Starbucks 11.1

Starbucks 11.1

Download as docx, pdf, or txt

You might also like

- Burton Sensors SheetDocument128 pagesBurton Sensors Sheetchirag shah14% (7)

- Schaum's Outline of Basic Business Mathematics, 2edFrom EverandSchaum's Outline of Basic Business Mathematics, 2edRating: 5 out of 5 stars5/5 (2)

- 3 Statement Model - Blank TemplateDocument3 pages3 Statement Model - Blank Templated11210175No ratings yet

- Business Finance Assignment 2Document8 pagesBusiness Finance Assignment 2Akshat100% (1)

- F2 - Past PapersDocument298 pagesF2 - Past Papersbilligee73% (11)

- Ceres Gardening Company SubmissionDocument7 pagesCeres Gardening Company SubmissionpranamyaNo ratings yet

- Case 5Document3 pagesCase 5rizkirachNo ratings yet

- Pacific Grove Spice CompanyDocument3 pagesPacific Grove Spice CompanyLaura JavelaNo ratings yet

- Exercise Problems - 485 Fixed Income 2021Document18 pagesExercise Problems - 485 Fixed Income 2021Nguyen hong LinhNo ratings yet

- Case 5 - What Are We Really WorthDocument7 pagesCase 5 - What Are We Really WorthMariaAngelicaMargenApe100% (2)

- Cost Accounting Theory NotesDocument41 pagesCost Accounting Theory NotesShrividhya Venkata Prasath86% (7)

- Burton ExcelDocument128 pagesBurton ExcelJaydeep SheteNo ratings yet

- Coca Cola - With Notes On Discount Factor CalculationDocument20 pagesCoca Cola - With Notes On Discount Factor CalculationJared HerberNo ratings yet

- Quiz 1 Practice ProblemsDocument8 pagesQuiz 1 Practice ProblemsUmaid FaisalNo ratings yet

- Key Performance Indicators (Kpis) : FormulaeDocument4 pagesKey Performance Indicators (Kpis) : FormulaeAfshan AhmedNo ratings yet

- Bond Stock Valuation Gr2 07-03Document13 pagesBond Stock Valuation Gr2 07-03Himanshu GuptaNo ratings yet

- Bosch (Akash Negi-JL19FS006) Assumptions Used in Valuation and Their RationaleDocument4 pagesBosch (Akash Negi-JL19FS006) Assumptions Used in Valuation and Their Rationaleakash NegiNo ratings yet

- Case 6 MathDocument16 pagesCase 6 MathSaraQureshiNo ratings yet

- CBO's August 2010 Baseline: Medicare: by Fiscal YearDocument10 pagesCBO's August 2010 Baseline: Medicare: by Fiscal Yearapi-27836025No ratings yet

- Walt DisneyDocument40 pagesWalt DisneyRahil VermaNo ratings yet

- Revision Exercise 2 - Int Rates + Capl Budgeting - SolutionsDocument25 pagesRevision Exercise 2 - Int Rates + Capl Budgeting - SolutionsBaher WilliamNo ratings yet

- Ratio AnalysisDocument6 pagesRatio Analysisamitca9No ratings yet

- Harley-Davidson, Inc. (HOG) Stock Financials - Annual Income StatementDocument5 pagesHarley-Davidson, Inc. (HOG) Stock Financials - Annual Income StatementThe Baby BossNo ratings yet

- Time Value of Money APPBDocument10 pagesTime Value of Money APPBkartalNo ratings yet

- Marks & Spencer PLCDocument7 pagesMarks & Spencer PLCMoona AwanNo ratings yet

- Earnings based-ROE(s)Document14 pagesEarnings based-ROE(s)Vaishali GuptaNo ratings yet

- SENEA Financial AnalysisDocument22 pagesSENEA Financial Analysissidrajaffri72No ratings yet

- WACC TemplateDocument13 pagesWACC TemplateAsad AminNo ratings yet

- Leverage Buyout of Balrampur Chini Mills LimitedDocument16 pagesLeverage Buyout of Balrampur Chini Mills LimitedAarti KatochNo ratings yet

- Research Needed For Question 5Document4 pagesResearch Needed For Question 5Ahmed MahmoudNo ratings yet

- Evercore Partners 8.6.13 PDFDocument6 pagesEvercore Partners 8.6.13 PDFChad Thayer VNo ratings yet

