0 ratings0% found this document useful (0 votes)

274 viewsThe Smart

The document summarizes the SMART car project launched as a joint venture between Swatch and DaimlerChrysler. The SMART was intended to revolutionize the automotive industry by offering an affordable, small urban car. It was produced in a new factory in France and aimed to compete in the growing mini/small car market segment. However, unlike the successful Swatch watches, the SMART failed to achieve critical mass or profitability after its 1997 launch. Questions remain about the project's strategy and whether it should be discontinued.

Uploaded by

Chin Ting Xuan CrystalCopyright

© © All Rights Reserved

Available Formats

Download as PDF, TXT or read online on Scribd

0 ratings0% found this document useful (0 votes)

274 viewsThe Smart

The document summarizes the SMART car project launched as a joint venture between Swatch and DaimlerChrysler. The SMART was intended to revolutionize the automotive industry by offering an affordable, small urban car. It was produced in a new factory in France and aimed to compete in the growing mini/small car market segment. However, unlike the successful Swatch watches, the SMART failed to achieve critical mass or profitability after its 1997 launch. Questions remain about the project's strategy and whether it should be discontinued.

Uploaded by

Chin Ting Xuan CrystalCopyright

© © All Rights Reserved

Available Formats

Download as PDF, TXT or read online on Scribd

You are on page 1/ 29

INSEAD

MBA PROGRAMME P3, February 2003

Main Project

Innovation Strategy and Entrepreneurship

Professor Ron Adner

The SMART

Group 4, Section A

Salah Belkhayat

Gokhan Gunes

Ana Fontes

Ricardo Camilher Gomes

David Doral

Abdulmonem Suliman

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 2

TABLE OF CONTENTS

EXECUTIVE SUMMARY.................................................................................................3

SMART IN CONTEXT.......................................................................................................4

SMART at Birth...........................................................................................................4

Affected Markets..........................................................................................................4

Initial Expectations: Timing & Size ............................................................................5

The State of the Automotive Industry..........................................................................6

SMART MARKET DYNAMICS........................................................................................7

Demand Side................................................................................................................7

Value Proposition and Differentiation.........................................................................8

SMART APPROACHES TO INNOVATION....................................................................9

Product/Design innovation...........................................................................................9

Supply Chain/Process Innovation..............................................................................10

Distribution ................................................................................................................13

EVOLUTION OF PRODUCT AND LESSONS LEARNED ...........................................14

Todays Situation.......................................................................................................14

Expectations and the Creation of New Markets.........................................................15

Why did MCC build an expensive car? .....................................................................16

Future Strategy...........................................................................................................17

Did Mercedes Over -reach? ........................................................................................18

Resource Commitment and Reversibility ..................................................................19

Conclusion .........................................................................................................................20

REFERENCES ..................................................................................................................21

Appendix 1 SMART Chronology...................................................................................22

Appendix 2: Prices and characteristics of substitutes ........................................................24

Appendix 3: Sales figures for the Mini-car segment .........................................................27

Appendix 4: Passenger Car Production in Western Europe by Segment ..........................28

Appendix 5: Mobility Offerings and Partnerships ............................................................29

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 3

EXECUTIVE SUMMARY

Towards the end of 1980s, Nicholas Hayek, who was behind the success of Swatch

watches, came up with the concept of the SMART car. He wanted to change the way

people buy cars and incorporate Swatch-like values of affordable fashion and lifestyle

into a car concept. Hayek partnered with DaimlerChrysler in a joint venture called Micro

Compact Car (MCC) to develop a product that would create a unique value proposition

for the automobile industry.

From its design to its supply chain, production, marketing and distribution processes, the

SMART was a true innovation. The SMART project was developed in a totally new site,

the so-called SMARTville, in the French village of Hambach. By forming various

partnerships with suppliers and dealers, MCC challenged the existing rules of the car

industry with a breakthrough product and new processes along the value chain.

The SMART was intended to be a modern, ecologically conscious car mainly targeted at

a growing segment: urban young consumers and dinks (double income no kid

couples). One of the principal value propositions of the SMART was its mobility

concept: its small size and special services would address increasing concerns of lack of

space in the European urban centers.

Unlike the Swatch watches, the SMART car failed to reach the critical mass. Six years

after its launch, the breakeven point of the SMART project is still at least two years down

the road and there are serious questions arising on whether the project should be

discontinued or not.

The implementers of the SMART project are currently struggling to make it profitable

and have added new models that deviated from the initial SMART concept. The tradeoff

that managers are facing today is to make the SMART more acceptable to the mass

market without erroding the original concept that differentiated their offering from other

small cars..

In this report we will analyze the innovations proposed by the SMART project in terms

of its design, supply chain, production, marketing and distribution processes. We will

also analyze what values were delivered by the product, how the market perceived these

values and whether management expectations were reasonable. SMART is currently

marketed in twenty eight countries. This report will mainly focus on Western Europe,

SMARTs core market.

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 4

SMART IN CONTEXT

SMART at Birth

It all began in 1989, eight years before the first SMART car would come off production

lines. Nicholas Hayek, founder and CEO of the Swatch Group, the Swiss manufacturer of

watches, was trying to revolutionize the automotive industry in the same way that he did

with the Swatch watches. In 1983, he had proposed the idea of launching a low cost, high

tech and emotional watch to compete with the low cost watches manufactured in Asia.

Eleven years later, the Swatch had sold more than 150 million units and Swatch Group

accounted for 25% of watches sold in the world. Coming back to the car, his idea was to

offer an ecologically friendly car for two adults and imitate the Swatch idea with low

price, high quality, special design and innovation. He also wanted to enhance the

purchasing experience by placing show rooms in shopping malls and airports. In 1991,

Swatch signed a deal with Volkswagen to develop the car, but a year later, the

partnership was ended because the newly-appointed CEO of Volkswagen did not believe

in the concept.

In the meantime, Mercedez-Benz, the passenger car and truck brand of DaimlerChrysler

Group, had already tried to enter in the mini car segment in the 70s and 80s but did not go

beyond the concept phase because it was too busy fighting strong competition from the

Japanese manufacturers in the luxury sedan market. Also, Mercedes-Benz was concerned

about its image because the average age of its drivers was fifty three. Realizing that it

needed to react to stiff competition, the company continued to look for new market

segments in order to increase its business and extend its brand image. At that moment,

the company turned its attention to the small car market. The entrance in this market

posed two main issues to Mercedez-Benz: 1) technological: the company had always

produced large and rear wheel cars in contrast with the small front wheel cars; and 2)

financial: beside the high risk for taking on small car projects that were outside the

companys core business, the small car market was known for its low margins and strong

competition.

In 1994, after considering its debut in the mini car segment, Mercedez-Benz signed a

partnership agreement with Swatch and founded MCC. Under this partnership, Mercedes

would be in charge of the production and Swatch would take care of the marketing. In the

same year they chose the factory site. It was a 173-acre area outside the French village of

Hambach. In 1997, the factory was inaugurated and the project received investments of

around 2.5 billion in production and marketing.

