Winfield Case

Winfield Case

Download as docx, pdf, or txt

You might also like

- Hill Country Solution ExcelDocument1 pageHill Country Solution Excelankujai88No ratings yet

- Pacific Grove Spice Company Case Write UpDocument3 pagesPacific Grove Spice Company Case Write UpVaishnavi Gnanasekaran100% (4)

- Case 34 - The Wm. Wrigley Jr. CompanyDocument72 pagesCase 34 - The Wm. Wrigley Jr. CompanyQUYNH100% (1)

- Icwim PDFDocument2 pagesIcwim PDFWolfgangNo ratings yet

- Ocean Carries HBS Case StudyDocument4 pagesOcean Carries HBS Case StudyRatul EsrarNo ratings yet

- New Heritage DollDocument4 pagesNew Heritage Dolls_gonzalez75No ratings yet

- Accounting and Bookkeeping Business PlanDocument45 pagesAccounting and Bookkeeping Business PlanDOZYENo ratings yet

- Winfield ManagementDocument5 pagesWinfield Managementmadhav1111No ratings yet

- Gulf Oil ExhibitsDocument20 pagesGulf Oil Exhibitsaskpeeves1No ratings yet

- Group 12 - Automation Consulting ServicesDocument1 pageGroup 12 - Automation Consulting ServicesRISHABH GUPTANo ratings yet

- Harley DavidsonDocument5 pagesHarley DavidsonpagalinsanNo ratings yet

- Larry Steffen-Valuing Stock Options in A Compensation PackageDocument4 pagesLarry Steffen-Valuing Stock Options in A Compensation PackageAbhinandan Singh0% (2)

- Chapter 7 Solution of Fundamental of Financial Accouting by EDMONDS (4th Edition)Document152 pagesChapter 7 Solution of Fundamental of Financial Accouting by EDMONDS (4th Edition)Awais Azeemi50% (4)

- Anandam Manufacturing CompanyDocument9 pagesAnandam Manufacturing CompanyAijaz AslamNo ratings yet

- Case Study 4 Winfield Refuse Management, Inc.: Raising Debt vs. EquityDocument5 pagesCase Study 4 Winfield Refuse Management, Inc.: Raising Debt vs. EquityAditya DashNo ratings yet

- Case Study 4Document8 pagesCase Study 4Ojas GuptaNo ratings yet

- Submitted To: Submitted By: Dr. Kulbir Singh Vinay Singh 201922106 Aurva Bhardwaj 201922066 Deepanshu Gupta 201922069 Sameer Kumbhalwar 201922097Document3 pagesSubmitted To: Submitted By: Dr. Kulbir Singh Vinay Singh 201922106 Aurva Bhardwaj 201922066 Deepanshu Gupta 201922069 Sameer Kumbhalwar 201922097Aurva BhardwajNo ratings yet

- Hill Country Snack Foods CoDocument1 pageHill Country Snack Foods CoKriti AhujaNo ratings yet

- Midland Case CalculationsDocument24 pagesMidland Case CalculationsSharry_xxx60% (5)

- Winfield Refuse ManagementDocument13 pagesWinfield Refuse ManagementAnshul Sehgal100% (3)

- Midland Energy Group A5Document3 pagesMidland Energy Group A5Deepesh Moolchandani0% (1)

- Assignment #2 Workgroup E IttnerDocument8 pagesAssignment #2 Workgroup E IttnerAziz Abi AadNo ratings yet

- Hill Country Snack Foods Co - UDocument4 pagesHill Country Snack Foods Co - Unipun9143No ratings yet

- Winfield Refuse ManagementDocument13 pagesWinfield Refuse Managementnishant JaiswalNo ratings yet

- Case Study: Hill Country Snack Foods " HCSF " (With Soluion )Document12 pagesCase Study: Hill Country Snack Foods " HCSF " (With Soluion )Kamran Shabbir50% (2)

- Bidding For Hertz Leveraged Buyout, Spreadsheet SupplementDocument12 pagesBidding For Hertz Leveraged Buyout, Spreadsheet SupplementAmit AdmuneNo ratings yet

- Mehak Bluntly MediaDocument18 pagesMehak Bluntly Mediahimanshu sagarNo ratings yet

- FIN 370 Final Exam 30 Questions With AnswersDocument11 pagesFIN 370 Final Exam 30 Questions With Answersassignmentsehelp0% (1)

- 13 Earned Value ManagementDocument9 pages13 Earned Value ManagementAbhinandan Singh100% (1)

- Teuer Furniture (A)Document14 pagesTeuer Furniture (A)Abhinandan SinghNo ratings yet

- Saatchi&SaatchiDocument5 pagesSaatchi&SaatchiAbhinandan SinghNo ratings yet

- Flash Memory IncDocument7 pagesFlash Memory IncAbhinandan SinghNo ratings yet

- Accounting IAS Model Answers Series 2 2010Document17 pagesAccounting IAS Model Answers Series 2 2010Aung Zaw HtweNo ratings yet

