4-35 Model Problem

4-35 Model Problem

Download as xlsx, pdf, or txt

You might also like

- Polimeni and An (2024) SSRNDocument48 pagesPolimeni and An (2024) SSRNWSB-TVNo ratings yet

- Solutions Ch04 P35 Build A ModelDocument13 pagesSolutions Ch04 P35 Build A Modelbusinessdoctor23100% (4)

- CF 13th Edition Chapter 08 Excel Master-1Document14 pagesCF 13th Edition Chapter 08 Excel Master-1Stephen CelestineNo ratings yet

- Advanced Technical Analysis A Guide To High Probability Trading by Aligning With Smart MoneyDocument113 pagesAdvanced Technical Analysis A Guide To High Probability Trading by Aligning With Smart MoneyShaowalit Gamter100% (4)

- Ch03 P15 Build A ModelDocument2 pagesCh03 P15 Build A Model03020380% (1)

- Chapter 13. Tool Kit For Corporate Valuation, Value-Based Management and Corporate GovernanceDocument19 pagesChapter 13. Tool Kit For Corporate Valuation, Value-Based Management and Corporate GovernanceHenry RizqyNo ratings yet

- Core Chapter 09 Excel Master 4th Edition StudentDocument77 pagesCore Chapter 09 Excel Master 4th Edition StudentShaunak ChitnisNo ratings yet

- Chapter 5. Ch05 P24 Build A ModelDocument5 pagesChapter 5. Ch05 P24 Build A ModelMatúš GašparovičNo ratings yet

- Ch02 P20 Build A Model SolutionDocument6 pagesCh02 P20 Build A Model Solutionsonam agrawalNo ratings yet

- Ch06 Tool KitDocument36 pagesCh06 Tool KitRoy HemenwayNo ratings yet

- Chapter 13. CH 13-11 Build A Model: (Par Plus PIC)Document7 pagesChapter 13. CH 13-11 Build A Model: (Par Plus PIC)AmmarNo ratings yet

- Chap 009Document68 pagesChap 009Mnar Abu-ShliebaNo ratings yet

- Ch04 Tool KitDocument80 pagesCh04 Tool KitAdamNo ratings yet

- Ch13 29Document3 pagesCh13 29Önder GiderNo ratings yet

- PDF PDFDocument7 pagesPDF PDFMikey MadRatNo ratings yet

- Week 3 SolutionDocument5 pagesWeek 3 SolutionI190006 Taimoor JanNo ratings yet

- SP500 Historical Monthly Total ReturnsDocument26 pagesSP500 Historical Monthly Total ReturnsQasim MughalNo ratings yet

- Chapter 4 - Build A Model SpreadsheetDocument9 pagesChapter 4 - Build A Model SpreadsheetSerge Olivier Atchu Yudom100% (1)

- Ch04 P35 Build A ModelDocument17 pagesCh04 P35 Build A ModelAbhishek Surana100% (2)

- F Wall Street 4-MSFT-Analysis (2010) 20100817Document1 pageF Wall Street 4-MSFT-Analysis (2010) 20100817smith_raNo ratings yet

- A13 - Job Order - GJM TailoringDocument13 pagesA13 - Job Order - GJM TailoringTee MendozaNo ratings yet

- IfDocument14 pagesIfĐặng Thuỳ HươngNo ratings yet

- A Mayor's Office 1Document34 pagesA Mayor's Office 1Mary Jane Katipunan CalumbaNo ratings yet

- Chapter 8Document78 pagesChapter 8Faisal SiddiquiNo ratings yet

- Expenses: BalancesDocument8 pagesExpenses: BalancesBrookeNo ratings yet

- Tutorial 3 AnswerDocument3 pagesTutorial 3 AnswerSyuhaidah Binti Aziz ZudinNo ratings yet

- Core Chapter 04 Excel Master 4th Edition StudentDocument150 pagesCore Chapter 04 Excel Master 4th Edition StudentDarryl WallaceNo ratings yet

- Basics of Financial Statement Analysis Tools of AnalysisDocument30 pagesBasics of Financial Statement Analysis Tools of AnalysisNurul MuslimahNo ratings yet

- New Assessment SchemeDocument6 pagesNew Assessment SchemeaakashkagarwalNo ratings yet

