IPSAS

IPSAS

Download as pdf or txt

You might also like

- 700FWRDDocument26 pages700FWRDthemoneydon0145No ratings yet

- The PPSAS and The Revised Chart of AccountsDocument98 pagesThe PPSAS and The Revised Chart of AccountsDaniel Salmorin87% (15)

- IPSAS in Your Pocket - August 2022Document61 pagesIPSAS in Your Pocket - August 2022Daniel AdegboyeNo ratings yet

- Portland Mayor's Office 1,000-Person Homeless Shelter MemoDocument8 pagesPortland Mayor's Office 1,000-Person Homeless Shelter MemoKGW News100% (1)

- IPSAS 2 Statement of Cash FlowsDocument37 pagesIPSAS 2 Statement of Cash FlowsAida MohammedNo ratings yet

- Issai 4100 PDFDocument71 pagesIssai 4100 PDFBisuk Tumonggo Ritonga100% (1)

- Dr. Pablito V. Mendoza Sr. High School: A. Parent Teacher Association (PTA)Document6 pagesDr. Pablito V. Mendoza Sr. High School: A. Parent Teacher Association (PTA)project_genome83% (6)

- Atm FraudDocument18 pagesAtm Fraudminky_sharma190% (1)

- IPSAS Detil StandardDocument93 pagesIPSAS Detil StandardNur AsniNo ratings yet

- Advantages of The Implementation of IPSASDocument3 pagesAdvantages of The Implementation of IPSASShilpa KumarNo ratings yet

- IPSAS Preparing For AuditDocument42 pagesIPSAS Preparing For AuditHassan Iqbal PenkarNo ratings yet

- Ipsas Accrual Basis Illustrative Financial StatementsDocument40 pagesIpsas Accrual Basis Illustrative Financial StatementsIoana IordacheNo ratings yet

- IPSAS Handbook PDFDocument6 pagesIPSAS Handbook PDFRonald McRonaldNo ratings yet

- Ipsas ManualDocument180 pagesIpsas ManualJohanna Catahan100% (1)

- International Public Sector Accounting Standards (IPSAS) (A4)Document12 pagesInternational Public Sector Accounting Standards (IPSAS) (A4)Moses K. Wangaruro100% (1)

- Cert IPSAS BrochureDocument2 pagesCert IPSAS BrochureMù SênNo ratings yet

- Acca Certificate IpsasDocument7 pagesAcca Certificate IpsasTawanda Zimbizi100% (1)

- Implementing Cash IPSAS Financial StatementsDocument24 pagesImplementing Cash IPSAS Financial StatementsInternational Consortium on Governmental Financial ManagementNo ratings yet

- Overview of IPSAS StandardsDocument28 pagesOverview of IPSAS StandardsAkinmulewo Ayodele100% (3)

- Cash Basis IPSASDocument18 pagesCash Basis IPSASBlade HasanNo ratings yet

- IPSAS Vs IFRS AU1506 PDFDocument8 pagesIPSAS Vs IFRS AU1506 PDFEar TanNo ratings yet

- Ipsas 12 InventoriesDocument20 pagesIpsas 12 InventoriesheridocNo ratings yet

- UN Audit Training Material On IPSASDocument42 pagesUN Audit Training Material On IPSASrajesh b100% (1)

- Ipsas 14 Events AfterDocument17 pagesIpsas 14 Events AfterPhebieon MukwenhaNo ratings yet

- IPSAS Vs PDFDocument6 pagesIPSAS Vs PDFIrwan Wicaksono100% (1)

- Assessment of The Perception of Foreign Charities On The Benefits and Challenges of Adopting IPSASDocument87 pagesAssessment of The Perception of Foreign Charities On The Benefits and Challenges of Adopting IPSASMuhammad ApridhoniNo ratings yet