- DBBL ChargesDocument9 pagesDBBL ChargesAhmadullah Sohag100% (1)

- Winfieldpresentationfinal 130212133845 Phpapp02Document26 pagesWinfieldpresentationfinal 130212133845 Phpapp02Sukanta JanaNo ratings yet

- Continental CarriersDocument10 pagesContinental Carriersnipun9143No ratings yet

- Corporate Finance - Hill Country Snack FoodDocument11 pagesCorporate Finance - Hill Country Snack FoodNell MizunoNo ratings yet

- Case Study - Linear Tech - Christopher Taylor - SampleDocument9 pagesCase Study - Linear Tech - Christopher Taylor - Sampleakshay87kumar8193No ratings yet

- Winfield Refuse Management Inc. Raising Debt vs. EquityDocument13 pagesWinfield Refuse Management Inc. Raising Debt vs. EquitynmenalopezNo ratings yet

- Continental CarriersDocument4 pagesContinental CarriersNIkhil100% (2)

- Teuer Furniture Case AnalysisDocument3 pagesTeuer Furniture Case AnalysisPankaj KumarNo ratings yet

- This Study Resource Was: 1 Hill Country Snack Foods CoDocument9 pagesThis Study Resource Was: 1 Hill Country Snack Foods CoPavithra TamilNo ratings yet

- Hampton Suggested AnswersDocument5 pagesHampton Suggested Answersenkay12100% (3)

- Winfield PPT 27 FEB 13Document13 pagesWinfield PPT 27 FEB 13prem_kumar83g100% (4)

- Winfield RefuseDocument5 pagesWinfield RefuseAbhishek BaratamNo ratings yet

- Hill Country SnackDocument8 pagesHill Country Snackkiller dramaNo ratings yet

- Linear TechnologyDocument4 pagesLinear TechnologySatyajeet Sahoo100% (2)

- Midland Energy A1Document30 pagesMidland Energy A1CarsonNo ratings yet

- 01 - Midland AnalysisDocument7 pages01 - Midland AnalysisBadr Iftikhar100% (1)

- Jones Electrical DistributionDocument5 pagesJones Electrical DistributionAsif AliNo ratings yet

- Guna Fibres Working CapitalDocument5 pagesGuna Fibres Working CapitalRahul KumarNo ratings yet

- Case Analysis - Cost of CapitalDocument5 pagesCase Analysis - Cost of CapitalHazraphine LinsoNo ratings yet

- Finance Case - Blaine KitchenwareDocument8 pagesFinance Case - Blaine KitchenwareodaiissaNo ratings yet

- Question 1Document9 pagesQuestion 1Minh HàNo ratings yet

- Group2 - Clarkson Lumber Company Case AnalysisDocument3 pagesGroup2 - Clarkson Lumber Company Case AnalysisDavid WebbNo ratings yet

- Cooper Case SolutionsDocument6 pagesCooper Case SolutionsDarshan Salgia100% (1)

- Linear Technology Payout Policy Case 3Document4 pagesLinear Technology Payout Policy Case 3Amrinder SinghNo ratings yet

- Session 10 Simulation Questions PDFDocument6 pagesSession 10 Simulation Questions PDFVAIBHAV WADHWA0% (1)

- Example MidlandDocument5 pagesExample Midlandtdavis1234No ratings yet

- Midland WACCDocument2 pagesMidland WACCDeniz Minican100% (3)

- Midland CaseDocument5 pagesMidland CaseJessica Bill100% (3)

- Tire City Inc.Document6 pagesTire City Inc.Samta Singh YadavNo ratings yet

- LinearDocument6 pagesLinearjackedup211No ratings yet

- Dividend Policy at Linear TechnologyDocument9 pagesDividend Policy at Linear TechnologySAHILNo ratings yet

- Afm-Unit 1Document26 pagesAfm-Unit 1joelmanoj98No ratings yet

- NO Soal: Tipe 1Document24 pagesNO Soal: Tipe 1AdirtnNo ratings yet

- WinfieldDocument4 pagesWinfieldMOHIT SINGHNo ratings yet

- Financial Management Notes 1Document55 pagesFinancial Management Notes 1Praduman SharmaNo ratings yet

- FIN222 Autumn2016 Tutorials Tutorial 8Document8 pagesFIN222 Autumn2016 Tutorials Tutorial 8HELENANo ratings yet

- FIN 370 Final Exam - AssignmentDocument11 pagesFIN 370 Final Exam - AssignmentstudentehelpNo ratings yet

- G GeniusDocument26 pagesG GeniusAbhinandan SinghNo ratings yet

- Use More SoapsDocument9 pagesUse More SoapsAbhinandan SinghNo ratings yet

- Category Management 2Document9 pagesCategory Management 2Abhinandan SinghNo ratings yet