Affected Markets

Although the original concept was marketed as a brand new mode of urban transportation

revolutionizing the automotive industry, SMART was initially going to compete within

the small car market. The small car market has been defined in the industry as composed

of two segments:

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 5

Mini (A) Small (B)

Engine Less than 1000 cc 1000 1500 cc

Body Style Miniature, 2 doors Variety of trims, 2 & 4 doors

Length Less than 3m (10 ft) Less than 3.745 m (12.5 ft)

Available

Brands 1998

Fiat Seicento, Ford Ka, Suzuki

Alto and Daewoo Matiz.

Ford Fiesta, Renault Clio, Nissan

Micra, Peugeot 206

The small and mini cars had enjoyed strong sales in the Western European market (see

appendix 3 for sales figures of mini cars in western Europe). While the B segment

accounted for around 25% of Western Europeannew car demand, the A segment claimed

under 5%. However the A segment was predicted to grow faster than the B segment

taking share mainly from the B segment with total market share of A and B remaining

fairly flat around 30%. Appendix 4 shows actual and projected production for 1998 and

2004 respectively for all segments in Western Europe.

The first mini cars were mainly sold to lower income groups who were looking for

inexpensive and low maintenance cars. Italy represented the biggest market in Europe

65% of the European market for mini cars. In the late 1980s and early 1990s, the A and B

segments had to respond to the evolution of a new customer segment. The se new

customers were now looking for style and similar performance in terms of quality and

safety as that of the large r automobiles.

Initial Expectations: Timing & Size

The SMART car was initially planed to be launched in March 1998. At that time,

managers at Mercedes were expecting very optimistic sales of 200,000 cars per year. The

200,000 cars per year sales would be enough to breakeven the plant. Sales were targeted

at 300,000. More recently, breakeven was expected to be reached in 2004.

1994

Estimated Break-Even: 200,000 units

Target Sales: 300,000 units

Expected

launch of

the SMART

Expected

Break-Even

Mercedes and the

Swatch Group

agree on the

creation of the joint

venture

1998 2004

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 6

The State of the Automotive Industry

At the time of the launch of the SMART, the automotive industry was marked by

consolidation of car markers, outsourcing of suppliers, lean manufacturing and low

growth prospects.

Consolidation of car makers

Industrial consolidation was a key trend in the global automotive industry. Shortly after

the launch of the SMART, Nissan and Renault agreed to tie-up by Renault taking a

minority stake in the Nissan. Volkswagen had acquired Seat in 1986 and Skoda in 1990.

BMW purchased Rover in 1994.

Outsourcing and consolidation of the supply industry

As car makers seeked to cut costs, they outsourced more and more to the supply industry.

Outsourcing of suppliers allowed greater economies of specialization and scale, since

suppliers were more experienced in certain functions and could supply several carmakers.

Consolidation of suppliers was also expected to intensify under cost pressure from the

automakers.

Lean manufacturing

Following the 80s automation trend, the automotive industry adopted the Japanese

model of lean manufacturing seeking to reduce waste through the best possible

utilization of resources (human resources, capital investment, factory space and

materials)

Low Growth Prospects

The financial crisis in Asia, South America and Russia crisis led to an expected decline to

13.8m unit sales in Western Europe in 1999 and a further more decline in 2000.

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 7

SMART MARKET DYNAMICS

Demand Side

Hayeks vision for the SMART was an ecological, trendy, urban and affordable car. The

primary target market was the urban young consumers and dinks (double income no

kid couples). MCC also planned to sell the SMART to families as a second or third car,

as well as young-at-heart senior citizens and businesses in general.

Given the offering and the target customer, we can argue that SMART was fighting for

buyers of class A and B vehicles, and maybe also for some sort of potential buyers of a

brand new sub-segment between those cars and other 2-3 wheel city vehicles like

scooters.

According to EIU Motor Business International the buying decision for small cars was

driven by the following main reasons:

Space Confined city centers required small cars which are easy to park and

manoeuvre.

Price Small cars were usually the first car purchase for many young customers

especially in Europe where car s are very expensive. Auto makers considered the mini

cars as an entry point for customers who would later upgrade to larger (and more

profitable) models.

Other factors included lower fuel consumption and lower excise taxes.

Most new car buyers were bypassing the mini (A) segment and moving straight to the

small (B) segment. Surveys had shown that one reason for this move was the perceived

lack of safety when sharing lanes with larger SUVs and MPVs (please refer to appendix

4). The small price difference between the minis and the smalls also blurred the

distinction between these two categories.

Overall, the total volume of A and B class cars sold in Western Europe was not expected

to change. However, class A segment was expected to grow and steal market share from

the class B segment. European car manufacturers that catered to both markets with a

single model were starting to introduce new models (e.g., Renault added Twingo below

Clio, VW introduced Lupo below the Polo).

From 1995 to 1998 European mini-car sales hadgrown from 500,000 units to 1,031

million surpassing the Japanese market as the biggest market for mini cars. Italy, France

and Germany were the main markets accounting for 70.4% of mini-car sales. From 1998

on, the mini cars segment was expected to grow 38% until 2004. The main players in this

market were the Ford KA, Renault Twingo and Fiat Seicento.

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 8

As we can see, the SMART was up against strong competition and a variety of potential

substitutes, and the initial expectations of sales of 300,000 cars a year, or 30% of the

small car segment, seemed a little bit too ambitious for a market which main driver, price,

was not exactly SMARTs strength.

Value Proposition and Differentiation

The SMART marketing team knew that style and fashion were not enough to distinguish

their offering from the competition. To differentiate itself from the small car pack, MCC

offered the mobility concept in addition to the SMART car. Mobility referred to a set

of services ranging from discounted rental car rates to train tickets for SMART owners. It

also included preferred rates for parking garages as well as ferries and other means of

transporting the SMART car between cities (see appendix 5 for a sample of current

mobility offerings). These services were marketed as a complete lifestyle package

designed for the modern, ecologically conscious European urban dweller.

As we will analyze in coming sections, SMART experienced production delays and

disappointing first sales, as well as problems negotiating and building the mobility

network of agreements with mass transportation authorities and parking garages. In

response, the management decided to change the marketing message during the re-launch

of 1999. The message was going to focus on the unique technology of the cars rather than

the mobility concept.

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 9

SMART APPROACHES TO INNOVATION

Product/Design innovation

The SMART is based on a rigid integral body frame / safety cell (called TRIDION) to

which such flexible body panels as doors, the front and rear panels and (the optional

glass) roof are attached. The final buyer can customize the product by combining two

colours of the frame (black and silver) with the different colors of the body panels.

Despite a high customization perception there is low variation in production.

Initially, the SMART was equipped with a basic 600cc, 3-cylinder engine in two tuning

levels that provided 45hp (33.5KW) and 55 (41KW) respectively. This engine evolved

into a more powerful one with three power variants: 50hp (37KW), 61hp (45KW) and

75hp (55KW). Also, a diesel engine was added with 800cc and 41hp (30.5KW).

The engines can be combined with either a half-automatic transmission, the denominated

softip that allows to change gears with a tap on the gearshift without using the clutch, or a

full-automatic transmission, the softouch, with a kickdown function that allows to change

down one or two gears simultaneously by pressing the accelerator to the floor when extra

power is needed, for instance in overtaking maneuvers. Both are based on the same six-

speed sequential gearbox.

