ANZ - Green Field Project

ANZ - Green Field Project

Download as docx, pdf, or txt

You might also like

- Spinoza and Heidegger Ontological Anticipation and InterpretationDocument17 pagesSpinoza and Heidegger Ontological Anticipation and Interpretationrahimibehzad936No ratings yet

- SME Financing PPT DTDocument28 pagesSME Financing PPT DTdeepaktandon86% (7)

- BCP Framework For Assessment of Crypto Tokens - Block 2Document25 pagesBCP Framework For Assessment of Crypto Tokens - Block 2selcuk100% (1)

- FINTECHDocument3 pagesFINTECHNurul AqilahNo ratings yet

- NXT Network: Energy and Cost Efficiency AnalysisDocument13 pagesNXT Network: Energy and Cost Efficiency AnalysisPetrNo ratings yet

- Talk Fusion Class-Action ComplaintDocument110 pagesTalk Fusion Class-Action ComplaintThompson Burton100% (2)

- The Alabama Reading Initiative Program Evaluation Report - ALSDE Research & DevelopmentDocument41 pagesThe Alabama Reading Initiative Program Evaluation Report - ALSDE Research & DevelopmentTrisha Powell Crain100% (1)

- Central Bank Digital Currencies For Cross-Border PaymentsDocument37 pagesCentral Bank Digital Currencies For Cross-Border PaymentsFranzNo ratings yet

- Blockchain and Central Bank Digital CurrencyDocument7 pagesBlockchain and Central Bank Digital CurrencyIgorFilkoNo ratings yet

- Blockchain-Based Trade FinanceDocument4 pagesBlockchain-Based Trade FinanceMuhammadNabhanNaufalNo ratings yet

- FINALDocument20 pagesFINALNishant PawarNo ratings yet

- The Case For Central Bank Digital CurrenciesDocument6 pagesThe Case For Central Bank Digital CurrenciesKeamogetse MotlogeloaNo ratings yet

- @@ Credit Risk Management On The Financial Performance of Banks in Kenya For The Period 2000 - 2006Document9 pages@@ Credit Risk Management On The Financial Performance of Banks in Kenya For The Period 2000 - 2006Rafiqul IslamNo ratings yet

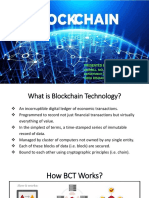

- Block ChainDocument12 pagesBlock ChainISHA AGGARWALNo ratings yet

- The Development of Asset Securitisation in MalaysiaDocument14 pagesThe Development of Asset Securitisation in MalaysiaAK FleurNo ratings yet

- Bitcoins Incentive StructureDocument23 pagesBitcoins Incentive StructureShruti SinghNo ratings yet

- Blockchain by Md. ABU TORABDocument15 pagesBlockchain by Md. ABU TORABMohammad Abu TorabNo ratings yet

- Amity School of Engineering & Technology Noida, Uttar PradeshDocument16 pagesAmity School of Engineering & Technology Noida, Uttar PradeshUjjwal BhatnagarNo ratings yet

- Cryptocurrency Risk and Governance Challenges Marizah Minhat & MazniDocument175 pagesCryptocurrency Risk and Governance Challenges Marizah Minhat & MazniLeong Kin PongNo ratings yet

- Deutsche Bank CIO Report Central Bank Digital CurrenciesDocument15 pagesDeutsche Bank CIO Report Central Bank Digital CurrenciesForkLogNo ratings yet

- McKinsey Telecoms. RECALL No. 11, 2010 - Mature MarketsDocument66 pagesMcKinsey Telecoms. RECALL No. 11, 2010 - Mature MarketskentselveNo ratings yet

- DefiDocument32 pagesDefikingslyjohan3No ratings yet

- Lorie Savage Capital JB 1949Document11 pagesLorie Savage Capital JB 1949akumar_45291100% (2)

- The Future of Central Bank Digital Currencies and Decentralized FinanceDocument3 pagesThe Future of Central Bank Digital Currencies and Decentralized FinanceLudovic Marc CoutinhoNo ratings yet

- Global Standards Mapping InitiativeDocument95 pagesGlobal Standards Mapping InitiativesumititproNo ratings yet

- Financial Technology: Fragmented For Financial Inclusion?Document6 pagesFinancial Technology: Fragmented For Financial Inclusion?Ahmad Aziz Putra PratamaNo ratings yet

- Marketing Strategies of VodafoneA New - Doc RajaDocument105 pagesMarketing Strategies of VodafoneA New - Doc Rajadeepak GuptaNo ratings yet