- Starbucks Deliveringcustomerservice 160222181028Document11 pagesStarbucks Deliveringcustomerservice 160222181028Abhinandan SinghNo ratings yet

- World CSR Congress: Integrating Sustainability Into A Global OrganizationDocument12 pagesWorld CSR Congress: Integrating Sustainability Into A Global OrganizationAbhinandan SinghNo ratings yet

- Visualmerchandising 121126111353 Phpapp02Document145 pagesVisualmerchandising 121126111353 Phpapp02Abhinandan SinghNo ratings yet

- Merve BEKTAŞ Didem ŞAHİN Sara OsmanoğluDocument22 pagesMerve BEKTAŞ Didem ŞAHİN Sara OsmanoğluAbhinandan SinghNo ratings yet

- Batiste 2in1 Dry Shampoo & Conditioner: Refreshes Roots and Targets Dryness For Gorgeously Soft, Conditioned HairDocument11 pagesBatiste 2in1 Dry Shampoo & Conditioner: Refreshes Roots and Targets Dryness For Gorgeously Soft, Conditioned HairAbhinandan SinghNo ratings yet

- Hola Kola Case StudyDocument8 pagesHola Kola Case StudyAbhinandan Singh100% (1)

- General Motors and Its SuppliersDocument8 pagesGeneral Motors and Its SuppliersAbhinandan SinghNo ratings yet

- Freelancing ListDocument29 pagesFreelancing ListAbhinandan SinghNo ratings yet

- Apple Case Analysis V3Document6 pagesApple Case Analysis V3Abhinandan SinghNo ratings yet

- Setting The Rules Dean BakerDocument11 pagesSetting The Rules Dean BakerOccupyEconomicsNo ratings yet

- Banking and Finance EssayDocument2 pagesBanking and Finance EssayRox31No ratings yet

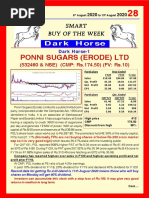

- Dark Horse & Investment Pick From Smart InvestmentDocument2 pagesDark Horse & Investment Pick From Smart InvestmentMukesh Gupta100% (2)

- Capital Budgeting SumsDocument6 pagesCapital Budgeting SumsDeep DebnathNo ratings yet

- Accidental InsuranceDocument33 pagesAccidental InsuranceHarinarayan PrajapatiNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Mayank GandhiNo ratings yet

- National Bank of Pakistan Product Key Fact Statement: 2% of Adjustment Amount + FEDDocument3 pagesNational Bank of Pakistan Product Key Fact Statement: 2% of Adjustment Amount + FEDMuhammad TauseefNo ratings yet

- G.O.No.282, Dated 26 October 2015.: Government of Tamil Nadu 2015Document2 pagesG.O.No.282, Dated 26 October 2015.: Government of Tamil Nadu 2015Gowtham Raj50% (2)

- Banking Institutions History Classifications and FunctionsDocument13 pagesBanking Institutions History Classifications and FunctionsJessielyn GialogoNo ratings yet

- Entrepreneurship Development Program Available in BangladeshDocument22 pagesEntrepreneurship Development Program Available in BangladeshAriful IslamNo ratings yet

- 2 Ndquarter 11Document2 pages2 Ndquarter 11abigail zipaganNo ratings yet

- PEE Assignment 1Document2 pagesPEE Assignment 1Wilfred ThomasNo ratings yet

- SH FormsDocument42 pagesSH FormsRajeev KumarNo ratings yet

- Eureeca PDFDocument8 pagesEureeca PDFAmir Al-AmirNo ratings yet

- Presentation On Types of DepositDocument17 pagesPresentation On Types of DepositSumit Samtani0% (2)

- GP Chargeback GuideDocument9 pagesGP Chargeback Guidetigohan0% (1)

- Problem Set PpeDocument11 pagesProblem Set PpeHdhsiaihagatataNo ratings yet

- Rules of Debit and CreditDocument4 pagesRules of Debit and CreditGlesa SalienteNo ratings yet

- Economics (Simple and Compound Interest#2)Document17 pagesEconomics (Simple and Compound Interest#2)api-2636776733% (3)

- Alm CanaraDocument12 pagesAlm CanaraMohmmedKhayyumNo ratings yet

- Problems Solved Pay Back PeriodDocument7 pagesProblems Solved Pay Back PeriodAfthab Muhammed67% (3)

- Case Study SolutionDocument10 pagesCase Study SolutionSidra ArshadNo ratings yet

- Paper Analysis of NTA UGC - NET COMMERCE December 2019 PDFDocument7 pagesPaper Analysis of NTA UGC - NET COMMERCE December 2019 PDFVikram DograNo ratings yet

- June 11 DipIFR AnswersDocument10 pagesJune 11 DipIFR AnswersjaimaakalikaNo ratings yet

- Permission For Deposit of Goods in A Warehouse UnderDocument1 pagePermission For Deposit of Goods in A Warehouse UnderWelcome 1995No ratings yet