Initially, three variants were available to the client (SMART & Pure, SMART &

Pulse and a SMART & Passion). The variations differ in interior trim, body colours,

comfort features and engine power. To these variants, a sporty version was added later

on, the Brabus. The modular product layout enables MCC to supply customer choice with

minimum product complexity.

As most of the features are easy to add, both at the assembly line and during the life span

of the car, variation in customer demand hardly interferes with production processes. For

example, the interior trim (fabric and color) consists of exchangeable panels, easy to

mount at the assembly line and even easy to be exchanged by the owner afterwards.

Moreover, features as ABS or electric windows might have disturbed production if made

optional, but they were integrated as standards in the car. The after sales extras include a

wide range of easy to attach peripherals such as CD player, GPS navigator , etc.

On top of the above-mentioned customisation, the modular concept enables the customer

completely to renew and upgrade the product during its lifetime. Product features can be

added and body parts (more colors!) can be changed in the SMART-centre. Moreover,

the modular concept makes it possible for the designers and engineers of MCC and its

suppliers quickly to develop and implement minor and major product redesigns.

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 10

For example, within six months after the introduction of the car, the first extension of the

product offering was already introduced. Two additional colors (on top of the various

basic ones) were introduced. The trick here is to use a form of cubic printing. This

technique uses not only a basic color but adds a color film on top of it (orange and green

in this case) in a random pattern (like the spots on a cow), making each panel unique. The

input of Swatch in the concept development is clearly visible here. Within the existing

product architecture of easy-to-assemble products, new options and features are

introduced at a rapid pace. This adds to the fashionable character of the product: constant

change and improvement.

The modular concept has also allowedengineers to extend the product line within limited

time span, by changing the form of body panels and interior components while keeping

the basis of the car (the TRIDION safety cell) unchanged. This modular approach is not

new in other fields, like the software industry, with the Object Oriented programming

philosophy, which is one of the main features of languages like JAVA. However, the

attempt to apply this concept to the automotive industry was pioneered by SMART.

In sum, through smart product development, the engineers of MCC have achieved (the

perceived) customization, while at the same time, limiting product variation and

production complexity.

Supply Chain/Process Innovation

The modular concept, as well as, technological innovations has enabled MCC to produce

a car from no more than 40 to 50 modules and parts.

The SMART's manufacturing process is just as unique as the product itself. The

partnership model practicedin Hambach, the assembly plant in France, embodies the

logical development of the conventional manufacturer/supplier relationship. Thus the

carmaker bears overall responsibility and is also the module system integrator, process

manager and manufacturer. At the same time, however, each system partner also shares a

considerable amount of responsibility. The advantage of this modern form of co-

operation is that it motivates the partners to contribute to the success and the achievement

of the corporate goals by means of their own input and ideas.

The production system, known as smart-Plus, is in the shape of a cross. This layout

enables maximum flexibility with excellent quality. The SMART production system is

held in high esteem by relevant experts. Only 4.5 hours are required for the final

assembly of a SMART.

Apart from the body, the TRIDION, the car consists of several main modules, namely:

the rear module including the driveline, the doors and the cockpit, each containing sub-

modules and components. The modules are supplied in sequence for final assembly, by a

small number of first tier suppliers, of who seven are fully integrated in the final

assembly site.

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 11

Modules are bought by the MCC only as they are needed in the final assembly process.

For example, a complete rear module, including among other things: rear axles,

transmission, sus pension and engine, is pre-assembled by one supplier who starts

assembling the module only upon demand by MCC and not earlier than one and half hour

before the module is needed on the final assembly line. The same is true of the doors (3-

hour lead-time) and the dashboard system (1-hour lead-time).

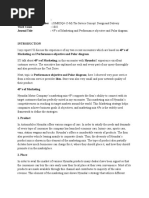

To ensure a smooth flow of goods within the plant, the car is moved along the work

stations of the assembly line, which is laid out in the form of a cross (see exhibit 1).

Exhibit 1: The SMART plant lay out

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 12

Arguments for this plant layout were to permit high-frequency deliveries at a large

number of offloading ramps, while keeping transport to a minimum. Sub-sections can

also work independently to avoid system disruptions in case of malfunction at one

particular point along the assembly line. Furthermore integrated suppliers are able to

supply their finished products directly to the final assembly line or on a conveyor system.

In the SMART-ville the manufacturing process starts with Magna assembling the

TRIDION body in white. This process is highly automated and standardised; Magna

employs 130 robots. In fact, this is one of the very few automated process steps.

Operators mostly perform subsequent steps. The finished body in white is then passed on

to the next partner in the adjoining, connected facility. In that step Surtema (an

Eisenmann subsidiary) primes and paints the body using paint tunnels for each of the two

colours (black and silver/grey). The process is based at powder-coating; it has been

developed especially for SMART and is environment friendly. After painting, the body is

transferred by conveyor belt to the beginning of the cross shaped assembly line. Starting

at the top of the cross, Siemens VDO assembles cockpits and mounts them to the body. In

the three other sections of the cross MCC goes on assembling the car, starting with the

mechanics and chassis, followed by external and internal trim assembly, inspection and

testing. The rear module (including the drive train) is pre-assembled by Krupp Hoesch

and undergoes several additional assembly tasks by workers of MCC on a small island

adjacent to the cross. Following assembly, the rear module is brought to the line on a

telescopic carrier that raises it to shoulder height, enabling operators to guide it into the

car.

During the assembly process, modules and components are delivered line-side (within 10

metres from the workstation) on a just-in-time basis. For example, complete front-end

and rear-end modules are delivered by Bosch and Krupp, respectively. Dynamit Nobel

delivers the plastic outer body panels molded on site. The door panels are delivered to

Magna Door Systems who pre-assembles the panels to complete doors, before delivering

them line-side.

The seven integrated suppliers are responsible for the supply of around 70% of the

volume and 30-40% of the value of the finished product. In addition, 16 non-integrated

suppliers deliver sub-modules and parts to both MCC and the integrated suppliers.

These non-integrated suppliers add about another 20% of the volume to the car. Their

supplies include seats, wheels, windows, etc. and are delivered to the relevant docking

station of the assembly line, at a maximum distance of 10 meters. The remaining 10% of

the volume consist of standard and small parts not linked to a particular module, which

are stored in an on-site warehouse, operated by a third party.

Although integration with suppliers is up to some extent always accomplished by todays

car manufacturers, this level of integration, both physically (MCC and suppliers work in

the same building) and value-wise, (the in-house manufacturing rate is less than six

percent - a figure which is unsurpassed in Europe) is on of MCCs major production

breakthroughs

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 13

MCC is also setting standards in terms of environmental compatibility at its plant in

Hambach. Stringent regulations to protect water, soil, air and the surrounding landscape

and also relating to energy saving and the protection of resources have been in force since

production started. Environmental protection is also extremely high on the agenda in the

development, use and also, ultimately, the recycling of SMART cars

Distribution

The first SMARTs were launched in Austria, Benelux, France, Germany, Italy, Spain,

and Switzerland. Subsequent geographical expansion included Portugal, Scandinavia,

UK, Taiwan, Japan, Hungary, Tchek Republic, and Croatia.