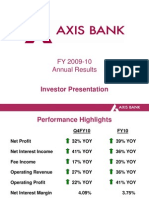

- FY 2009-10 Annual Results: Investor PresentationDocument34 pagesFY 2009-10 Annual Results: Investor PresentationDujesh KardamNo ratings yet

- 17 Aishwarya GuptaDocument5 pages17 Aishwarya Guptaanshul singhalNo ratings yet

- FM fund post - question 2Document10 pagesFM fund post - question 2Valeria CTNo ratings yet

- UST - B - Exhibits+TemplateDocument8 pagesUST - B - Exhibits+TemplateDinhkhanh NguyenNo ratings yet

- Amaha Advanced 3 - StatementModelDocument6 pagesAmaha Advanced 3 - StatementModelamahaktNo ratings yet

- Financial Analysis Template EBayDocument18 pagesFinancial Analysis Template EBayHarit keshruwalaNo ratings yet

- Supplement Du Pont 1983Document13 pagesSupplement Du Pont 1983Eesha KNo ratings yet

- Earnings based-ROEDocument15 pagesEarnings based-ROERahul SinghNo ratings yet

- Financial Analysis Template FinalDocument8 pagesFinancial Analysis Template FinalHarit keshruwalaNo ratings yet

- I. Income StatementDocument27 pagesI. Income StatementNidhi KaushikNo ratings yet

- 3 Statement Modeling With Iterations SummaryDocument7 pages3 Statement Modeling With Iterations SummaryEmperor OverwatchNo ratings yet

- Class Exercise Fashion Company Three Statements Model - CompletedDocument16 pagesClass Exercise Fashion Company Three Statements Model - CompletedbobNo ratings yet

- Byjus Base ModelDocument8 pagesByjus Base Modelsharma.kunal70No ratings yet

- Intro to Bank Valuation Interactive Exercise Support (Template)Document28 pagesIntro to Bank Valuation Interactive Exercise Support (Template)wayiso kocheNo ratings yet

- Management of Monetary Resource of GSK: Course: Faculty: Group NameDocument27 pagesManagement of Monetary Resource of GSK: Course: Faculty: Group Nameborn2growNo ratings yet

- Assignment (Project)Document5 pagesAssignment (Project)davidNo ratings yet

- 04.06.2016dividend PolicyDocument35 pages04.06.2016dividend PolicyAbdu MohammedNo ratings yet

- Duration Problems: Problem 1Document6 pagesDuration Problems: Problem 1Sanjeev100% (1)

- Exam 3C Take HomeDocument9 pagesExam 3C Take HomeTerra RoenNo ratings yet

- Nike Inc - Cost of Capital - Syndicate 10Document16 pagesNike Inc - Cost of Capital - Syndicate 10Anthony KwoNo ratings yet

- 10 - Deepika - Suzlon EnergyDocument24 pages10 - Deepika - Suzlon Energyrajat_singlaNo ratings yet

- W1 - Implied Equity PremiumDocument7 pagesW1 - Implied Equity PremiumChip choiNo ratings yet

- Group4 DeluxeDocument7 pagesGroup4 DeluxeHEM BANSAL100% (1)

- 5 Solution Maf302Document6 pages5 Solution Maf302diana.p7reiraNo ratings yet

- BASIC MODEL - Construction.Document10 pagesBASIC MODEL - Construction.KAVYA GUPTANo ratings yet

- Valuation Under Mergers and Acquisition_IBDocument3 pagesValuation Under Mergers and Acquisition_IBipm02khushijNo ratings yet

- Institute of Actuaries of Australia Course 2A Life Insurance May 2005 Examinations Answer All 6 Questions. (9 Marks)Document9 pagesInstitute of Actuaries of Australia Course 2A Life Insurance May 2005 Examinations Answer All 6 Questions. (9 Marks)Jeff GundyNo ratings yet

- Particulars (INR in Crores) FY2015A FY2016A FY2017A FY2018ADocument6 pagesParticulars (INR in Crores) FY2015A FY2016A FY2017A FY2018AHamzah HakeemNo ratings yet

- FM205 CaseDocument33 pagesFM205 CaseAastik RockzzNo ratings yet

- Lecture-3 & 4 - Common Size and Comparative AnalysisDocument28 pagesLecture-3 & 4 - Common Size and Comparative AnalysissanyaNo ratings yet

