Lim V CA

Lim V CA

Download as pdf or txt

You might also like

- Macro Final Cheat SheetDocument2 pagesMacro Final Cheat SheetChristine Son100% (1)

- Marcos II Vs CA Case DigestDocument2 pagesMarcos II Vs CA Case Digestlucky javellana100% (3)

- Republic v. KerDocument2 pagesRepublic v. KerAira Madrid100% (1)

- 10 FS Analysis Sample Exam Discussion KEYDocument10 pages10 FS Analysis Sample Exam Discussion KEYrav danoNo ratings yet

- Gitman IM ch08 PDFDocument17 pagesGitman IM ch08 PDFdmnque pileNo ratings yet

- Question Bank VatDocument14 pagesQuestion Bank VatLeonard Cañamo90% (10)

- Lim Vs CaDocument11 pagesLim Vs CaAnonymous VtsflLix1No ratings yet

- Republic v. Lim de YuDocument6 pagesRepublic v. Lim de YuDaLe AparejadoNo ratings yet

- Lim SR Vs CADocument15 pagesLim SR Vs CAPia Christine BungubungNo ratings yet

- Lim, Sr. vs. Court of Appeals, 190 SCRA 616, G.R. Nos. 48134-37. October 18, 1990Document4 pagesLim, Sr. vs. Court of Appeals, 190 SCRA 616, G.R. Nos. 48134-37. October 18, 1990Pilyang SweetNo ratings yet

- Taxation Law LimvsCADocument3 pagesTaxation Law LimvsCAJohn Benedict TigsonNo ratings yet

- Lim Vs CADocument2 pagesLim Vs CAestvanguardiaNo ratings yet

- 6 Arches Vs BellosilloDocument6 pages6 Arches Vs BellosilloJeanne CalalinNo ratings yet

- Tax 2 Remedies Digests KoDocument29 pagesTax 2 Remedies Digests KoMary Ann LeeNo ratings yet

- Republic Vs Ker & CompanyDocument17 pagesRepublic Vs Ker & Companycode4saleNo ratings yet

- 1 Cebu Portland Vs CTADocument5 pages1 Cebu Portland Vs CTAvendetta scrubNo ratings yet

- Petitioner Vs Vs Respondent: Third DivisionDocument9 pagesPetitioner Vs Vs Respondent: Third DivisionPatricia Nicole TabundaNo ratings yet

- Compiled Tax DigestsDocument12 pagesCompiled Tax DigestsDominique PobeNo ratings yet

- Republic v. Lim de Yu: DOCTRINE/S: For The Ten-Year Period ofDocument3 pagesRepublic v. Lim de Yu: DOCTRINE/S: For The Ten-Year Period ofDaLe AparejadoNo ratings yet

- Ferdinand E. Marcos II vs. Court of Appeals (G.R. No. 120880, June 5, 1997)Document3 pagesFerdinand E. Marcos II vs. Court of Appeals (G.R. No. 120880, June 5, 1997)Pia Vanessa CeballosNo ratings yet

- 1) Cebu Portland Cement v. CTA, L-29059, 15 Dec 1987, 156 SCRA 535 (Lifeblood of The Government)Document9 pages1) Cebu Portland Cement v. CTA, L-29059, 15 Dec 1987, 156 SCRA 535 (Lifeblood of The Government)Guiller C. MagsumbolNo ratings yet

- CIR vs. Philippine Global CommunicationsDocument28 pagesCIR vs. Philippine Global CommunicationsChristle CorpuzNo ratings yet

- Supreme Court: Office of The Solicitor General For Petitioner. Ross, Selph and Carrascoso For Respondent CompanyDocument9 pagesSupreme Court: Office of The Solicitor General For Petitioner. Ross, Selph and Carrascoso For Respondent CompanyRaziele RanesesNo ratings yet

- 258-Republic v. Hizon G.R. No. 130430 December 13, 1999Document4 pages258-Republic v. Hizon G.R. No. 130430 December 13, 1999Jopan SJNo ratings yet

- Commissioner of Lnternal Revenue vs. Cebu Portlandcement Company 156 Scra 535, December 15, 1987Document50 pagesCommissioner of Lnternal Revenue vs. Cebu Portlandcement Company 156 Scra 535, December 15, 1987AnatheaAcabanNo ratings yet

- Office of The Solicitor General and A.H. Garces For Plaintiff-Appellant. Tongco, Tongco and de Leon For Defendant-AppelleeDocument5 pagesOffice of The Solicitor General and A.H. Garces For Plaintiff-Appellant. Tongco, Tongco and de Leon For Defendant-AppelleeRandee CeasarNo ratings yet