- RAROCDocument6 pagesRAROCvishalchigaleNo ratings yet

- Implementing IPSAS at UNHCR PDFDocument43 pagesImplementing IPSAS at UNHCR PDFrafimaneNo ratings yet

- An Overview of Islamic Banking System in Malaysia: Country ReportDocument30 pagesAn Overview of Islamic Banking System in Malaysia: Country ReportChan Yee TeenzNo ratings yet

- ACCA Programme SpecificationDocument6 pagesACCA Programme SpecificationHabib AzamNo ratings yet

- Summary of Standards of AuditingDocument23 pagesSummary of Standards of AuditingMary Grace FajardoNo ratings yet

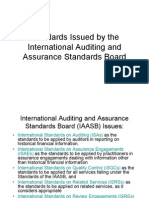

- IAASB StandardsDocument8 pagesIAASB StandardsaccanazmulNo ratings yet

- ACCA Handbook 2018 v7Document16 pagesACCA Handbook 2018 v7TalhaAzamNo ratings yet

- F7 - Presenatation - Day 2Document30 pagesF7 - Presenatation - Day 2anon_17214281No ratings yet

- Financial Accounting Standards BoardDocument12 pagesFinancial Accounting Standards BoardNoor HossainNo ratings yet

- Ipsas 1 - Handbook Ipsas 2018 Vol 1Document922 pagesIpsas 1 - Handbook Ipsas 2018 Vol 1anisaNo ratings yet

- Statements Guidance Notes Issued by IcaiDocument9 pagesStatements Guidance Notes Issued by IcaiSatish MehtaNo ratings yet

- Ipsas 24 BudgetDocument2 pagesIpsas 24 Budgetritunath100% (1)

- 48- دور الصكوك الإسلامية في تمويل عجز الموازنة العامةDocument20 pages48- دور الصكوك الإسلامية في تمويل عجز الموازنة العامةZoheir RABIANo ratings yet

- Budgetary Contol System in Service OrganisationDocument10 pagesBudgetary Contol System in Service OrganisationM S Sridhar100% (16)

- Illustrative Financial Statements O 201210Document316 pagesIllustrative Financial Statements O 201210Yogeeshwaran Ponnuchamy100% (1)

- مجلد 17 العدد الثانيDocument160 pagesمجلد 17 العدد الثانيHayderAlTamimiNo ratings yet

- Ipsas 17 PpeDocument29 pagesIpsas 17 PpeEZEKIELNo ratings yet

- FAS 33 Investment in Sukuk Shares and Similar Instrutments FINAL v3 CleanDocument22 pagesFAS 33 Investment in Sukuk Shares and Similar Instrutments FINAL v3 CleanAhamed Fasharudeen100% (2)

- التحوط في نظام التمويل الإسلامي وإدارة التنمية عند الأزمات الاقتصادية بلجبل عادل وبركات فايزة وجوامح اسماعيلDocument16 pagesالتحوط في نظام التمويل الإسلامي وإدارة التنمية عند الأزمات الاقتصادية بلجبل عادل وبركات فايزة وجوامح اسماعيلBOUAKKAZ NAOUALNo ratings yet

- International Public Sector Accounting Standards Board: 2012 EditionDocument856 pagesInternational Public Sector Accounting Standards Board: 2012 EditionritunathNo ratings yet

- Ipsas 2 Cash Flow Statements 2Document26 pagesIpsas 2 Cash Flow Statements 2lupualin123No ratings yet

- IPSAS Implementation UNOPSDocument5 pagesIPSAS Implementation UNOPSflorica1975No ratings yet

- أثر تطبيق نظام الحوكمة على تحسين اجراءات تحصيل الايرادات الضريبية - دراسة ميدانيةDocument16 pagesأثر تطبيق نظام الحوكمة على تحسين اجراءات تحصيل الايرادات الضريبية - دراسة ميدانيةouafae jowharNo ratings yet

- Accrual Accounting in The Public SectorDocument52 pagesAccrual Accounting in The Public SectorSamuel BrefoNo ratings yet

