Characteristics of Microeconomics

Characteristics of Microeconomics

Download as docx, pdf, or txt

You might also like

- Goods and Services Purchased Goods and Services Sold: 1 Principles of Economics W/ Taxation and Agrarian ReformDocument20 pagesGoods and Services Purchased Goods and Services Sold: 1 Principles of Economics W/ Taxation and Agrarian ReformBai NiloNo ratings yet

- Chapter 1 Introduction To Microeconomics PDFDocument16 pagesChapter 1 Introduction To Microeconomics PDFMicko Capinpin100% (1)

- 1.introduction To Managerial EconomicsDocument21 pages1.introduction To Managerial EconomicsDiksha Pahuja100% (3)

- Basic Economics With Taxation and Agrarian ReformDocument4 pagesBasic Economics With Taxation and Agrarian ReformLouie Leron72% (25)

- Sample REVIEW OF RELATED LITERATUREDocument4 pagesSample REVIEW OF RELATED LITERATUREexquisite100% (2)

- Module 1 MicroEconomicsDocument29 pagesModule 1 MicroEconomicsjustin vasquez100% (1)

- Marketing Management ReviewerDocument6 pagesMarketing Management ReviewerRozette MacapazNo ratings yet

- Entrepreneurial ProcessDocument12 pagesEntrepreneurial ProcessBalajir Cmy100% (1)

- Lesson 3.6: The Economy's Producing SectorsDocument15 pagesLesson 3.6: The Economy's Producing SectorsRosemarie Matugas100% (1)

- Principles On Economics With Taxation and Agrarian ReformDocument9 pagesPrinciples On Economics With Taxation and Agrarian Reformjunelledequina100% (6)

- Entrepreneurial ManagementDocument23 pagesEntrepreneurial Managementgirish6567% (3)

- Concept of BusinessDocument2 pagesConcept of BusinessHarishYadav100% (3)

- Economics: Chapter 1: Introduction To MicroeconomicsDocument3 pagesEconomics: Chapter 1: Introduction To Microeconomicsfamin87100% (4)

- Qop 56 01 Management ReviewDocument6 pagesQop 56 01 Management ReviewMrityunjoy Banerjee100% (1)

- Fast Meals Less Bills (A Feasibility Study)Document57 pagesFast Meals Less Bills (A Feasibility Study)Carl Justin Ballerta100% (1)

- Itinerary: Additional InformationDocument1 pageItinerary: Additional InformationPravin PatilNo ratings yet

- Characteristics of MicroeconomicsDocument11 pagesCharacteristics of MicroeconomicsMaria JessaNo ratings yet

- Characteristics of MicroecoDocument10 pagesCharacteristics of MicroecoMarrion Dean-Alexis Ragadio RomeroNo ratings yet

- The Case For Free Markets - The Price SystemDocument26 pagesThe Case For Free Markets - The Price Systemspectregaming29100% (1)

- Government (Tax Revenues, Poverty, andDocument8 pagesGovernment (Tax Revenues, Poverty, andMary Leen CustodioNo ratings yet

- The Effectiveness of Using Facebook As A Modern Platform On Conducting Business Group 1Document28 pagesThe Effectiveness of Using Facebook As A Modern Platform On Conducting Business Group 1gianricco75% (4)

- 5 Major Division of EconomicsDocument1 page5 Major Division of Economicsmaria genio100% (1)

- Chapter 7 Pricing and Output Under Pure Competition 2Document43 pagesChapter 7 Pricing and Output Under Pure Competition 2escramosaaravellaNo ratings yet

- Basic Microeconomics (Reviewer)Document3 pagesBasic Microeconomics (Reviewer)Patricia QuiloNo ratings yet

- Perfect Competition - PPTDocument20 pagesPerfect Competition - PPTDyuti Sinha50% (2)

- Applied Economics Chapter 2-3Document6 pagesApplied Economics Chapter 2-3Joan Mae Angot - Villegas100% (1)

- Social Responsibility To ConsumersDocument12 pagesSocial Responsibility To ConsumersJeh Ubaldo0% (1)

- Eastern and Western Perspective of The Self PDFDocument16 pagesEastern and Western Perspective of The Self PDFPrince AntivolaNo ratings yet

- Pros and Cons of Market IntegrationDocument1 pagePros and Cons of Market IntegrationBlank UNKOWNNo ratings yet

- NSTP CWTSDocument30 pagesNSTP CWTSRondoy Desuasido GulfoNo ratings yet

- The Philippine EconomyDocument4 pagesThe Philippine EconomyVillaruz Shereen MaeNo ratings yet

- 1.1 Introduction To MicroeconomicsDocument20 pages1.1 Introduction To MicroeconomicsLeo Marbeda Feigenbaum100% (1)

- Law, Order and War in Non-State SocietiesDocument22 pagesLaw, Order and War in Non-State Societiesk6225857No ratings yet

- Chapter 4 National Income AcctgDocument49 pagesChapter 4 National Income AcctgReynaldo Flores Jr.No ratings yet