- CIR V BF. GoodrichDocument7 pagesCIR V BF. GoodrichMary Ann Celeste LeuterioNo ratings yet

- Palanca Vs CirDocument5 pagesPalanca Vs Ciryelina_kuranNo ratings yet

- Tax Remedies DigestsDocument19 pagesTax Remedies DigestsHiedi SugamotoNo ratings yet

- Tax Case 1 To 30Document21 pagesTax Case 1 To 30Ma RaNo ratings yet

- CIR V Cebu Portland Cement, GR No L-29059, 156 SCRA 535Document9 pagesCIR V Cebu Portland Cement, GR No L-29059, 156 SCRA 535Sheena Reyes-BellenNo ratings yet

- 4 Bonifacio Sy Po Vs CTA GR No. 81446 PDFDocument10 pages4 Bonifacio Sy Po Vs CTA GR No. 81446 PDFJeanne CalalinNo ratings yet

- 4 Bonifacio Sy Po Vs CTA GR No. 81446Document10 pages4 Bonifacio Sy Po Vs CTA GR No. 81446Jeanne CalalinNo ratings yet

- Second Division: Syllabus SyllabusDocument7 pagesSecond Division: Syllabus SyllabusVMNo ratings yet

- 007 CIR Vs BASFDocument7 pages007 CIR Vs BASFEric TamayoNo ratings yet

- Tax II DigestsDocument62 pagesTax II DigestsWilfredo Guerrero IIINo ratings yet

- Cta 3D Co 00989 M 2023apr27 VTCDocument8 pagesCta 3D Co 00989 M 2023apr27 VTCFirenze PHNo ratings yet

- CIR v. Philippine Global CommunicationsDocument23 pagesCIR v. Philippine Global CommunicationsDaLe AparejadoNo ratings yet

- Republic vs. Marsman Development CompanyDocument14 pagesRepublic vs. Marsman Development CompanyFbarrsNo ratings yet

- G.R. Nos. L-48134-37 Whatever Is ItDocument6 pagesG.R. Nos. L-48134-37 Whatever Is ItPrhylleNo ratings yet

- Cir v. Basf CoatingDocument8 pagesCir v. Basf CoatingPaulineNo ratings yet

- Republic VS KerDocument5 pagesRepublic VS KerJudith Eliscia YacobNo ratings yet

- Estate Tax DDocument13 pagesEstate Tax DRalph Christian UsonNo ratings yet

- 5 Republic Vs Salud HizonDocument11 pages5 Republic Vs Salud HizonJeanne CalalinNo ratings yet

- TAX Principles Digest Batch 1Document10 pagesTAX Principles Digest Batch 1Victor SarmientoNo ratings yet

- G.R. No. L-23912 March 15, 1968 Commissioner of Internal Revenue, Petitioner, Jose ConcepcionDocument4 pagesG.R. No. L-23912 March 15, 1968 Commissioner of Internal Revenue, Petitioner, Jose ConcepcionANGIE BERNALNo ratings yet

- RMC 101-90Document2 pagesRMC 101-90Latasha Phillips100% (2)

- CIR Vs BFDocument1 pageCIR Vs BFNikhim CroneNo ratings yet

- G.R. No. 198677 November 26, 2014 Commissioner of Internal Revenue, Petitioner, BASF COATING + INKS PHILS., INC., RespondentDocument10 pagesG.R. No. 198677 November 26, 2014 Commissioner of Internal Revenue, Petitioner, BASF COATING + INKS PHILS., INC., RespondentMikkaEllaAnclaNo ratings yet

- 262-Republic v. Acebedo G.R. No. L-20477 March 29, 1968Document2 pages262-Republic v. Acebedo G.R. No. L-20477 March 29, 1968Jopan SJNo ratings yet

- Republic V KerDocument3 pagesRepublic V KerCinNo ratings yet

- Ungab, Accused " and To Restrain The Respondent Judge FromDocument3 pagesUngab, Accused " and To Restrain The Respondent Judge FromDon YcayNo ratings yet

- Cir V Basf CoatingDocument18 pagesCir V Basf CoatingJuris PasionNo ratings yet

- Prescription - Sayson Statute of Limitations: ConstructionDocument6 pagesPrescription - Sayson Statute of Limitations: ConstructionAnne Fatima PilayreNo ratings yet

- Today Is Sunday, March 17, 2019: Melquiades P. de Leon For Plaintiff-AppellantDocument3 pagesToday Is Sunday, March 17, 2019: Melquiades P. de Leon For Plaintiff-AppellantEunice SerneoNo ratings yet