- Polaroid 1996 CalculationDocument8 pagesPolaroid 1996 CalculationDev AnandNo ratings yet

- BUS 525 LOS1 Spring 2023Document55 pagesBUS 525 LOS1 Spring 2023Asif Hossain Hemel 2315078660No ratings yet

- Brand Identity KapfererDocument15 pagesBrand Identity KapfererMonika ChughNo ratings yet

- Module 6 SolutionsDocument6 pagesModule 6 SolutionsNeha Wadhwani AhujaNo ratings yet

- Dove - Swot AnalysisDocument9 pagesDove - Swot AnalysisRajiv BhatiyaNo ratings yet

- Strategic Financial Management: An Overview: After Reading This Chapter, You Will Be Conversant WithDocument9 pagesStrategic Financial Management: An Overview: After Reading This Chapter, You Will Be Conversant WithAnish MittalNo ratings yet

- The Why of Buy: Understanding Consumer BehaviorDocument13 pagesThe Why of Buy: Understanding Consumer Behaviorusama iqbalNo ratings yet

- Book Building IPODocument2 pagesBook Building IPOSarada NagNo ratings yet

- CAC1107200904 Accounting IADocument6 pagesCAC1107200904 Accounting IAGift MoyoNo ratings yet

- Overheads Bamboo Brush Bamboo Bottles: Unit Price Estimation For Bamboo Brushes and Bottles For 12 Months (In INR)Document2 pagesOverheads Bamboo Brush Bamboo Bottles: Unit Price Estimation For Bamboo Brushes and Bottles For 12 Months (In INR)Chirag JainNo ratings yet

- FA5Document3 pagesFA5Gray JavierNo ratings yet

- List of Tables and Figures Executive Summary 2.0 Situation AnalysisDocument27 pagesList of Tables and Figures Executive Summary 2.0 Situation AnalysischerikokNo ratings yet

- Ra 9298 Accountancy Act of 2004 MCQDocument11 pagesRa 9298 Accountancy Act of 2004 MCQKim Patrick MarianoNo ratings yet

- Ch05TB PDFDocument16 pagesCh05TB PDFMico Duñas CruzNo ratings yet

- Pom ReviewerDocument5 pagesPom ReviewerMorales Ma. CristaNo ratings yet

- B02 Final Exam Review QuestionsDocument8 pagesB02 Final Exam Review QuestionsnigaroNo ratings yet

- Business Studies - Objective Part - Section 1Document64 pagesBusiness Studies - Objective Part - Section 1Edu Tainment100% (1)

- Project On Volatility in Indian Stock MarketDocument41 pagesProject On Volatility in Indian Stock MarketPoonam Singh80% (5)

- Updated 2002 - 2009Document172 pagesUpdated 2002 - 2009Laila SarhanNo ratings yet

- Post Purchase Behaviour: Purchase Evaluation, Customer SatisfactionDocument19 pagesPost Purchase Behaviour: Purchase Evaluation, Customer Satisfactionmanojverma231988No ratings yet

- Intacc Reviewer - Module 4Document20 pagesIntacc Reviewer - Module 4Lizette Janiya SumantingNo ratings yet

- Management Information System Cia - 1Document9 pagesManagement Information System Cia - 1ISHDEV SINGH DHEER 1620217No ratings yet

- Syllabus Financial Reporting and Analysis - Level One ModuleDocument8 pagesSyllabus Financial Reporting and Analysis - Level One ModuleJazzer NapixNo ratings yet

- Paper BVRMG 101: EnglishDocument14 pagesPaper BVRMG 101: Englishsunilrs1980No ratings yet

- Overall Audit Plan and Audit Program: ©2012 Prentice Hall Business Publishing, Auditing 14/e, Arens/Elder/BeasleyDocument36 pagesOverall Audit Plan and Audit Program: ©2012 Prentice Hall Business Publishing, Auditing 14/e, Arens/Elder/BeasleydindaadaniNo ratings yet

- Building Customer ValueDocument41 pagesBuilding Customer Valueapi-3793009100% (5)

- Far0 ReviewerDocument8 pagesFar0 ReviewerAshianna KimNo ratings yet

- Chapter 3: Marketing Strategy: A. Research and AnalysisDocument13 pagesChapter 3: Marketing Strategy: A. Research and AnalysisMarrNo ratings yet

- Cost Accounting 1Document4 pagesCost Accounting 1Rohan RalliNo ratings yet