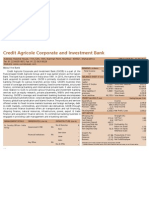

- Profile-Foreign Banks-Credit Agricole Corporate and Investment BankDocument1 pageProfile-Foreign Banks-Credit Agricole Corporate and Investment BankAnimesh LodhaNo ratings yet

- Financial Management Process of Leading UniversityDocument52 pagesFinancial Management Process of Leading UniversityHumayun KabirNo ratings yet

- PNB Ze Lo Mastercard - App Form OnePager - Jan2020 1Document9 pagesPNB Ze Lo Mastercard - App Form OnePager - Jan2020 1Crypto ManiacNo ratings yet

- Excel 2Document6 pagesExcel 2rupasana157No ratings yet