- Tax 2Document20 pagesTax 2MiaNo ratings yet

- 10-CIR v. B.F. Goodrich Phils., Inc. G.R. No. 104171 February 4, 1999Document5 pages10-CIR v. B.F. Goodrich Phils., Inc. G.R. No. 104171 February 4, 1999Jopan SJNo ratings yet

- 10 Consolidated Mines, Inc. Vs Commissioner of Internal RevenueDocument21 pages10 Consolidated Mines, Inc. Vs Commissioner of Internal RevenueHey it's RayaNo ratings yet

- Republic of The PH vs. Lim de Yu DGDocument1 pageRepublic of The PH vs. Lim de Yu DGKimberly RamosNo ratings yet

- Domingo v. Garlitos - G.R. No. L-18994Document2 pagesDomingo v. Garlitos - G.R. No. L-18994Ash SatoshiNo ratings yet

- G.R. No. L-28782 - Auyong Hian vs. Court of Tax AppealsDocument20 pagesG.R. No. L-28782 - Auyong Hian vs. Court of Tax AppealsLarssen IbarraNo ratings yet

- Real Estate: How to Find Auctions, Foreclosures, and the Cheapest PropertiesFrom EverandReal Estate: How to Find Auctions, Foreclosures, and the Cheapest PropertiesNo ratings yet

- A Caution to the Directors of the East-India Company With Regard to their Making the Midsummer Dividend of Five Per Cent.From EverandA Caution to the Directors of the East-India Company With Regard to their Making the Midsummer Dividend of Five Per Cent.No ratings yet

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- Teleological School of Thought - FINALDocument15 pagesTeleological School of Thought - FINALKaye Miranda LaurenteNo ratings yet

- Functional SchoolDocument11 pagesFunctional SchoolKaye Miranda LaurenteNo ratings yet

- Petition For Notarial CommissionDocument11 pagesPetition For Notarial CommissionKaye Miranda LaurenteNo ratings yet

- The Insular Life Assurance Company, Ltd. vs. KhuDocument24 pagesThe Insular Life Assurance Company, Ltd. vs. KhuKaye Miranda LaurenteNo ratings yet

- The Insular Life Assurance Company, Ltd. vs. KhuDocument24 pagesThe Insular Life Assurance Company, Ltd. vs. KhuKaye Miranda LaurenteNo ratings yet

- Phil. Consolidated Coconut Industries V CIR (70 SCRA 22) PDFDocument15 pagesPhil. Consolidated Coconut Industries V CIR (70 SCRA 22) PDFKaye Miranda LaurenteNo ratings yet

- Phil. Consolidated Coconut Industries V CIR (70 SCRA 22)Document15 pagesPhil. Consolidated Coconut Industries V CIR (70 SCRA 22)Kaye Miranda LaurenteNo ratings yet

- TORTS Case DigestDocument14 pagesTORTS Case DigestKaye Miranda LaurenteNo ratings yet

- Lopez V LiboroDocument9 pagesLopez V LiboroKaye Miranda LaurenteNo ratings yet

- Succession - Morales vs. OlondrizDocument1 pageSuccession - Morales vs. OlondrizKaye Miranda LaurenteNo ratings yet

- Balais Mabanag V Register of Deeds of Quezon City (GR No 153142 March 29, 2010)Document16 pagesBalais Mabanag V Register of Deeds of Quezon City (GR No 153142 March 29, 2010)Kaye Miranda LaurenteNo ratings yet

- Balais Mabanag V Register of Deeds of Quezon City (GR No 153142 March 29, 2010)Document30 pagesBalais Mabanag V Register of Deeds of Quezon City (GR No 153142 March 29, 2010)Kaye Miranda LaurenteNo ratings yet

- In the Matter of the Testate Estate of Edward e. Christensen, Deceased. Adolfo c. Aznar, Executor and Lucy Christensen, Heir of the Deceased, Executor and Heir-Appellees, Vs.helen Christensen Garcia, Oppositor-Appellant.Document286 pagesIn the Matter of the Testate Estate of Edward e. Christensen, Deceased. Adolfo c. Aznar, Executor and Lucy Christensen, Heir of the Deceased, Executor and Heir-Appellees, Vs.helen Christensen Garcia, Oppositor-Appellant.Kaye Miranda LaurenteNo ratings yet

- Succession - Cano vs. Director of LandsDocument1 pageSuccession - Cano vs. Director of LandsKaye Miranda Laurente100% (1)