- Tha4 658 005Document359 pagesTha4 658 005Lamia Nour Ben abdelrahmenNo ratings yet

- The Cash Basis IPSASDocument85 pagesThe Cash Basis IPSASHarry K. MatolaNo ratings yet

- Gov Acc 2019 JaaDocument9 pagesGov Acc 2019 JaaGlaiza Lerio100% (1)

- Statement of Cash FlowsDocument2 pagesStatement of Cash FlowsCatriona Cassandra SantosNo ratings yet

- Advanced Public Sector AccountingDocument408 pagesAdvanced Public Sector AccountingFatin Ferdinand100% (1)

- Improving Public Sector Financial Management in Developing Countries and Emerging EconomiesDocument50 pagesImproving Public Sector Financial Management in Developing Countries and Emerging EconomiesAlia Al ZghoulNo ratings yet

- Accounting Concepts: Fair Presentation Going ConcernDocument12 pagesAccounting Concepts: Fair Presentation Going Concernkim_oun09No ratings yet

- Week 1 .05 Government Accounting Manual and International Public Sector Accounting StandardsDocument21 pagesWeek 1 .05 Government Accounting Manual and International Public Sector Accounting StandardsElaineJrV-Igot100% (1)

- دراسة تحليلية لتطبيق مبادئ الحوكمة في سوق عمان للأوراق الماليةDocument10 pagesدراسة تحليلية لتطبيق مبادئ الحوكمة في سوق عمان للأوراق الماليةmemoires writeNo ratings yet

- Session 4 - Risk Governance & Control Environment v2 - Chris RazookDocument26 pagesSession 4 - Risk Governance & Control Environment v2 - Chris RazookEra HRNo ratings yet

- The PPSAS and The Revised Chart of Accounts: Tools To Enhance Accountability and Transparency in Financial ReportingDocument98 pagesThe PPSAS and The Revised Chart of Accounts: Tools To Enhance Accountability and Transparency in Financial ReportingJhopel Casagnap EmanNo ratings yet

- Preface To PPSAS 10-18 2013Document4 pagesPreface To PPSAS 10-18 2013Ingrid CaobleclolalNo ratings yet

- Course Module - Chapter 1 - Overview of Government AccountingDocument13 pagesCourse Module - Chapter 1 - Overview of Government Accountingssslll2No ratings yet

- 04 x04 Cost-Volume-Profit RelationshipsDocument48 pages04 x04 Cost-Volume-Profit RelationshipsArvin John MasuelaNo ratings yet

- Financial Statement Analysis Suggested Answers and SolutionsDocument12 pagesFinancial Statement Analysis Suggested Answers and SolutionsArvin John MasuelaNo ratings yet

- Scales - ColorDocument1 pageScales - ColorArvin John MasuelaNo ratings yet

- Philippine Deposit Insurance Corporation (Pdic) :: Pdic Act (Ra 3591, As Amended)Document2 pagesPhilippine Deposit Insurance Corporation (Pdic) :: Pdic Act (Ra 3591, As Amended)Arvin John MasuelaNo ratings yet

- Initial Stock Offering and Subscriptions - Memorandum Entry Method Journal Entry MethodDocument4 pagesInitial Stock Offering and Subscriptions - Memorandum Entry Method Journal Entry MethodArvin John MasuelaNo ratings yet

- PARTNERSHIPDocument10 pagesPARTNERSHIPArvin John MasuelaNo ratings yet

- Quizzer 1Document4 pagesQuizzer 1Arvin John MasuelaNo ratings yet

- Synthesis Paper (Masuela, Anjelo)Document4 pagesSynthesis Paper (Masuela, Anjelo)Arvin John MasuelaNo ratings yet

- Mock PreboardDocument12 pagesMock PreboardArvin John MasuelaNo ratings yet

- Far Probs - EvaluationDocument7 pagesFar Probs - EvaluationArvin John Masuela100% (1)