- IntroductionDocument3 pagesIntroduction3037 Vishva RNo ratings yet

- Impact of E-Commerce On Organization Performance Evidence From Banking Sector of PakistanDocument18 pagesImpact of E-Commerce On Organization Performance Evidence From Banking Sector of PakistanMEHTABAZEEMNo ratings yet

- FIN20016 - Assignment 2Document11 pagesFIN20016 - Assignment 2youuuclassenterpriseNo ratings yet

- Risks 06 00111Document11 pagesRisks 06 00111STRESSEDD -No ratings yet

- Qredo Research PaperDocument21 pagesQredo Research PaperĐào TuấnNo ratings yet

- Enterprise Blockchain Study Cambridge University - 1568990992Document72 pagesEnterprise Blockchain Study Cambridge University - 1568990992Argyris XafisNo ratings yet

- Crowdfunding Using Blockchain by Aishwarya and KavinDocument7 pagesCrowdfunding Using Blockchain by Aishwarya and KavinAishwarya RajeshNo ratings yet

- Chapter 21 Cryptocurrency Article (ACCA + IFRS Box)Document8 pagesChapter 21 Cryptocurrency Article (ACCA + IFRS Box)Kelvin Chu JYNo ratings yet

- Regulatory Sandbox - 270218 FINAL - 2Document18 pagesRegulatory Sandbox - 270218 FINAL - 2Mustafa Al OdailiNo ratings yet

- Technology in Retail LendingDocument31 pagesTechnology in Retail LendingRedSunNo ratings yet

- Block Chain Architecture DesignDocument18 pagesBlock Chain Architecture DesignMayank GuptaNo ratings yet

- Financial Inclusion - Does Digital Financial Literacy Matter For Women Entrepreneurs PDFDocument20 pagesFinancial Inclusion - Does Digital Financial Literacy Matter For Women Entrepreneurs PDFSucatta IDNo ratings yet

- Blockchain in Logistics and Supply Chain: A Lean Approach For Designing Real-World Use CasesDocument11 pagesBlockchain in Logistics and Supply Chain: A Lean Approach For Designing Real-World Use CasesTalha ImtiazNo ratings yet

- Documentation ICO 06092018Document15 pagesDocumentation ICO 06092018hugelinNo ratings yet

- Report 2022 The Enablers of Open Banking Open Finance and Open DataDocument195 pagesReport 2022 The Enablers of Open Banking Open Finance and Open DatasebiroperNo ratings yet

- Comparison of Cryptocurrency Regulations in Kenya & Other JurisdictionsDocument23 pagesComparison of Cryptocurrency Regulations in Kenya & Other JurisdictionsSancho SanchezNo ratings yet

- Fintech Glossary 2nd EditionDocument197 pagesFintech Glossary 2nd EditionalmohannadNo ratings yet

- Blockchain Distributed Ledger Technologies For Biomedical and Health Care ApplicationsDocument10 pagesBlockchain Distributed Ledger Technologies For Biomedical and Health Care ApplicationsMatias CaporaleNo ratings yet

- Blockchain Technology in The Banking SectorDocument2 pagesBlockchain Technology in The Banking Sectorvaralakshmi aNo ratings yet

- Cryptocurrencies and Market Efficiency: Investigate The Implications of Cryptocurrencies On Traditional Financial Markets and Their EfficiencyDocument16 pagesCryptocurrencies and Market Efficiency: Investigate The Implications of Cryptocurrencies On Traditional Financial Markets and Their EfficiencyInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Inspirer L'algérie Des Fintechs Cas de La TurquieDocument80 pagesInspirer L'algérie Des Fintechs Cas de La TurquieMehdi ZentarNo ratings yet

- 1 - Fintech Development and Bank Risk Taking in ChinaDocument23 pages1 - Fintech Development and Bank Risk Taking in ChinaErvanFachrudinNo ratings yet

- 312 Money and BankingDocument3 pages312 Money and BankingKims Pak0% (1)

- Nift 2.0Document2 pagesNift 2.0axeclu100% (1)

- Cryptocurrency IEEE (Abstract)Document1 pageCryptocurrency IEEE (Abstract)Sharath Kumar KR100% (2)

- Future Finance InfographicDocument4 pagesFuture Finance InfographicAssetNo ratings yet

- Seminar Report BlockDocument18 pagesSeminar Report BlockFieldartNo ratings yet

- Final Report Project 374: Security Investigation of Selected Blockchain ApplicationsDocument47 pagesFinal Report Project 374: Security Investigation of Selected Blockchain ApplicationsDominic SummersNo ratings yet

- Strategi Optimalisasi Digitalisasi Produk Perbankan Pada Bank Syariah IndonesiaDocument20 pagesStrategi Optimalisasi Digitalisasi Produk Perbankan Pada Bank Syariah IndonesiaAbdul AzizNo ratings yet

