May 2017 Advanced Financial Accounting & Reporting Final Pre-Board

May 2017 Advanced Financial Accounting & Reporting Final Pre-Board

Download as docx, pdf, or txt

At a glance

Powered by AI

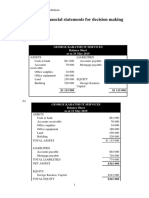

The document discusses accounting problems related to partnerships, corporations, and cost accounting.

2,542 and 1,550 shares

Closing of partnership books

You might also like

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2024 Edition)From EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2024 Edition)Rating: 4.5 out of 5 stars4.5/5 (6)

- 1 1 4-Partnership-LiquidationDocument7 pages1 1 4-Partnership-LiquidationCundangan, Denzel Erick S.67% (3)

- TAX - First Preboard PDFDocument14 pagesTAX - First Preboard PDFPatrick Arazo100% (1)

- Partnership Additional ProbsDocument9 pagesPartnership Additional ProbsJoy LagtoNo ratings yet

- May 2017Document7 pagesMay 2017Patrick Arazo0% (1)

- DynatronicsDocument24 pagesDynatronicsFezi Afesina Haidir90% (10)

- 1 - Case 12 Guna FibresDocument11 pages1 - Case 12 Guna FibresBalaji Palatine100% (1)

- BAC 522 Mid Term ExamDocument9 pagesBAC 522 Mid Term ExamJohn Carlo Cruz0% (1)

- FInals in Advacc 1 1718 - JBinaluyoDocument12 pagesFInals in Advacc 1 1718 - JBinaluyoAveryl Lei Sta.Ana100% (1)

- PAS 7 Reviewer (With Answers)Document5 pagesPAS 7 Reviewer (With Answers)John Ace Madriaga100% (1)

- Answer Key - Exercises - Adjusting EntriesDocument4 pagesAnswer Key - Exercises - Adjusting EntriesAlexa AbaryNo ratings yet

- 9201 - Partnership FormationDocument4 pages9201 - Partnership FormationBrian Dave OrtizNo ratings yet

- PRTC AFAR-1stPB 05.22Document12 pagesPRTC AFAR-1stPB 05.22Ciatto SpotifyNo ratings yet

- 03-Partnership Liquidation Quiz2Document6 pages03-Partnership Liquidation Quiz2JiddahNo ratings yet

- Prelim PartnershipDissolutionSampleProblemDocument12 pagesPrelim PartnershipDissolutionSampleProblemLee SuarezNo ratings yet

- 8901 - Partnership FormationDocument3 pages8901 - Partnership FormationRica Jane Santos Marcelo100% (1)

- Review AfarDocument10 pagesReview AfarJon Dumagil Inocentes, CPANo ratings yet

- Special TransactionsDocument20 pagesSpecial TransactionsapremsNo ratings yet

- 1st Yr Review Questions Parcor 1Document6 pages1st Yr Review Questions Parcor 1Rogen Dane GeneblazaNo ratings yet

- Comprehensive Review QuestionsDocument5 pagesComprehensive Review QuestionsJane Ruby JennieferNo ratings yet

- Testbank For ParnetshipDocument4 pagesTestbank For ParnetshipKristel Joyce LaureñoNo ratings yet

- Partnership FormationDocument3 pagesPartnership FormationAngelica Francine GuanlaoNo ratings yet

- BADVAC2X - MOD 1 Partnership FormationDocument4 pagesBADVAC2X - MOD 1 Partnership FormationAlice WuNo ratings yet

- Advac SemifinalDocument8 pagesAdvac SemifinalDIVINE VILLENANo ratings yet

- AST - PRELIM With AnswersDocument13 pagesAST - PRELIM With Answersjohnmichael.relonNo ratings yet

- ProblemsDocument12 pagesProblemsJoy MarieNo ratings yet

- Afar 2Document92 pagesAfar 2Fathma-Allyzzah AC100% (1)

- Partnership Dissolution and Liquidation HandoutsDocument15 pagesPartnership Dissolution and Liquidation HandoutsBrent DumangengNo ratings yet

- Accounting For Special Transaction 3Document3 pagesAccounting For Special Transaction 3Nicole Gole CruzNo ratings yet

- Ast Discussion 4 - Partnership Liquidation For PrintDocument4 pagesAst Discussion 4 - Partnership Liquidation For PrintCHRISTINE TABULOGNo ratings yet

- ACC110 P1 Q2 AnswersDocument22 pagesACC110 P1 Q2 AnswersJohn Lloyd De GuzmanNo ratings yet

- Partnership Formation Practice SetDocument5 pagesPartnership Formation Practice SetAlexandra CunananNo ratings yet

- Self-Test Partnership and Corporate LiquidationDocument6 pagesSelf-Test Partnership and Corporate Liquidationxara mizpahNo ratings yet

- Accounting 2&3 PretestDocument11 pagesAccounting 2&3 Pretestelumba michaelNo ratings yet

- 1 Partnership AccountingDocument10 pages1 Partnership AccountingMarynelle Labrador SevillaNo ratings yet