- Metropolitan Bank and Trust Company, Petitioner, V. CPR Promotions and Marketing, Inc.Document37 pagesMetropolitan Bank and Trust Company, Petitioner, V. CPR Promotions and Marketing, Inc.Kaye Miranda LaurenteNo ratings yet

- Timing Is EverythingDocument11 pagesTiming Is EverythingAxzl RhosNo ratings yet

- Krispy Kreme Case Study - ReymarrHijaraDocument10 pagesKrispy Kreme Case Study - ReymarrHijaraReymarr HijaraNo ratings yet

- Activity 13 - Chapter 31-35 (CFAS)Document4 pagesActivity 13 - Chapter 31-35 (CFAS)Rocel Casilao DomingoNo ratings yet

- Annual Declaration Form (1/8/2008)Document4 pagesAnnual Declaration Form (1/8/2008)ronaldodigmaNo ratings yet

- DocxDocument6 pagesDocxMeshack MathembeNo ratings yet

- Levi Strauss SWOT Analysis-1Document9 pagesLevi Strauss SWOT Analysis-1A.J. GambleNo ratings yet

- Tax Evasion CHPT 1-5Document38 pagesTax Evasion CHPT 1-5KAYODE OLADIPUPO100% (5)

- Periodic and Perpetual Inventory SystemsDocument17 pagesPeriodic and Perpetual Inventory SystemsMichael Brian TorresNo ratings yet

- NEDA ICC Project Evaluation Procedures and Guidelines As of 24 June 2004Document26 pagesNEDA ICC Project Evaluation Procedures and Guidelines As of 24 June 2004rubydelacruz0% (1)

- Corrosion EconomicsDocument9 pagesCorrosion EconomicsEmmanuel EkongNo ratings yet

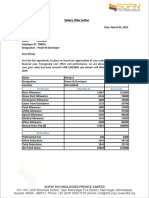

- Salary Hike Letter: Private & ConfidentialDocument2 pagesSalary Hike Letter: Private & Confidentialsandeepreddy2427125No ratings yet

- Salary Detail Earnings Deduction Net PayableDocument1 pageSalary Detail Earnings Deduction Net PayableSheelendra Mangal BhattNo ratings yet

- BPS Midterm Exam KADocument5 pagesBPS Midterm Exam KASheena CalderonNo ratings yet

- Form16.pdf HIRA PDFDocument2 pagesForm16.pdf HIRA PDFSuchitra BakulyNo ratings yet

- Financial Modeling Training PDFDocument8 pagesFinancial Modeling Training PDFVaneet Singh AroraNo ratings yet

- Powerpoint Lectures For Principles of Macroeconomics, 9E by Karl E. Case, Ray C. Fair & Sharon M. OsterDocument36 pagesPowerpoint Lectures For Principles of Macroeconomics, 9E by Karl E. Case, Ray C. Fair & Sharon M. OsterfamytyasNo ratings yet

- Rachita Bba LLB (H) ASSIGNMENT-Differences Between Shares and DebenturesDocument3 pagesRachita Bba LLB (H) ASSIGNMENT-Differences Between Shares and DebenturesRachita WaghadeNo ratings yet

- Budget Statistics 2005 - 2011: Ministry of Finance Republic of IndonesiaDocument16 pagesBudget Statistics 2005 - 2011: Ministry of Finance Republic of IndonesiaSurjadiNo ratings yet

- Corporate Finance Practice Questions MidDocument9 pagesCorporate Finance Practice Questions MidFrasat IqbalNo ratings yet

- Average Score: Texchem Resources (Texchem-Ku)Document11 pagesAverage Score: Texchem Resources (Texchem-Ku)Zhi_Ming_Cheah_8136No ratings yet

- Ratio Analysis of Banking Reports (HBL, UBL, MCB Etc)Document42 pagesRatio Analysis of Banking Reports (HBL, UBL, MCB Etc)Fahad Khan80% (20)

- CooperativeDocument51 pagesCooperativeLuzviminda Chavez100% (1)

- COPA Process StepDocument9 pagesCOPA Process StepTrinath Gujari100% (1)

- CSU Bakersfield FRSDocument79 pagesCSU Bakersfield FRSMatt BrownNo ratings yet

- 1.inroduction: Working Capital Management Refers To A Company's ManagerialDocument7 pages1.inroduction: Working Capital Management Refers To A Company's Managerialmaa digitalxeroxNo ratings yet

- Punjab National Bank: Reg.:-Pbf Under Kisan Gold SchemeDocument3 pagesPunjab National Bank: Reg.:-Pbf Under Kisan Gold SchemeROHIT YADAVNo ratings yet