Income Tax in Australia

Income Tax in Australia

Download as pdf or txt

You might also like

- Bilant Lb. Engleza ModelDocument5 pagesBilant Lb. Engleza ModelklarckkentNo ratings yet

- Unswl036 297x210 Law Juris Doctor Guide 2018 Web SpreadDocument23 pagesUnswl036 297x210 Law Juris Doctor Guide 2018 Web SpreadblairzhangNo ratings yet

- The Compliance Guide To Financial PromotionsDocument10 pagesThe Compliance Guide To Financial PromotionsWH100% (1)

- The A To Z of Employment PracticeDocument714 pagesThe A To Z of Employment PracticengamoloNo ratings yet

- The Exponential Law FirmDocument9 pagesThe Exponential Law FirmRyan McCleadNo ratings yet

- Taxation Chapter 5 - 8Document117 pagesTaxation Chapter 5 - 8Hồng Hạnh NguyễnNo ratings yet

- Taxation in AustraliaDocument1,181 pagesTaxation in AustraliaTimore Francis0% (1)

- Company Law TextbookDocument921 pagesCompany Law Textbookzacharyswartz26No ratings yet

- Sage Pastel Accounting Payroll and HR Tax Guide For 2013/2014Document52 pagesSage Pastel Accounting Payroll and HR Tax Guide For 2013/2014Patty PetersonNo ratings yet

- Property Studies Postgrad Real Estate June 2016Document20 pagesProperty Studies Postgrad Real Estate June 2016takuva03No ratings yet

- MAC2602 001 2018 4 B PDFDocument248 pagesMAC2602 001 2018 4 B PDFVusi Mazibuko0% (1)

- PastelDocument56 pagesPastelCindy Macpherson0% (1)

- Ipaper For Book NID#41987Document443 pagesIpaper For Book NID#41987bfelix100% (1)

- LU19 - Tax Administration ActDocument25 pagesLU19 - Tax Administration ActVincent Mutumwa8oo9wooNo ratings yet

- Tax Policy ConceptsDocument17 pagesTax Policy Conceptseriazalikiharata100% (1)

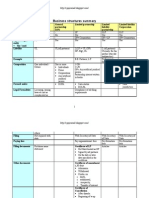

- Business Structures SummaryDocument5 pagesBusiness Structures SummaryMrudula V.100% (2)

- Tax Administration 2021 OecdDocument355 pagesTax Administration 2021 OecdscorpioboyNo ratings yet

- Corporate Governance PresentationDocument146 pagesCorporate Governance PresentationCompliance CRG100% (1)

- 2012 Financial Services Fact BookDocument259 pages2012 Financial Services Fact BookThe Partnership for a Secure Financial Future100% (3)

- SA Income Tax Guide - UnknownDocument723 pagesSA Income Tax Guide - UnknownElias KehayiasNo ratings yet

- 2011 Sydney Law School Postgraduate GuideDocument144 pages2011 Sydney Law School Postgraduate GuideShamir GuptaNo ratings yet

- Companies Act 71 of 2008Document197 pagesCompanies Act 71 of 2008whkhumalo100% (1)

- Internet Entrepreneurship Survival GuideDocument29 pagesInternet Entrepreneurship Survival GuideboyhermesNo ratings yet

- CV Review Top CVDocument4 pagesCV Review Top CVIlyas HabibiNo ratings yet

- Beginners Guide To Power BiDocument80 pagesBeginners Guide To Power BishailenderojhaNo ratings yet

- Canadian Investment Tax BookletDocument29 pagesCanadian Investment Tax BookletNeel Roberts100% (2)

- Sources of Law in Australia Lecture Slides - Revised On February 24Document23 pagesSources of Law in Australia Lecture Slides - Revised On February 24尹米勒No ratings yet

- What Next?: Making Smarter Career ChoicesDocument0 pagesWhat Next?: Making Smarter Career Choicesmoisescu.raduNo ratings yet

- Understanding Investments Theories and StrategiesDocument76 pagesUnderstanding Investments Theories and StrategiesFinancial WisdomNo ratings yet