- Cpar - Afar - Reviewer - QuizbeeDocument27 pagesCpar - Afar - Reviewer - QuizbeeYvonne MalingNo ratings yet

- ACC 311 Ass#2Document7 pagesACC 311 Ass#2Justine Reine CornicoNo ratings yet

- Cpa Review School of The Philippines ManilaDocument4 pagesCpa Review School of The Philippines Manilaxara mizpahNo ratings yet

- Lyceum First Preboard 2020Document3 pagesLyceum First Preboard 2020Jordan Tobiagon100% (1)

- Acco 30103 Partnership Formation and Operations 04-2022Document3 pagesAcco 30103 Partnership Formation and Operations 04-2022Zyrille Corrine GironNo ratings yet

- Partnership FormationDocument5 pagesPartnership Formationdongabriel820No ratings yet

- Partnership FormationDocument2 pagesPartnership FormationMaria LopezNo ratings yet

- Afar 04Document3 pagesAfar 04yvonneNo ratings yet

- AfarDocument14 pagesAfarPaulo MiguelNo ratings yet

- PARCOR DiscussionDocument6 pagesPARCOR DiscussionSittiNo ratings yet

- 03 - Handout - Partnership DissolutionDocument4 pages03 - Handout - Partnership DissolutionJanysse CalderonNo ratings yet

- AFARDocument41 pagesAFARAlican, JerhamelNo ratings yet

- MID-TERM Adv - Actg. 1 (No Answer)Document10 pagesMID-TERM Adv - Actg. 1 (No Answer)Jose Benzon100% (1)

- ACC - XII - PT - Pre PT AssgDocument4 pagesACC - XII - PT - Pre PT Assgphyxer222No ratings yet

- 12 Accounts Summer Vacation Assignment 2022-23Document15 pages12 Accounts Summer Vacation Assignment 2022-23Ashelle DsouzaNo ratings yet

- Formation of Partnership1Document3 pagesFormation of Partnership1itik meowmeowNo ratings yet

- 9101 - Partnership FormationDocument2 pages9101 - Partnership FormationGo FarNo ratings yet

- Liquidation Assignment PrintingDocument2 pagesLiquidation Assignment Printingranilyn.dacocoNo ratings yet

- 95 - AFAR Preweek LectureDocument18 pages95 - AFAR Preweek Lecturemahisam293No ratings yet

- AST Discussion 3 - PARTNERSHIP DISSOLUTIONDocument5 pagesAST Discussion 3 - PARTNERSHIP DISSOLUTIONCHRISTINE TABULOGNo ratings yet

- P2 Exam ParCor Questionnaire 1Document7 pagesP2 Exam ParCor Questionnaire 1peter paker100% (1)

- AfarDocument6 pagesAfarRolando PasamonteNo ratings yet

- 96 AFAR Preweek SELFTEST 3Document18 pages96 AFAR Preweek SELFTEST 3Gab GabNo ratings yet

- 9301 - Partnership FormationDocument2 pages9301 - Partnership Formationomer 2 gerdNo ratings yet

- INSTRUCTIONS: Select The Best Answer For Each of The Following Attempted. Mark Only One Answer For Each Item On The Answer SheetDocument13 pagesINSTRUCTIONS: Select The Best Answer For Each of The Following Attempted. Mark Only One Answer For Each Item On The Answer SheetMac Ferds100% (2)

- Accounting 2&3 PretestDocument11 pagesAccounting 2&3 Pretestelumba michael0% (1)

- How to Read a Financial Report: Wringing Vital Signs Out of the NumbersFrom EverandHow to Read a Financial Report: Wringing Vital Signs Out of the NumbersNo ratings yet

- Financial Instruments and Institutions: Accounting and Disclosure RulesFrom EverandFinancial Instruments and Institutions: Accounting and Disclosure RulesNo ratings yet

- Make Money With Dividends Investing, With Less Risk And Higher ReturnsFrom EverandMake Money With Dividends Investing, With Less Risk And Higher ReturnsNo ratings yet

- 2018 4083 3rd Evaluation ExamDocument7 pages2018 4083 3rd Evaluation ExamPatrick Arazo0% (1)

- 2018 4083 2nd Evaluation Exam PDFDocument11 pages2018 4083 2nd Evaluation Exam PDFPatrick ArazoNo ratings yet

- October 2010 Business Law & Taxation Final Pre-BoardDocument9 pagesOctober 2010 Business Law & Taxation Final Pre-BoardPatrick ArazoNo ratings yet

- Vacational SchoolDocument11 pagesVacational SchoolPatrick ArazoNo ratings yet

- Practical Accounting Problems IIDocument12 pagesPractical Accounting Problems IIJericho PedragosaNo ratings yet

- 2016 3123Document6 pages2016 3123Patrick ArazoNo ratings yet

- 2018 4073 1st Evaluation ExamDocument9 pages2018 4073 1st Evaluation ExamPatrick ArazoNo ratings yet

- October 2010 Business Law & Taxation Final Pre-BoardDocument11 pagesOctober 2010 Business Law & Taxation Final Pre-BoardPatrick ArazoNo ratings yet

