The memo analyzes three strategies for RJR Nabisco proposed by different acquirers to determine which provides the highest valuation of the company. It calculates values using weighted average cost of capital and discounted cash flows, finding values per share of $115-149 depending on the strategy and growth rate assumed. The main differences between the strategies are their capital structures and operating plans. An auction of the company was reasonable to promote competition and shareholder value, though it risked taking on large debt.

The memo analyzes three strategies for RJR Nabisco proposed by different acquirers to determine which provides the highest valuation of the company. It calculates values using weighted average cost of capital and discounted cash flows, finding values per share of $115-149 depending on the strategy and growth rate assumed. The main differences between the strategies are their capital structures and operating plans. An auction of the company was reasonable to promote competition and shareholder value, though it risked taking on large debt.

The memo analyzes three strategies for RJR Nabisco proposed by different acquirers to determine which provides the highest valuation of the company. It calculates values using weighted average cost of capital and discounted cash flows, finding values per share of $115-149 depending on the strategy and growth rate assumed. The main differences between the strategies are their capital structures and operating plans. An auction of the company was reasonable to promote competition and shareholder value, though it risked taking on large debt.

The memo analyzes three strategies for RJR Nabisco proposed by different acquirers to determine which provides the highest valuation of the company. It calculates values using weighted average cost of capital and discounted cash flows, finding values per share of $115-149 depending on the strategy and growth rate assumed. The main differences between the strategies are their capital structures and operating plans. An auction of the company was reasonable to promote competition and shareholder value, though it risked taking on large debt.

Download as DOCX, PDF, TXT or read online from Scribd

Download as docx, pdf, or txt

You are on page 1/ 4

MEMO

RJR Nabisco BY: Yuxiang Fan, Da Luo, Di Jia, Tiantao Zheng

Executive Summary Three strategies of RJR Nabisco are presented by different acquirers. The following memo is trying to work out the strategy that gives the highest valuation of the firm.

Values of RJR under Different Scenarios

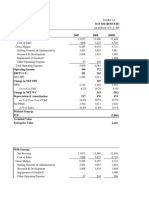

In order to calculate the value of the company, we first need to unlever to derive beta asset or return on asset. As the EBIT/Int. Exp. of RJR falls on BBB, the beta debt is 0.151 for both 1986 and 87. So the beta asset can be given in the following table. Year 1986 1987

D E V Beta D Beta E Beta A 11389 5312 16701 0.151 1.24 0.497 10823 6038 16861 0.151 0.67 0.337 Average Beta Asset 0.417 Average Return on Asset 11.92% Then we need to relever to calculate beta equity under different debt ratios across time, using beta E=beta A + (beta A- beta D) D/E We adopt WACC (APV can also be applied in this case, which is equivalent to WACC) to calculate the value of RJR under the strategy given by pre-bid, Management Group, and KKR respectively. After working out Rd and Re with CAPM, we use WACC=Rd* (1-Tc) *D/V + Re*E/V to calculate the different WACCs of each period. Here we have made an assumption that the corporate tax rate is constant at 35%. We also estimate that there is an assumed debt of $5000 million in 1988. Then we may use the WACCs to discount the FCFs of each period. The sum of the present values will be the total value of company. We also work out the share prices given the growth rate of 0%, 2% and 4% after 1998. The calculating process can be seen in the appendices. Values of RJR Under Different Strategies ($/share) Growth Rate Pre-bid Strategy Management Group Strategy KKR Strategy

0% 115.02 118.48 115.63

2% 127.32 129.34 128.64

4% 145.83 145.81 148.22

The Reasons That Accounts for Differences

The differences in the value of the three operating plans are mainly from capital structure and operating strategy used by two bidders. Both bidders believed that the value of stock was undervalued by the market and the cash flow of RJR was strong and stable, which can utilize more aggressive capital structure to save taxes and therefore increasing value of the company. Besides, KKR and the Management Group thought that the operating strategy used by company could not maximize the shareholders value. The Management Group believed that stock market undervalued the strong and stable cash flow generated from tobacco business and market did not fully value its food business since its connection with selling tobacco. In addition, during that time, food industry was experiencing a major restructuring and revaluation and Johnson had experience selling food assets. Therefore, the Management Groups strategy was to sell RJRs food business and take tobacco business private. The Management Group believed that the new strategy would eliminate undervaluation and generate more gains for shareholders. Moreover, this strategy was financed by long term debt, which resulted in greater valuation because of tax shield. However, KKRs strategy was to keep all of the tobacco business and most of food business because KKR thought that retaining food business and operating it correctly would generate more value than just selling it. Also, KKRs strategy took more debt, which led to higher tax shield and valuation. Thus, the operating strategy and capital structure are the major drivers for the difference among three plans.

Evaluation of the Special Committees Auction

Special Committees use of an auction for the sale of RJR Nabisco is very reasonable and protective to RJR Nabiscos shareholders. Such auction will benefit shareholders value by allowing all potential buyers to compete with their highest bid offer. Moreover, this auction will promote a quick and smooth buyout process as it gives a specific deadline to bid. This would prevent the joint-bid case by KKR and Management Group that lasted for a year. If all parties are privately negotiating with one another, the bidding process would be prolonged which would not benefit shareholders interest. However, one drawback of such auction is that competition will drive the valuation of RJR Nabisco very high, meaning that after the buyout, RJR Nabisco would incur a significant amount of debt, which might damage remaining shareholders longer term value. Through our analysis, the operating strategy and capital structure are the major drivers for the difference among three plans, since more debt would lead to higher tax shield and therefore higher valuation.