Mercedes decided to build a new distribution channel exclusively dedicated to the

SMART project. The main motivation behind this move was to isolate the luxury car and

SMART brands and avoid the potential erosion of sales if these two were to share the

same retail space.

The dealers were selected from a mix of existing Mercedes Benz dealers, dealers for

other brands and newcomers to auto dealers hip. The franchise dealers were given

exclusive territory rights but were expected to sell around 1500 cars.

The SMART distribution concept was based on sales towers, the SMART centers,

located near the big shopping centers. The costumer should be able to see his car, decide

to buy it and take it away immediately.

Exhibit 2: Example of SMART centers.

The decision to go for an independent distribution channel ended-up adding considerable

costs to the project. MCC initially planned to build 100 SMART centers and the

necessary investment was around US$ 2.5 to 3 million per tower.

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 14

EVOLUTION OF PRODUCT AND LESSONS LEARNED

Todays Situation

The SMART is currently 100% owned by DaimlerChrysler. At the end of 1998

DaimlerChrysler took over the interest of The Swatch Group Ltd. in the joint venture. In

September 2002, SMART was repositioned from being an independent company and

became the small car brand of Mercede s-Benz.

Since 1998, the SMART division and the Mercedes Group have had disappointing

results. Both Mercedes Group and the SMART division replaced their CEOs. A number

of restructuring plans have revised breakeven expectations and lowered sales and profits

targets.

In the mean time, other automotive companies launched cars that compete with the

SMART in the market of small trendy cars: the VW New Beetle and the BMW Mini.

Although these two models can be included in the mini car segment, they are

significantly bigger than the SMART.

After six years on the market, SMART has not yet reached break-even leading to

speculation -- denied by the company -- that DaimlerChrysler might sell or close the unit.

SMART unit sales

1998 1999 2000 2001 2002 2003 2004

20,000 80,000 101,000 116,000 122,300 115,000 140,000

Source: Mercedes Benz company releases.

Analysts at the US investment bank Morgan Stanley claim that SMART loses more per

car than any other volume brand in recent history, except Rover , and that restructuring or

closing the division would be a "high-return investment" and the situation of BMW-

Rover cars in 2000 should be studied in order to learn from others mistakes and the way

they solved them.

Making the SMART profitable is the top priority for newly appointed head of Mercedes-

Benz division, Eckhard Cordes. Eckhard became head of the division in October 2004

and at the end of the year ordered a complete review of the SMART line.

Under the new strategic plan the SMART division should start to make pr ofits within

three or four years. SMART originally hoped to be profitable by the financial year 2004,

an objective put back to 2006 in October of last year.

Launch of

the

SMART

Break-

Even

Mercedes and the

Swatch Group agree

on the creation of

the joint venture

Expected

2006

Actual

Oct98

1994 Mar98 2004

Launch of

the

SMART

Break-

Even

Mercedes and the

Swatch Group agree

on the creation of

the joint venture

Expected

2006

Actual

Oct98

1994 Mar98 2004

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 15

Expectations and the Creation of New Markets

The SMART sales have not met expectations. Sales in 2004 are still more than 60,000

units short from the break-even figure of 200,000 units, and the promise to reach

profitability has been postponed another two years.

Were the original expectations too high?

The main feature of the SMART was its reduced dimensions and its trendy look. This

should have appealed to potential customers as a very convenient and fashionable way of

driving and parking in highly congested cities, while providing more comfort and safety

than a motorbike.

We believe that MCC overestimated the demand for an extra-small trendy urban car. The

target sales figure (300,000 units according to the automotive press) was 30% of the

European mini car market. MCC was obviously not planning to instantly capture that

much market share from the existing segment. The management must have planned to

grow the market by creating new demand. One can put forward some reasons why

demand may have been lower than expected:

Parking may be a problem in crowded cities, but it is not a strong enough reason

to drive the purchase of an extra small car. Even though it provides an

improvement, the SMART does not completely solve the parking problem.

SMART is very small. In a two-seater, a couple cannot take along a friend, a

child, or a few pieces of luggage for a short road trip.

A lot of reviews complained about a perception of exposure when driving

alongside bigger cars and buses.

Did SMART fail to differentiate itself?

The SMART had many close substitutes. Even though SMART was marketed as a

revolutionary product, it was introduced in a crowded and competitive market. The A and

B segments were extremely price sensitive, and the buyers needed a lot of added value if

they had to pay a price premium for a small car.

SMART packed a lot of sophisticated features for a tiny car. It was relatively expensive

compared to other small cars such as Ford Ka, Peugeot 106 and Citroen C2 (See

Appendix 2 for sample pricing for small cars). In that respect it was stuck in the middle

of a price-sensitive small car market and the expensive sport luxury market. We see here

some sort of awkward compromise among three main factors that usually drive the

purchase of a car: functionality, price and social status (or style). SMART wanted to

achieve status symbol (with a trendy design), and function (practical urban mobility) in

order to justify its steep price for a tiny car and may have failed to do so.

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 16

The mobility concept also failed to differentiate the offering. The SMART was conceived

to be more than a car: it tried to be a new means of transportation for young and

environment conscious urban people. The initial plan shaped by Hayek, Swatch founder,

included a set of services and partnerships designed to meet all the transportation needs

of the SMART owners (see Appendix 5).

But this mobility idea, far from crystallizing as an intrinsic part of the SMART concept,

simply became another add-on that was not even available at all in most of the countries

where the SMART was launched. Arranging extensive agreements with rental car

companies, parking garages, airlines and train services turned out to be much more

complex than expected. After all, it was completely out of the core competences of both

partners, Swatch and Daimler, and was not developed enough to attract additional

customers. The concept was later taken out of the marketing message and replaced with

an emphasis on the technical features of the car.

Why did MCC build an expensive car?

There can be some reasons why MCC ended up building a car more expensive than

expected.

Modularity: Even though Daimler top management states that the modular

production concept provides cost savings, we argue that it introduces enough

complexity to negate the cost savings of plain mass production. Eliminating the

customizable offering could have reduced the trendiness, but in return the final

price could have been reduced too. As argued before, we consider price a more

powerful driver in buying a small car than nice looks.

Sophistication: Daimler probably pushed for that sophistication, afraid of being

related with a cheap car. Thus, all the SMART models feature a host of safety

features as standard. In addition to an electronic stability control system, all

SMARTs feature ABS, electronic brake power distribution, full size driver and

passenger airbags, seatbelt tensioners and belt force limiters. Another example of

that quality commitment over other drivers like price is the extra 150million

Daimler was forced to invest to solve some safety issues raised when the car

flipped over during extreme maneuvering tests

1

, a very similar case to what the

Mercedes A class had to go through. Daimler finally created a tiny car with more

and better technical features than the typical segment A car, and it give the

SMART and overall perception of stylish design. All of those came at a cost,

which raised the price too much, and the new tiny segment finally did not have a

tiny price, something that seemed to be part of the core original idea.

1

http://news.bbc.co.uk/1/hi/oldbusiness/40900.stm

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 17

Lack of synergies: Although the initial partnership of MCC with

DaimlerChrysler was supposed to provide experience and know how in the whole

production process, the typical synergies given in the industry when whole

platforms are shared by several models or even brands did not take place here.