- 4083 EvalDocument11 pages4083 EvalPatrick ArazoNo ratings yet

- CORRECTIONS Ledger ProperDocument37 pagesCORRECTIONS Ledger ProperPatrick ArazoNo ratings yet

- Accounting TreatmentDocument4 pagesAccounting TreatmentPatrick Arazo100% (1)

- FAR Preboard SolutionsDocument4 pagesFAR Preboard SolutionsHikariNo ratings yet

- 2014 3016 Midterm Departmental ExamDocument14 pages2014 3016 Midterm Departmental ExamPatrick ArazoNo ratings yet

- Affidavit of LossDocument3 pagesAffidavit of LossPatrick ArazoNo ratings yet

- 2016 4083 4th Evaluation ExamDocument8 pages2016 4083 4th Evaluation ExamPatrick ArazoNo ratings yet

- Ai EssayDocument1 pageAi EssayPatrick ArazoNo ratings yet

- Estate TaxDocument21 pagesEstate TaxPatrick ArazoNo ratings yet

- How Will AI Change The World We Live In? What Kind of AI Solutions Should Enterprises Invest In?Document1 pageHow Will AI Change The World We Live In? What Kind of AI Solutions Should Enterprises Invest In?Patrick ArazoNo ratings yet

- Taxation 4th Evaluation Exam 2018Document14 pagesTaxation 4th Evaluation Exam 2018Patrick ArazoNo ratings yet

- Supply Chain Management QuestionnaireDocument3 pagesSupply Chain Management QuestionnairePatrick ArazoNo ratings yet

- Practice Question For Midterm Test - FA - 28.03Document4 pagesPractice Question For Midterm Test - FA - 28.03TRANG NGUYỄN THỊ HÀNo ratings yet

- Financial Accounting Q&aDocument4 pagesFinancial Accounting Q&aGlen JavellanaNo ratings yet

- Unit 3: Financial Statement AnalysisDocument24 pagesUnit 3: Financial Statement Analysissujata dawadiNo ratings yet

- GE Hca15 PPT ch01Document205 pagesGE Hca15 PPT ch01jeanneta oliviaNo ratings yet

- Psak 46Document15 pagesPsak 46api-3708783100% (1)

- Ans 3.o Dot1 p6 Fm Sm Jan25 PradhicaDocument23 pagesAns 3.o Dot1 p6 Fm Sm Jan25 Pradhicasripurushothaman.sNo ratings yet

- 2022Q1 Alphabet Earnings ReleaseDocument9 pages2022Q1 Alphabet Earnings ReleaseArthur SzNo ratings yet

- Bukalapak Com TBK Bilingual Q1 2023 FinalDocument175 pagesBukalapak Com TBK Bilingual Q1 2023 FinalTappp - Elevate your networkingNo ratings yet

- Home Office Questions With AnswersDocument9 pagesHome Office Questions With AnswersMichaela QuimsonNo ratings yet

- MABALAZADocument4 pagesMABALAZAMahasa R HajiiNo ratings yet

- ch3 RatioDocument18 pagesch3 RatioEman Samir100% (1)

- Ias 02 InventoryDocument20 pagesIas 02 Inventorydương nguyễn vũ thùyNo ratings yet

- Materi Laporan Keuangan Dan Analisis Rasio Keuangan-LDLDocument33 pagesMateri Laporan Keuangan Dan Analisis Rasio Keuangan-LDLLukmanul HakimNo ratings yet

- CHP 3 Problems Student TemplateDocument28 pagesCHP 3 Problems Student TemplateDarkeningoftheLightNo ratings yet

- Gerrard Construction Co Is An Excavation Contractor The Following SummarizedDocument3 pagesGerrard Construction Co Is An Excavation Contractor The Following SummarizedCharlotteNo ratings yet

- Entrepreneur Chapter 18Document6 pagesEntrepreneur Chapter 18CaladhielNo ratings yet

- Part Two: MatchingDocument2 pagesPart Two: MatchingBereket MamoNo ratings yet

- Partnership Liquidation: Problem MDocument8 pagesPartnership Liquidation: Problem MMiko ArniñoNo ratings yet

- The Accounting CycleDocument3 pagesThe Accounting Cycleliesly buticNo ratings yet

- Consolidated Statement of Financial Position Past QuestionsDocument4 pagesConsolidated Statement of Financial Position Past Questionsa.saymaa.93No ratings yet

- Financial Statement 2162Document126 pagesFinancial Statement 2162YOLA DWI YULANDARINo ratings yet

- Week 4 Solutions PDFDocument4 pagesWeek 4 Solutions PDFchi_nguyen_100No ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 5.0) : How To Use This SpreadsheetDocument49 pagesSafal Niveshak Stock Analysis Excel (Ver. 5.0) : How To Use This Spreadsheetajujk123No ratings yet

- Seat Work 03 - DingcongDocument7 pagesSeat Work 03 - DingcongJheilson S. Dingcong100% (2)

- Level Four Code 3 Answer-1Document7 pagesLevel Four Code 3 Answer-1EdomNo ratings yet

- Eastern Coalfields LimitedDocument9 pagesEastern Coalfields LimitedSyed Shamiul HaqueNo ratings yet