- Ch05 P24 Build A ModelDocument6 pagesCh05 P24 Build A ModelРоман УдовичкоNo ratings yet

- Inspection Form HDEC 2Document36 pagesInspection Form HDEC 2UD. Gunung JatiNo ratings yet

- Excel Project Timesheet FullDocument4 pagesExcel Project Timesheet Fullprateekchopra1No ratings yet

- CF 11th Edition Chapter 03 Excel Master StudentDocument48 pagesCF 11th Edition Chapter 03 Excel Master StudentAdrian GonzagaNo ratings yet

- La Tabla Del Ahorro: Monto Financiado: Interés Efectivo MensualDocument21 pagesLa Tabla Del Ahorro: Monto Financiado: Interés Efectivo MensualIvan Forero TorresNo ratings yet

- Assessment SchemesDocument8 pagesAssessment SchemesaakashkagarwalNo ratings yet

- FINA Chapter 6 HWDocument7 pagesFINA Chapter 6 HWBrandonNo ratings yet

- In These Spreadsheets, You Will Learn How To Use The Following Excel FunctionsDocument78 pagesIn These Spreadsheets, You Will Learn How To Use The Following Excel FunctionsFaisal SiddiquiNo ratings yet

- La Tabla Del Ahorro: Total Gastos Mensuales Monto Financiado: Interés Efectivo MensualDocument21 pagesLa Tabla Del Ahorro: Total Gastos Mensuales Monto Financiado: Interés Efectivo Mensualrociobal03No ratings yet

- 12 Month Cash Flow Statement Template Camino FinancialDocument6 pages12 Month Cash Flow Statement Template Camino Financialsandra istalla caceresNo ratings yet

- 2019-057-JSA-Loading Unloading Near Access RoadDocument8 pages2019-057-JSA-Loading Unloading Near Access RoadUD. Gunung JatiNo ratings yet

- Mgac CustomDocument123 pagesMgac CustomJoana TrinidadNo ratings yet

- SBICAPS - Model Test 2Document34 pagesSBICAPS - Model Test 2rishav digga0% (1)

- Chapter10 StudentworksheetDocument45 pagesChapter10 StudentworksheetMohitNo ratings yet

- Income Statement Horizontal Analysis TemplateDocument2 pagesIncome Statement Horizontal Analysis TemplateSope DalleyNo ratings yet

- CH 14Document27 pagesCH 14ReneeNo ratings yet

- Chapter 9 Case Question FinanceDocument3 pagesChapter 9 Case Question FinanceBhargavNo ratings yet

- Chapter (4) TVMDocument5 pagesChapter (4) TVMMohamed DiabNo ratings yet

- Chapter 12Document17 pagesChapter 12Faisal SiddiquiNo ratings yet

- Tax CalculaterDocument2 pagesTax CalculaterMahimaNo ratings yet

- Capitalization: Capital Vs Operating LeaseDocument2 pagesCapitalization: Capital Vs Operating Leasejohnsmith12312312312No ratings yet

- Amazon Accounting Ver 0.1Document148 pagesAmazon Accounting Ver 0.1Lalit mohan PradhanNo ratings yet

- Ch25 Tool KitDocument35 pagesCh25 Tool KitJITIN ARORANo ratings yet

- How To Calculate Terminal ValueDocument4 pagesHow To Calculate Terminal ValueSODDEYNo ratings yet

- Ch05 Mini CaseDocument8 pagesCh05 Mini CaseSehar Salman AdilNo ratings yet

- Accounting Formulas DoneDocument27 pagesAccounting Formulas DoneRikuh RiyastantoNo ratings yet

- Break Even Point in Unit Sales Dollar SalesDocument27 pagesBreak Even Point in Unit Sales Dollar SalesdrgNo ratings yet

- SML 9179 SML 21531 SML: Daily Daily WeeklyDocument3 pagesSML 9179 SML 21531 SML: Daily Daily WeeklysamNo ratings yet

- Asignacion Unidad 2Document6 pagesAsignacion Unidad 2Angel L Rolon TorresNo ratings yet

- IFM PresentsiDocument4 pagesIFM PresentsiRezky Pratama Putra0% (1)

- Dividend Discount Model - Stable GrowthDocument7 pagesDividend Discount Model - Stable GrowthArie NervouzNo ratings yet

- Case StudyDocument6 pagesCase StudyArun Kenneth100% (1)