- Bluestone Alley LTR NoteDocument2 pagesBluestone Alley LTR NoteArvin John Masuela88% (8)

- TheEconomist 2024 04 20Document344 pagesTheEconomist 2024 04 20RodrigoNo ratings yet

- WUP2018-F21-Proportion Urban AnnualDocument71 pagesWUP2018-F21-Proportion Urban AnnualLeoo WhiteeNo ratings yet

- Lesotho ConstitutionDocument199 pagesLesotho ConstitutionEd ChikuniNo ratings yet

- Complaint - CalingacionDocument3 pagesComplaint - CalingacionrjpogikaayoNo ratings yet

- The Objectives of The National Youth Policy AreDocument6 pagesThe Objectives of The National Youth Policy AreShweta SinghNo ratings yet

- A 516 - A 516M - 17Document4 pagesA 516 - A 516M - 17picottNo ratings yet

- Rejoinder To Written StatementDocument7 pagesRejoinder To Written StatementAnujNo ratings yet

- CTM ReviewedDocument2 pagesCTM ReviewedAneesh KallumgalNo ratings yet

- Metaethics, Normative, and Applied EthicsDocument4 pagesMetaethics, Normative, and Applied EthicsSandra Mae CabuenasNo ratings yet

- Columbus Bank & Trust vs. Michael A. Eddings Lawsuit: Docket, Notice of Removal, Complaint, Exhibit ADocument110 pagesColumbus Bank & Trust vs. Michael A. Eddings Lawsuit: Docket, Notice of Removal, Complaint, Exhibit AColumbus GA WhispersNo ratings yet

- Wowza Streaming Engine For EC2 - UsersGuideDocument42 pagesWowza Streaming Engine For EC2 - UsersGuidecrejocNo ratings yet

- Free Rider & Rocker Instruction ManualDocument1 pageFree Rider & Rocker Instruction ManualBen SzapiroNo ratings yet

- Good Conduct Time Allowance 2Document12 pagesGood Conduct Time Allowance 2Nikka OsorioNo ratings yet

- Environmental LawDocument15 pagesEnvironmental Lawmohd sakibNo ratings yet

- BANKDocument8 pagesBANKAyesha jamesNo ratings yet

- No Work, No Pay On Nov. 2, Dec. 24 and 31Document2 pagesNo Work, No Pay On Nov. 2, Dec. 24 and 31nut_crackreNo ratings yet

- Judgment of The Court: 14th & 22nd August 2024Document11 pagesJudgment of The Court: 14th & 22nd August 2024nubitse94No ratings yet

- Crude Oil Limited Purchases An Oil Tanker Depot On July PDFDocument1 pageCrude Oil Limited Purchases An Oil Tanker Depot On July PDFTaimur TechnologistNo ratings yet

- 5311XXXXXXXXX950030 03 2024Document4 pages5311XXXXXXXXX950030 03 2024adityayadavasyNo ratings yet

- TransfdDocument104 pagesTransfdNgoc Tram VanNo ratings yet

- Charge of GSTDocument86 pagesCharge of GSTmonikaduhan29No ratings yet

- English Literature: Rejhane JonuziDocument5 pagesEnglish Literature: Rejhane JonuziRejhane JonuziNo ratings yet

- A Study On Investors Preferences Towards Mutual FundsDocument64 pagesA Study On Investors Preferences Towards Mutual FundsVini SreeNo ratings yet

- Lesson 1 - Overview of CybercrimeDocument52 pagesLesson 1 - Overview of Cybercrimejacob tradioNo ratings yet

- Howton v. Fecsko, Et Al. ComplaintDocument22 pagesHowton v. Fecsko, Et Al. ComplaintjhbryanNo ratings yet

- LindsayHuge CandidateSurveyDocument3 pagesLindsayHuge CandidateSurveyInjustice Watch100% (1)