The SMART platform was designed from scratch and has not been shared across

by any other product. In fact, the SMART forfour launched later on is based on a

Mitsubishi platform. A good example of these synergies we mention here are

exactly what Peugeot, Citroen and Toyota are taking advantage of with their new

A segment models, to be launched in June 2005 (see future substitutes in

Appendix 2).

Future Strategy

In the struggle to make the SMART a profitable venture, the management of the

company has added new models to the SMART line that modify the initial concept of the

car. The tradeoff being faced by managers is to make the SMART more acceptable to

mass markets without diluting the original concept.

In this effort, the Mercedes Group is now promoting a second, larger SMART sedan

(called the ForFour) based on a Mitsubishi platform (Daimler owns t he Japanese

carmaker).

The new model deviate from the initial concept for the following reasons:

1. While the original SMART is only 2.4m long, the ForFour is the size of a

small/medium car. The initial innovative concept of an urban tiny car fades away with

these models

2. Mitsubishi has not been a quality king and the trendy price premium will be hard to

justify

3. The new cars are being released with manual gearbox rather than the complex,

compromised auto/sequential manual cog shifters

We see point one as a major breach of the initial strategy pursued with the original

SMART city coupe (fortwo). Although the For Four can be seen as an attempt to

diversify the product offering, the fact that both cars do not share a platform will increase

development and production costs significantly.

On the diversification front DaimlerChrysler froze plans for a sports utility vehicle to be

launched (SMART SUV) and decided to continue the development of the next generation

of its original 2-seater ForTwo.

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 18

SMART ForMore SMART ForFour

Exhibit 3: Extending the SMART

Line

Launching the SMART in the US has been always considered a possibility to

DaimlerChrysler. Selling the SMART in the US is a challenging venture: it would be

feasible only in a few metropolitan areas as fuel economy and narrow roads are not a

concern in general in the US. In the beginning of February 2005, after revealing that the

SMART division lost 600 million in 2004 (and total losses of 2 billion since launch in

1998) , the Mercedes Group announced that the group was working on a "long-term

business model" for the SMART that includes reviewing possible partnerships. It was

also announced that a restructuring plan should be ready in April

2

.

Did Mercedes Over-reach?

At the conception of the SMART, the core luxury passenger car business of Mercedes

was profitable but the company was facing increasing competition from Japanese luxury

brands, and an overall trend of consolidation in the automotive sector was taking place.

Placing the company on the reach quadrant

3

we can argue that the SMART venture was

a risky proposition since the mini car market was uncharted territory for Mercedes and

required changes to the core capabilities. SMART was not a simple extension of context

for Mercedes. Mercedes tried to mitigate this risk by initially setting up a separate joint

venture (MCC). However, this venture was soon bought out and SMART became a

wholly owned brand of Mercedes.

2

http://www.dw-world.de/dw/article/0,1564,1488809,00.html

3

Rangan and Adner, Profits and the Internet: Seven Misconception, 2001.

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 19

primarily

context

primarily

core

relatively

attractive

relatively

unattractive

The companys

current business

prospects are

The elements of

the business

model that might

change in pursuit

of reach are

MB

primarily

context

primarily

core

relatively

attractive

relatively

unattractive

The companys

current business

prospects are

The elements of

the business

model that might

change in pursuit

of reach are

MB

Exhibit 4: The Market Reach Quadrant

Resource Commitment and Reversibility

The initial resource commitment by MCC was very low given the size and complexity of

the project. A large share of investment was contributed by suppliers backed by strong

supply agreements that guaranteed compensation in case contracts were terminated and in

case production volume agreed upon was not met. MCC also significantly transferred

unfinished goods inventory related costs to suppliers. Except for inexpensive and

standard parts, MCC pays its supplies only when a car is complete with the module built

in.

At the launch of the product a total of 424 million had been invested in developing and

building a factory. MCC invested approximately 228 million, its suppliers and partners

about 197 million. On top of the investment in the factory, MCC invested 358 million

in the development of the car and in machinery and 256 million in establishing a dealer

and distribution organization. Suppliers in machinery and facilities in the proximity of the

Hambach location invested a total of 153 million. Total investment before the launch of

the car reached 1.2 billion.

Initial Investments in the SMARTville and in the launch of the SMART

Amounts in million

Development

and building of

factory

Machinery

and facilities

in the

proximity

Development of

the car

Dealer and

Distribution Total

MCC 228 358 256 841

Suppliers 197 153 350

Total 424 153 358 256 1 191

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 20

We may argue that one of the reasons Daimler accepted the project was the relatively low

commitment from the investment point of view. MCC invested a little bit over 200

million in the SMARTville production plant, slightly more but very close to what the

suppliers did. Additionally, the French government contributed enough to own 25% of

the facilities. It provided funding to the project sponsors expecting to generate 2,000

direct jobs over three years in the region of the city of Hambach. Also, the suppliers took

care of 85% of the working capital needed to keep the assembly line going. This was a

big plus for MCC and Daimler, as the financial burden was much less severe than what a

regular project might have brought for a car manufacturer.

But all those prerogatives did not come without a price: suppliers accepted to take risks

only to a certain point, and MCC was forced to sign compensation clauses by which it

was forced to pay high sums of money to the suppliers if the production expectations

were not met, as it finally happened. All added together meant that another extra

1billion (apart from the 1billion already invested) would be needed by Daimler to exit

the SMART production according to 2000 estimates.

Not only financial, MCC made also political commitments. The project received French

government funding and was considered a public symbol of German-French cooperation.

Shutting the plant and laying off close to 2000 workers from DaimlerChrysler and

suppliers would be politically complicated.

Conclusion

The SMART car ventur e has not been a success. Six years after its launch MCC is still

struggling to reach break-even sales of 200,000 units and is far from reaching its initial

annual sales target of 300,000 units.

In our opinion, the lessons learned from the analysis of the venture are:

It is key to understand what drives the willingness to pay of your target segment

in order to deliver true value to customers. A more complex, sophisticated product

may not necessarily be what your costumer is looking for. Features expected to be

competitive advantage may be only perceived as add-ons to a customer.

Expanding reach is risky. SMART venture was a risky proposition since the mini

car market was uncharted territory for Mercedes and required changes to the core

capabilities. SMART was not a simple extension of context for Mercedes.

Reducing initial commitment by transferring risks to suppliers and governments

usually do not come without a cost. Low initial investments may be attractive at

start but may compromise the reversibility of the project.

Exiting a project and leaving behind huge investments takes a lot of discipline,

but constant discrepancies between expectations and actual sales should be

enough to show a project is not sustainable. Shutting down the project may be a

costly and tough decision, but pushing it even further by widening the offering

may not only deviate from the initial concept but also enlarge the already high

losses.

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 21

REFERENCES

Rangan and Adner, Profits and the Internet: Seven Misconception, 2001.

Trends and drivers of change in the European automotive industry: Mapping report,

European Foundation for the Improvement of Living and Working Conditions, 2004.

Flint J., Backseat Driver Not So SMART, Forbes Magazine, February 2, 2005.

Flint J., Thinking Small, Forbes Magazine, February 3, 2004.

Power, S., The SMART Car Stalls --- DaimlerChrysler Promotes Tiny Car as Next

Big Thing, But Buying Won't Be Easy, The Wall Street Journal, January 11, 2005.