- WW Corporate Tax Guide 2005Document1,108 pagesWW Corporate Tax Guide 2005LFNo ratings yet

- Canadian Personal Tax ChecklistDocument4 pagesCanadian Personal Tax ChecklistNeel RobertsNo ratings yet

- Guide To Save Tax in UKDocument8 pagesGuide To Save Tax in UKCyrus KhanNo ratings yet

- Accounting For Non AccountantsDocument66 pagesAccounting For Non Accountantsআম্লান দত্ত100% (2)

- Careers in Financial Markets 2010-2011 PDFDocument100 pagesCareers in Financial Markets 2010-2011 PDFtrop41No ratings yet

- Personal Exemptions: UK: Income Tax ExemptionsDocument4 pagesPersonal Exemptions: UK: Income Tax ExemptionsLuiza ŢîmbaliucNo ratings yet

- Elements of Corporate TaxationDocument4 pagesElements of Corporate Taxationreggie1010No ratings yet

- Ncome Tax: Business StructuresDocument51 pagesNcome Tax: Business StructuresGab VillahermosaNo ratings yet

- Running Head: INCOME TAXDocument9 pagesRunning Head: INCOME TAXKashif MalikNo ratings yet

- CTP 3 UnitsDocument53 pagesCTP 3 Unitsjdivyadharshini131202No ratings yet

- Estate Tax After The Fiscal Cliff: Collaborative Financial Solutions, LLCDocument4 pagesEstate Tax After The Fiscal Cliff: Collaborative Financial Solutions, LLCJanet BarrNo ratings yet

- Name: Course: Prepared By: Dr. Jessie N. DiazDocument11 pagesName: Course: Prepared By: Dr. Jessie N. DiazPrince Isaiah JacobNo ratings yet

- TaxationDocument2 pagesTaxationIanNo ratings yet

- Income Taxation in The PhilippinesDocument4 pagesIncome Taxation in The PhilippinesjenxxacadsNo ratings yet

- Corporate Income Taxes and Tax RatesDocument38 pagesCorporate Income Taxes and Tax RatesShaheen ShahNo ratings yet

- X 70 15 PDFDocument32 pagesX 70 15 PDFkunalwarwickNo ratings yet

- Withholding TaxDocument4 pagesWithholding TaxTudor KingNo ratings yet

- What Is IncomeDocument6 pagesWhat Is Incomejustine joi WrightNo ratings yet

- Summary of Thailand-Tax-Guide and LawsDocument34 pagesSummary of Thailand-Tax-Guide and LawsPranav BhatNo ratings yet

- Unit 2Document5 pagesUnit 2piyush.birru25No ratings yet

- Unit 1Document5 pagesUnit 1piyush.birru25No ratings yet

- Tax System: BY Arpita Pali Prachi Jaiswal Mansi MahaleDocument30 pagesTax System: BY Arpita Pali Prachi Jaiswal Mansi MahaleSiddharth SharmaNo ratings yet

- Module 4 - Income TaxationDocument6 pagesModule 4 - Income TaxationLumbay, Jolly MaeNo ratings yet

- Vaishnavi ProjectDocument72 pagesVaishnavi ProjectAkshada DhapareNo ratings yet

- What Type of Information Is Necessary To Complete A Tax ReturnDocument4 pagesWhat Type of Information Is Necessary To Complete A Tax ReturnDianna RabadonNo ratings yet

- DocumentDocument1 pageDocumentjoeyrosario817No ratings yet

- Lecture 1 - Introduction To Income TaxDocument27 pagesLecture 1 - Introduction To Income TaxMimi kupiNo ratings yet

- module 1 Overview of Income tax lawDocument10 pagesmodule 1 Overview of Income tax lawsabirmessi1019No ratings yet

- CHAPTERDocument20 pagesCHAPTERsanchitNo ratings yet

- Presentation1 TaxDocument27 pagesPresentation1 Taxzerubabel abebeNo ratings yet

- International Tax EnvironmentDocument14 pagesInternational Tax EnvironmentAnonymous VstguMKrb50% (2)