- CH 4 4-35 SpreadsheetDocument34 pagesCH 4 4-35 Spreadsheetcherishwisdom_997598No ratings yet

- CH 02 P 35 Build A Model 11/24/2006Document7 pagesCH 02 P 35 Build A Model 11/24/2006sqlserver200800No ratings yet

- Institute For Excellence in Higher Education (IEHE), Bhopal: TitleDocument1 pageInstitute For Excellence in Higher Education (IEHE), Bhopal: TitleDevanshu VermaNo ratings yet

- Final AccountsDocument9 pagesFinal AccountsRositaNo ratings yet

- 05 Wms Green Fields RenaissanceDocument5 pages05 Wms Green Fields RenaissanceAllan DouglasNo ratings yet

- The Great Depression - Real ReasonsDocument148 pagesThe Great Depression - Real Reasonsarchuganapathy8409No ratings yet

- FranchisingDocument5 pagesFranchisingDonita RossNo ratings yet

- TAX267 - OBE Lesson Plan Oct2023 - Feb2024Document11 pagesTAX267 - OBE Lesson Plan Oct2023 - Feb2024NUR ATHIRAH ZAINONNo ratings yet

- Credtrans Rem CDocument8 pagesCredtrans Rem CKarina Bette Ruiz100% (1)

- Final PPT of Income From House PropertyDocument33 pagesFinal PPT of Income From House PropertyAzhar Ali100% (1)

- Ever Blue Equity SDN BHD (202201007684)Document6 pagesEver Blue Equity SDN BHD (202201007684)INFINITY GROUPNo ratings yet

- Tugas 12 Dividend and Retained EarningsDocument4 pagesTugas 12 Dividend and Retained EarningsLenrik AbcNo ratings yet

- Travel & Cash Advance Request: TCAR DetailDocument2 pagesTravel & Cash Advance Request: TCAR Detailhendri sulistiawanNo ratings yet

- Introduction 1Document3 pagesIntroduction 1HDNo ratings yet

- MBA Business Sustainablity - 2011Document2 pagesMBA Business Sustainablity - 2011Santhosh KrishnanNo ratings yet

- Example Business Profit and Economic ProfitDocument2 pagesExample Business Profit and Economic Profitmaria isabellaNo ratings yet

- South Korea Accounting StandardsDocument2 pagesSouth Korea Accounting StandardsAaron Joy Dominguez PutianNo ratings yet

- Doa FreshDocument25 pagesDoa FreshDinesh KumarNo ratings yet

- ACCOUNTING IDENTITY-means That TheDocument23 pagesACCOUNTING IDENTITY-means That TheHel LoNo ratings yet

- Case Study On Joint Stock CompayDocument2 pagesCase Study On Joint Stock CompayShichin SenanNo ratings yet

- Sps Antonio Tibay Vs CA GR 119655Document11 pagesSps Antonio Tibay Vs CA GR 119655VieNo ratings yet

- Mathematics of FinanceDocument18 pagesMathematics of FinanceKennet CruzNo ratings yet

- Supplements CMSLJune2024NewSyllabus06032024Document31 pagesSupplements CMSLJune2024NewSyllabus06032024vaishnavimohanta7No ratings yet

- Trading Using The Moving AveragesDocument8 pagesTrading Using The Moving AveragesRichard NdahaniNo ratings yet

- Corporation 2Document48 pagesCorporation 2Fria maeNo ratings yet

- Lesson 4.1 GAAP Acctg ConceptsDocument19 pagesLesson 4.1 GAAP Acctg ConceptsSamantha CabugonNo ratings yet

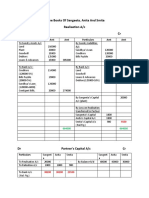

- In The Books of Sangeeta, Anita and Smita Realisation A/c DR CRDocument2 pagesIn The Books of Sangeeta, Anita and Smita Realisation A/c DR CRHarendra PrajapatiNo ratings yet

- Fundamental Equity Analysis - SPI Index - The Top 100 Companies of The Swiss Performance IndexDocument205 pagesFundamental Equity Analysis - SPI Index - The Top 100 Companies of The Swiss Performance IndexQ.M.S Advisors LLCNo ratings yet

- Certificate PDFDocument2 pagesCertificate PDFDurgesh RaghuvanshiNo ratings yet