11 January 2005

Kurylko, D., SMART's US debut may be killed; DaimlerChrysler's small-car brand is

a money-loser, Automotive News Europe, January 24, 2005

German-U.S. DaimlerChrysler's SMART Unit Sees No Profit Before 2008, German

News Digest, January 17, 2005

EIU Motor Business Europe, 2

nd

Quarter 1999

EIU Motor Business Europe, 3

rd

Quarter 1999

Promotex online research available at

http://www.promotex.ca/articles/cawthon/2004/2004-01-05_article.html

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 22

Appendix 1 SMART Chronology

01/93: Start of a feasibility study at Mercedes-Benz regarding the development of

a small car

04/03/1994 Press conference: Planned joint venture between Mercedes-Benz and SMH

(today: The Swatch Group Ltd.)

04/1994: Establishment of Micro Compact Car AG, Biel (Switzerland)

12/1994: Location chosen: Hambach in Europle de Sarreguemines (France)

09/1995: SMART concept study at the IAA in Frankfurt (Germany)

14.10.1995: Foundation stone laid in SMARTville

28.11.1995: Foundation of the company Micro Compact Car France in Hambach

(France)

12.06.1997: Inauguration of the SMART engine plant in the (then) Daimler-Benz AG in

Berlin (Germany)

09/1997: World premire of the SMART city-coup at the IAA in Frankfur t

(Germany)

27.10.1997: Inauguration of SMARTville

01.07.1998: Production of the SMART city-coup begins.

10.07.1998: Beginning of advance sales in the SMART Centres

10/1998: Market launch of the SMART city-coup in nine European countries

(Belgium, Germany, France, Italy, Luxembourg, Austria, Switzerland,

Spain and the Netherlands)

01/11/1998 100% take-over of MCC by the (then) Daimler-Benz AG

01/01/1999 Transfer of business activities from Biel (Switzerland) to Renningen

(Germany). Micro Compact Car GmbH renamed Micro Compact Car

SMART GmbH

12/1999: Market launch of the SMART cdi in nine European countries (Belgium,

Germany, France, Italy, Luxembourg, Austria, Switzerland, Spain and the

Netherlands)

12/1999: MCC SMART is the first manufacturer to sell cars via the internet

12/1999: In Hambach, the 100,000th SMART city-coup rolls off the production line

03/2000: Market launch of the SMART cabrio in nine European countries (Belgium,

Germany, France, Italy, Luxembourg, Austria, Switzerland, Spain and the

Netherlands)

09/2000: MCC SMART is the first manufacturer to install internet access in cars,

beginning of internet services at wap.smart.com

03/2001: Market launch of the SMART cabrio cdi

10/2001: Market launch of the SMART city-coup (RHD), SMART cabrio (RHD) in

Great Britain (UK)

11/2001: Market launch of the SMART city-coup (RHD), SMART cabrio (RHD)

and SMART k (RHD) - (japan.: kei-jidousha, "light vehicles") - in Japan

03/2002: Presentation of the SMART crossblade as a production car at the

International Motor Show in Geneva in 2002

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 23

06/2002: Market launch of the SMART crossblade in Belgium, Germany, France,

Great Britain, Italy, Japan, Luxembourg, the Netherlands, Austria, Portugal,

Sweden, Switzerland, Spain, Taiwan, Hungary, the Czech Republic and the

Slovak Republic

09/2002: Micro Compact Car smart GmbH renamed smart GmbH:

09/2002: Establishment of the "SMART mall", the new production line for the

SMART roadster and SMART roadster-coup models in Hambach

10/2002: Fifth anniversary of the plant in Hambach, with a total of 430,000 vehicles

produced since operations commenced

04/2003: Market launch of the SMART roadster, SMART roadster-coup, SMART

city-coup BRABUS and SMART cabrio BRABUS models throughout

Europe

Source: company website

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 24

Appendix 2: Prices and characteristics of substitutes

Parker independent price lists and reviews as of February 2, 2005.

(sources http://www.parkers.co.uk/ http://www.km77.comhttp://elmundomotor.elmundo.es )

Citroen C2: Cheap and really quite funky, 1.1 is a bit breathless and noisy at speed.

Price range: 10,000-12,000

Ford Ka: Stylish, cheap to run, fun to drive, Limited rear accommodation

Price range: 9,000-15,000

Mini One/C. Hatchback: Slick handling, cool image, Poor rear space, pricey,

waiting list

Price range: 15,000-27,000

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 25

SMART fortwo coupe: Teeny-weeny, anyone can park one, Pricey for what it is,

no fun on motorways.

Price range: 10,500-15,000

Daewoo Matiz: Style, space, equipment, cheap, Needs more power on motorways

Price range: 8,500-9,000

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 26

Future substitutes

Peugeot 107, Toyota Aygo and Citron C1: based on the same platform and to be

launched in June 2005

Price range: 7,500

Also, Renault has released in February 2005 a new concept, the Z17. It is just a concept

car which production is not decided yet but if approved, its launch could represent the

closest attempt to do something similar to SMART, while keeping two important

differences:

o It has been shown that cars carry only 1.4 people on average, but two seat interiors

are perceived as a constraint. Z17 is therefore a genuine three-seater complete with

a boot located behind the driver's seat, all built into a compact architecture.

o Although no price estimation is known yet, it would probably try to beat the prices

of cars already in the market or just about to be launched, i.e. less than 7,500.

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 27

Appendix 3: Sales figures for the Mini-car segment

Mini-Car Sales Segment by Model (Western Europe Market:1995-1998)

