0% found this document useful (0 votes)

471 viewsTime Value

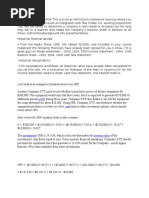

The document provides 20 examples of time value of money calculations involving concepts like present value, future value, compound interest, effective interest rates, and yield calculations. The examples calculate financial values for scenarios like investments growing over several years, loans, bonds, savings accounts, tuition costs, and more. Formulas used include FV=PV(1+R/100)^T to calculate future or present values based on given interest rates and time periods.

Uploaded by

Bhaskar VishalCopyright

© Attribution Non-Commercial (BY-NC)

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

471 viewsTime Value

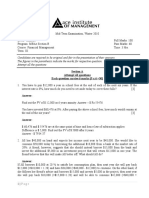

The document provides 20 examples of time value of money calculations involving concepts like present value, future value, compound interest, effective interest rates, and yield calculations. The examples calculate financial values for scenarios like investments growing over several years, loans, bonds, savings accounts, tuition costs, and more. Formulas used include FV=PV(1+R/100)^T to calculate future or present values based on given interest rates and time periods.

Uploaded by

Bhaskar VishalCopyright

© Attribution Non-Commercial (BY-NC)

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

/ 10