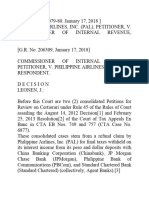

- G.R. Nos. 206079-80Document63 pagesG.R. Nos. 206079-80Jericho CapitoNo ratings yet

- This Study Resource Was: Lecture Handout For Chapter 12Document6 pagesThis Study Resource Was: Lecture Handout For Chapter 12rifa hanaNo ratings yet

- OD119393245620383000Document1 pageOD119393245620383000cpkaseraNo ratings yet

- Income From Capital GainDocument13 pagesIncome From Capital GainDeepak Patil100% (1)

- Instant Download Payroll Accounting 2019 29th Edition Bernard J. Bieg PDF All ChapterDocument84 pagesInstant Download Payroll Accounting 2019 29th Edition Bernard J. Bieg PDF All Chapterzhorekissou70100% (1)

- Lease Contract Against CODDocument2 pagesLease Contract Against CODAntonieto BNo ratings yet

- ch2 Version1-2Document59 pagesch2 Version1-2yea okayNo ratings yet

- Tax Ch02Document10 pagesTax Ch02GabriellaNo ratings yet

- IndividualDocument14 pagesIndividualKenneth Bryan Tegerero TegioNo ratings yet

- 10 Personal Financial Plan Template-1Document2 pages10 Personal Financial Plan Template-1Emirish PNo ratings yet

- PremiumPaidStatement 2022-2023 LicDocument1 pagePremiumPaidStatement 2022-2023 LicHemant BhoriaNo ratings yet

- Destruction FormDocument2 pagesDestruction FormHanabishi RekkaNo ratings yet

- Goods and Services Tax: Introduction To Excel Based Template For Data Upload in Java Offline ToolDocument28 pagesGoods and Services Tax: Introduction To Excel Based Template For Data Upload in Java Offline ToolBharath NaniNo ratings yet

- Fesco Online BillDocument2 pagesFesco Online BillWaqar AkramNo ratings yet

- Power Bank of Empire City 15th PAYROLL: For The Period ofDocument3 pagesPower Bank of Empire City 15th PAYROLL: For The Period ofGas dela RosaNo ratings yet

- NJ Seller's Residencey CertificateDocument2 pagesNJ Seller's Residencey CertificateAndrew LiputNo ratings yet

- Sales 32 2023 24Document1 pageSales 32 2023 24Bharat AutomobileNo ratings yet

- Eastern Telecommunications Philippines v. CIRDocument1 pageEastern Telecommunications Philippines v. CIRMarcella Maria KaraanNo ratings yet

- Invoice E2018226816Document3 pagesInvoice E2018226816amjadbonusNo ratings yet

- Pan Card India: Guidelines and InstructionsDocument5 pagesPan Card India: Guidelines and InstructionsMayank SardanaNo ratings yet

- DR - Bharucha Pay Bill May-11Document22 pagesDR - Bharucha Pay Bill May-11Nayan BharuchaNo ratings yet

- CIR Vs Citytrust Investment Phil IncDocument14 pagesCIR Vs Citytrust Investment Phil IncLea AndreleiNo ratings yet

- Full JKSC Online DT Summary Nov 20Document172 pagesFull JKSC Online DT Summary Nov 20Shubham ManikpuriNo ratings yet

- Ea 14Document4 pagesEa 14Nicole BatoyNo ratings yet

- GST Return FilingDocument9 pagesGST Return FilingSanthosh K SNo ratings yet

- Frances Leah Sapla - OKDocument3 pagesFrances Leah Sapla - OKKelvin Jay Sebastian SaplaNo ratings yet

- Tax Planning & ManagementDocument7 pagesTax Planning & Managementoffer manNo ratings yet

- TAXATION 2 Chapter 8 Percentage Tax PDFDocument4 pagesTAXATION 2 Chapter 8 Percentage Tax PDFKim Cristian MaañoNo ratings yet

- SLSP Presentation BIRDocument52 pagesSLSP Presentation BIRprecy.calusaNo ratings yet