Manufacturer Model 1995 % 1996 % 1997 % 1998 %

Ford Ka

- 0.0%

25,194 4.3%

202,337 22.9%

266,137 25.8%

Renault Twingo

227,944 40.6%

214,063 36.3%

208,533 23.6%

199,148 19.3%

Lancia Ypsilon

59,187 10.5%

80,907 13.7%

135,571 15.3%

145,507 14.1%

Fiat Panda

66,750 11.9%

63,901 10.8%

126,861 14.3%

130,943 12.7%

Fiat Seicento

- 0.0%

- 0.0% 0.0%

82,166 8.0%

Fiat Cinquecento

146,535 26.1%

145,408 24.6%

154,265 17.4%

77,316 7.5%

Seat Arosa

- 0.0%

- 0.0%

- 0.0%

46,375 4.5%

Daewoo Matiz

- 0.0%

- 0.0%

- 0.0%

23,186 2.2%

MCC SMART

- 0.0%

- 0.0%

52 0.0%

20,000 1.9%

Suzuki Alto

16,020 2.9%

16,020 2.7%

20,330 2.3%

16,908 1.6%

Daihatsu Cuore

7,541 1.3%

7,541 1.3%

7,511 0.8%

9,281 0.9%

Rover Mini

9,980 1.8%

9,980 1.7%

6,486 0.7%

7,517 0.7%

Seat Marbella

22,426 4.0%

22,426 3.8%

18,021 2.0%

5,204 0.5%

Subaru Vivio

2,684 0.5%

2,684 0.5%

2,993 0.3%

1,752 0.2%

Hyundai Atoz

- 0.0%

- 0.0%

- 0.0% n.a. -

Total

561,062 100.0%

590,120 100.0%

884,957 100.0%

1,033,438 100.0%

Source: EIU Motor Business Europe, 2

nd

Quarter 1999

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 28

Appendix 4: Passenger Car Production in Western

Europe by Segment

Segment Brands units % units %

A Ford Ka 629,384 4.3% 772,054 5.3%

B Peugeot 206 3,743,542 25.6% 3,569,852 24.4%

C VW Golf 4,424,434 30.3% 4,409,949 30.2%

D Ford Mondeo 3,289,172 22.5% 3,097,645 21.2%

E VW Passat 1,385,577 9.5% 1,590,017 10.9%

F MB S-Class 153,771 1.1% 141,353 1.0%

G Jaguar XJS 199,887 1.4% 172,368 1.2%

LCV VW Caravan 181,728 1.2% 192,833 1.3%

MPV Chrysler Minivan 348,849 2.4% 320,165 2.2%

SUV Ford Explorer 258,925 1.8% 354,868 2.4%

Total 14,615,269 100% 14,621,104 100%

1998 2004

Source: Motor Business International 3

rd

Quarter 1999.

SMART Main Project Group 4, Section A

Innovation Strategy and Entrepreneurship 29

Appendix 5: Mobility Offerings and Partnerships

Accor Hotels

The Accor Hotel Group with Sofitel, Novotel and Mercure hotels, provide attractive

and comfortable hotels. smart drivers benefit from special smart rates in selected hotels

worldwide.

APCOA Autoparking GmbH/VUP GmbH

APCOA has provided the first 3m parking spaces for smart fortwo coup/cabrio drivers

in Germany and Austria. VUP GmbH, which operates in Germany, is also doing the

same. This ensures that not only can smart fortwo coup/cabrio drivers find a parking

space more easily, they can often benefit from special smart prices too.

AVIS Europe

Avis has the largest rental car service network in Europe. smart drivers can rent cars at

favourable rates in all western European countries and in many other countries too.

Deutsche Bahn AG

DB AutoZug will transport your smart fortwo coup/cabrio to around 18 interesting

destinations at home and abroad. smart fortwo coup/cabrio customers are entitled to

special smart rates.

DFDS Seaways, Hoverspeed, Color Line, Scandlines, SeaFrance, Bodensee-

Schiffsbetriebe GmbH, Schweizerische Bodensee-Schiffahrtsgesellschaft AG.

The road sometimes comes to an end at a large expanse of water - then the ferry is the

only means of transport available. But this can be a real pleasure - some smartmove

ferries cross attractive routes on the Baltic Sea and the North Sea, Lake Constance and

Lake Zurich. And you can take your smart at special rates.

Bundesverband CarSharing (bcs)

bcs provides all classes of vehicles in more than 200 German towns and cities in

accordance with the principle of car sharing. smart drivers are offered free membership

for the first year.

Conoco Jet, Shell, Migrol, BP, COVA, Wash One

In some European countries smart fortwo coups are that little bit cleaner than in other

places. This is because of the smartmove Wash partners, Conoco Jet, Shell, Migrol,

BP, COVA, Wash One who offer reduced rates for washing a smart fortwo coup.

RailLink AG

Together with RailLink AG and Swiss Railways (SBB), smart completes the mobility

chain at railway stations. RailLink members can use a smart fortwo coup at all larger

stations in Switzerland, and they have access to the Mobility CarSharing fleet at many

further locations.

CineMaxX AG

With 49 central cinema centres, CinemaxX AG is the market leader in Germany. The

CinemaxXCard offers cinema fans discounts and special offers for cinema tickets and

related products and services. smart drivers can buy this card at a special price.

Source: company website

You might also like

- Situational Analysis: 3.1 Detailed Company Analysis (600 Words)No ratings yetSituational Analysis: 3.1 Detailed Company Analysis (600 Words)17 pages

- The New Peasantries Struggles For Autonomy and Sustainability in An Era of Empire and Globalization100% (1)The New Peasantries Struggles For Autonomy and Sustainability in An Era of Empire and Globalization385 pages

- Design A Marketing Plan To Launch A Small CarNo ratings yetDesign A Marketing Plan To Launch A Small Car19 pages

- Management Information System in Maruti Suzuki India LTD: Corporate ProfileNo ratings yetManagement Information System in Maruti Suzuki India LTD: Corporate Profile19 pages

- Operations Management: The Input/output Transformation ModelNo ratings yetOperations Management: The Input/output Transformation Model2 pages

- 3417 Class 5 International Expansion Strategy100% (2)3417 Class 5 International Expansion Strategy33 pages

- Business Strategy Module: Oxford Brookes University - International Business School - BudapestNo ratings yetBusiness Strategy Module: Oxford Brookes University - International Business School - Budapest8 pages

- A+ Athletics Final Presentation 11.28.11No ratings yetA+ Athletics Final Presentation 11.28.1158 pages

- How TITAN Watches Changed Consumers Perception About Wrist WatchesNo ratings yetHow TITAN Watches Changed Consumers Perception About Wrist Watches16 pages

- Factors Affecting The Automotive Industry (PEST Analysis)No ratings yetFactors Affecting The Automotive Industry (PEST Analysis)10 pages

- Accenture ATIOS Publication Natural Rubber Trading Markets100% (1)Accenture ATIOS Publication Natural Rubber Trading Markets36 pages

- Franz Collections - Marketing FM2 - Rajinda He - One Pager100% (1)Franz Collections - Marketing FM2 - Rajinda He - One Pager2 pages

- Competitive Analysis: Porter's Five-Forces Model: Rivalry Among Competing FirmsNo ratings yetCompetitive Analysis: Porter's Five-Forces Model: Rivalry Among Competing Firms3 pages

- About This Document: Adidas Group Sustainability Intro 1No ratings yetAbout This Document: Adidas Group Sustainability Intro 161 pages

- Visualizing Marketing: From Abstract To IntuitiveNo ratings yetVisualizing Marketing: From Abstract To Intuitive306 pages

- Marketing and Performance Objective and Polar DiagramNo ratings yetMarketing and Performance Objective and Polar Diagram17 pages

- Global Project Marketing Assignment 2: Samsung ElectronicsNo ratings yetGlobal Project Marketing Assignment 2: Samsung Electronics11 pages

- COVID-19 A Guide to Self Preparedness for Crisis Management: 1, #2From EverandCOVID-19 A Guide to Self Preparedness for Crisis Management: 1, #25/5 (1)

- Study of Securing Required Ventilation Rates For Underground Parking LotsNo ratings yetStudy of Securing Required Ventilation Rates For Underground Parking Lots7 pages

- Indoor Air Environment of A Shopping Centre Carpark CFD Ventilation StudyNo ratings yetIndoor Air Environment of A Shopping Centre Carpark CFD Ventilation Study11 pages

- Monitoring and Simulation of Mechanically Ventilated Underground Car ParksNo ratings yetMonitoring and Simulation of Mechanically Ventilated Underground Car Parks8 pages

- Smoke Clearance in An Underground Car Park Using The Jet Fan SystemNo ratings yetSmoke Clearance in An Underground Car Park Using The Jet Fan System7 pages