- Priority Banking FinalDocument42 pagesPriority Banking Finalneelam rawatNo ratings yet

- Smart Stamp DutyDocument12 pagesSmart Stamp DutyYudhis YudhistiraNo ratings yet

- SocGen - Blockchain, Crypto and Banks 011221v2Document49 pagesSocGen - Blockchain, Crypto and Banks 011221v2irvinkuanNo ratings yet

- Blockchain Business Models A Complete Guide - 2019 EditionFrom EverandBlockchain Business Models A Complete Guide - 2019 EditionNo ratings yet

- Seminar: Angela C Webster, Evi V Nagler, Rachael L Morton, Philip MassonDocument15 pagesSeminar: Angela C Webster, Evi V Nagler, Rachael L Morton, Philip MassonMaría José GalvisNo ratings yet

- Group 7 - SpecialtopicDocument26 pagesGroup 7 - SpecialtopickylamaeduyorNo ratings yet

- 1Document12 pages1Justin MangubatNo ratings yet

- Year 2 Daily Lesson Plans: Skills Pedagogy (Strategy/Activity)Document5 pagesYear 2 Daily Lesson Plans: Skills Pedagogy (Strategy/Activity)MAS' AFIEZUL ZARIEN BIN MASNON KPM-GuruNo ratings yet

- HRMT 4429 NA Winter 2024Document2 pagesHRMT 4429 NA Winter 2024kaursatveer324No ratings yet

- Mendoza V PNPDocument2 pagesMendoza V PNPFrancis Nealle RicasioNo ratings yet

- The Blessing of Sending Salawat - Shaykh Faid Mohammed SaidDocument6 pagesThe Blessing of Sending Salawat - Shaykh Faid Mohammed SaidThe Nur OfficialNo ratings yet

- Experimental Study of Tensile Testing of Metallic Materials in Engineering MechanicsDocument4 pagesExperimental Study of Tensile Testing of Metallic Materials in Engineering Mechanics中华人民共和国People Republic of ChinaNo ratings yet

- Wisest and Brighest of MankindDocument13 pagesWisest and Brighest of MankindFaisal JahangeerNo ratings yet

- College of Teacher Education: Cebu Normal UniversityDocument1 pageCollege of Teacher Education: Cebu Normal UniversityJohn Lloyd TinapayNo ratings yet

- 10 1016@j Chemosphere 2019 05 233Document8 pages10 1016@j Chemosphere 2019 05 233Azzeddine MustaphaNo ratings yet

- Mengukur KompetensiDocument7 pagesMengukur KompetensiMufti Nur'ainiNo ratings yet

- CH 11 LeadershipDocument32 pagesCH 11 LeadershipshopeewithdaisyNo ratings yet

- Grade 6 Science - Space - Lesson Plan PDFDocument4 pagesGrade 6 Science - Space - Lesson Plan PDFEric Bois50% (2)

- Guerrilla Filmmaking 101 PDFDocument51 pagesGuerrilla Filmmaking 101 PDFደጀን ኣባባ67% (3)

- Salmon Primer BGNDDocument2 pagesSalmon Primer BGNDchem_is_tryNo ratings yet

- Factors Affecting Valuation of SharesDocument6 pagesFactors Affecting Valuation of SharesSneha ChavanNo ratings yet

- Markiting Analysis Report of GetzDocument8 pagesMarkiting Analysis Report of GetzMahad aslam QureshiNo ratings yet

- Having Learned The Materials in Session 5Document2 pagesHaving Learned The Materials in Session 5Resta Dwi Apni100% (4)

- Hinton - Women and Slash Fan FictionDocument22 pagesHinton - Women and Slash Fan FictionZofia BaranNo ratings yet

- Mathematics 6 - First SemesterDocument57 pagesMathematics 6 - First Semester세드릭No ratings yet

- CRM ProjectDocument95 pagesCRM Projectramangurdas100% (8)

- Barber 1997Document32 pagesBarber 1997helmiselvia82No ratings yet

- Simulation, Consciousness and ExistenceDocument11 pagesSimulation, Consciousness and ExistenceWeo RefNo ratings yet

- Eagleeye Msrcamera QuicktipsDocument2 pagesEagleeye Msrcamera QuicktipsMiguel Ángel de PablosNo ratings yet

- Corporate Liquidation QuizDocument4 pagesCorporate Liquidation QuizMarinoNo ratings yet

- OssecDocument38 pagesOssecMehdi LaarifNo ratings yet

- Stability of Curved Bridges During ConstructionDocument129 pagesStability of Curved Bridges During ConstructionAri PranantaNo ratings yet