- Mozart - KV550 Symphony No40 Pno Arr August HornNo ratings yetMozart - KV550 Symphony No40 Pno Arr August Horn22 pages

- Factors Affecting The Women Entrepreneurship Development in BangladeshNo ratings yetFactors Affecting The Women Entrepreneurship Development in Bangladesh7 pages

- Entrepreneurship Compensation CorporationNo ratings yetEntrepreneurship Compensation Corporation16 pages

- The Entrepreneurial Mind: (Bad Newz BBQ)No ratings yetThe Entrepreneurial Mind: (Bad Newz BBQ)4 pages

- Introduction To Entrepreneurship: Bruce R. Barringer R. Duane IrelandNo ratings yetIntroduction To Entrepreneurship: Bruce R. Barringer R. Duane Ireland27 pages

- Issues and Challenges For Women Entrepreneurs in Global SceneNo ratings yetIssues and Challenges For Women Entrepreneurs in Global Scene7 pages

- Sad State of Cyber Politics (Cato Policy Report)No ratings yetSad State of Cyber Politics (Cato Policy Report)4 pages

- Group2 Sterling Final-Research-ManuscriptNo ratings yetGroup2 Sterling Final-Research-Manuscript113 pages

- Entrepreneurship and Small Business Management Unit 4No ratings yetEntrepreneurship and Small Business Management Unit 422 pages

- omran-yousafzai-2023-epistemic-injustice-and-epistemic-resistance-an-intersectional-study-of-women-s-entrepreneurshipNo ratings yetomran-yousafzai-2023-epistemic-injustice-and-epistemic-resistance-an-intersectional-study-of-women-s-entrepreneurship28 pages

- Module-5 TECHNOLOGICAL INNOVATION AND MANAGEMENT ENTREPRENEURSHIPNo ratings yetModule-5 TECHNOLOGICAL INNOVATION AND MANAGEMENT ENTREPRENEURSHIP79 pages

- Analysis of Maize Value Addition Among Entrepreneurs in Taraba State, NigeriaNo ratings yetAnalysis of Maize Value Addition Among Entrepreneurs in Taraba State, Nigeria9 pages

- Theme 3 Innovation, Strategy and Project ManagementNo ratings yetTheme 3 Innovation, Strategy and Project Management95 pages

- The Role of Multipurpose Cooperatives in Social and Economic Empowerment, Gambella Town, Ethiopia100% (1)The Role of Multipurpose Cooperatives in Social and Economic Empowerment, Gambella Town, Ethiopia80 pages

- Mastercard Foundation Scholars Program Scholar Entrepreneurship FundNo ratings yetMastercard Foundation Scholars Program Scholar Entrepreneurship Fund3 pages

- Role of Smes in Economic Development of India: Dr.P.UmaNo ratings yetRole of Smes in Economic Development of India: Dr.P.Uma7 pages

- Situational Analysis: 3.1 Detailed Company Analysis (600 Words)Situational Analysis: 3.1 Detailed Company Analysis (600 Words)

- The New Peasantries Struggles For Autonomy and Sustainability in An Era of Empire and GlobalizationThe New Peasantries Struggles For Autonomy and Sustainability in An Era of Empire and Globalization

- Management Information System in Maruti Suzuki India LTD: Corporate ProfileManagement Information System in Maruti Suzuki India LTD: Corporate Profile

- Operations Management: The Input/output Transformation ModelOperations Management: The Input/output Transformation Model

- Business Strategy Module: Oxford Brookes University - International Business School - BudapestBusiness Strategy Module: Oxford Brookes University - International Business School - Budapest

- How TITAN Watches Changed Consumers Perception About Wrist WatchesHow TITAN Watches Changed Consumers Perception About Wrist Watches

- Factors Affecting The Automotive Industry (PEST Analysis)Factors Affecting The Automotive Industry (PEST Analysis)

- Accenture ATIOS Publication Natural Rubber Trading MarketsAccenture ATIOS Publication Natural Rubber Trading Markets

- Franz Collections - Marketing FM2 - Rajinda He - One PagerFranz Collections - Marketing FM2 - Rajinda He - One Pager

- Competitive Analysis: Porter's Five-Forces Model: Rivalry Among Competing FirmsCompetitive Analysis: Porter's Five-Forces Model: Rivalry Among Competing Firms

- About This Document: Adidas Group Sustainability Intro 1About This Document: Adidas Group Sustainability Intro 1

- Marketing and Performance Objective and Polar DiagramMarketing and Performance Objective and Polar Diagram

- Global Project Marketing Assignment 2: Samsung ElectronicsGlobal Project Marketing Assignment 2: Samsung Electronics

- COVID-19 A Guide to Self Preparedness for Crisis Management: 1, #2From EverandCOVID-19 A Guide to Self Preparedness for Crisis Management: 1, #2

- Study of Securing Required Ventilation Rates For Underground Parking LotsStudy of Securing Required Ventilation Rates For Underground Parking Lots

- Indoor Air Environment of A Shopping Centre Carpark CFD Ventilation StudyIndoor Air Environment of A Shopping Centre Carpark CFD Ventilation Study

- Monitoring and Simulation of Mechanically Ventilated Underground Car ParksMonitoring and Simulation of Mechanically Ventilated Underground Car Parks

- Smoke Clearance in An Underground Car Park Using The Jet Fan SystemSmoke Clearance in An Underground Car Park Using The Jet Fan System

- Factors Affecting The Women Entrepreneurship Development in BangladeshFactors Affecting The Women Entrepreneurship Development in Bangladesh

- Introduction To Entrepreneurship: Bruce R. Barringer R. Duane IrelandIntroduction To Entrepreneurship: Bruce R. Barringer R. Duane Ireland

- Issues and Challenges For Women Entrepreneurs in Global SceneIssues and Challenges For Women Entrepreneurs in Global Scene

- Entrepreneurship and Small Business Management Unit 4Entrepreneurship and Small Business Management Unit 4

- omran-yousafzai-2023-epistemic-injustice-and-epistemic-resistance-an-intersectional-study-of-women-s-entrepreneurshipomran-yousafzai-2023-epistemic-injustice-and-epistemic-resistance-an-intersectional-study-of-women-s-entrepreneurship

- Module-5 TECHNOLOGICAL INNOVATION AND MANAGEMENT ENTREPRENEURSHIPModule-5 TECHNOLOGICAL INNOVATION AND MANAGEMENT ENTREPRENEURSHIP

- Analysis of Maize Value Addition Among Entrepreneurs in Taraba State, NigeriaAnalysis of Maize Value Addition Among Entrepreneurs in Taraba State, Nigeria

- Theme 3 Innovation, Strategy and Project ManagementTheme 3 Innovation, Strategy and Project Management

- The Role of Multipurpose Cooperatives in Social and Economic Empowerment, Gambella Town, EthiopiaThe Role of Multipurpose Cooperatives in Social and Economic Empowerment, Gambella Town, Ethiopia

- Mastercard Foundation Scholars Program Scholar Entrepreneurship FundMastercard Foundation Scholars Program Scholar Entrepreneurship Fund

- Role of Smes in Economic Development of India: Dr.P.UmaRole of Smes in Economic Development of India: Dr.P.Uma