- BM Module 1Document14 pagesBM Module 1Sharon Cadampog Mananguite100% (1)

- Lesson 2 - Entrepreneurial Character Traits, Skills, and COmpetenciesDocument40 pagesLesson 2 - Entrepreneurial Character Traits, Skills, and COmpetenciesWappy Wepwep100% (1)

- Lesson 3 - THEORIES OF ENTREPRENEURSHIPDocument38 pagesLesson 3 - THEORIES OF ENTREPRENEURSHIPTeacher Flo100% (3)

- The Salient Features and Theories On EntrepreneurshipDocument20 pagesThe Salient Features and Theories On EntrepreneurshipArbhe Rose AñascoNo ratings yet

- Philosophers Believe That Self Has Different PersDocument5 pagesPhilosophers Believe That Self Has Different PersPrincess GinezNo ratings yet

- Polytechnic University of The Philippines: Don Fabian, Commonwealth Quezon City PhilippinesDocument22 pagesPolytechnic University of The Philippines: Don Fabian, Commonwealth Quezon City PhilippinesMajessa BongueNo ratings yet

- A Case Study On UnemploymentDocument10 pagesA Case Study On UnemploymentAizelle Mynina Pitargue80% (5)

- Marcel Mauss: Lesson 2:Socio-Anthro View of SelfDocument7 pagesMarcel Mauss: Lesson 2:Socio-Anthro View of SelfMa. Kristina Señorita HayagNo ratings yet

- Economic ResourcesDocument12 pagesEconomic ResourcesMarianne Hilario0% (2)

- Microeconomics Module 1Document29 pagesMicroeconomics Module 1Rezia Rose Pagdilao100% (3)

- ABM G12 Business Ethics - Fairness, Justice, Accountability and TransparencyDocument1 pageABM G12 Business Ethics - Fairness, Justice, Accountability and TransparencymauuiNo ratings yet

- Asian RegionalismDocument15 pagesAsian RegionalismAngelica Sambo100% (2)

- Philippine Rice Shortage EssayDocument2 pagesPhilippine Rice Shortage EssayMoguriNo ratings yet

- Business Proposal The Ginger CandyDocument9 pagesBusiness Proposal The Ginger CandyPerri YussNo ratings yet

- Microeconomic Theory and Practice: San Beda University AY 21-22Document63 pagesMicroeconomic Theory and Practice: San Beda University AY 21-22Sergio ConjugalNo ratings yet

- Chapter 1: Concepts of Entrepreneurship: I. The EntrepreneurDocument5 pagesChapter 1: Concepts of Entrepreneurship: I. The EntrepreneurChristian Rivera100% (1)

- CASE StudyDocument26 pagesCASE Studyjerah may100% (1)

- Entrepreneurship Education in The Philippines: Aida L. Velasco, D.B.ADocument14 pagesEntrepreneurship Education in The Philippines: Aida L. Velasco, D.B.AkarimNo ratings yet

- Characteristics of MicroeconomicsDocument8 pagesCharacteristics of Microeconomicsjustine100% (1)

- Lesson 2 APPLIED ECONOMICSDocument30 pagesLesson 2 APPLIED ECONOMICSJoey Aranduque100% (1)

- North South GapDocument33 pagesNorth South GapAllen TorioNo ratings yet

- Contemporary Economic Issues Affecting The Filipino EntrepreneurDocument5 pagesContemporary Economic Issues Affecting The Filipino Entrepreneurkaren bulauan100% (1)

- Basic Economic Tools in Managerial EconomicsDocument11 pagesBasic Economic Tools in Managerial EconomicsDileep Kumar Raju100% (2)

- Applied Economics ReviewerDocument6 pagesApplied Economics ReviewerAevan Joseph100% (1)

- Towards A Resilient and Inclusive Financial SectorDocument36 pagesTowards A Resilient and Inclusive Financial SectorSpare ManNo ratings yet

- Chapter 4 Theory of Consumption Summary 1Document4 pagesChapter 4 Theory of Consumption Summary 1Alyssa Joy De BelenNo ratings yet

- Timeline of Cheerleading: First Pep ClubDocument9 pagesTimeline of Cheerleading: First Pep ClubSachie MosquiteNo ratings yet

- 2.2 Price Theory and Economic TheoryDocument30 pages2.2 Price Theory and Economic TheoryLeo Marbeda Feigenbaum100% (2)

- Microeconomics (From Greek Prefix Mikro-Meaning "Small" + Economics) Is A BranchDocument4 pagesMicroeconomics (From Greek Prefix Mikro-Meaning "Small" + Economics) Is A BranchNithya RajaramNo ratings yet

- Preview ISO+TS+22317-2021Document7 pagesPreview ISO+TS+22317-2021IsaiahNo ratings yet

- Real Estate ManagementDocument3 pagesReal Estate ManagementRubina HannureNo ratings yet

- DocumentDocument3 pagesDocumentTidene BaynoNo ratings yet

- Cbc-5Dmr: Assay Values and Expected RangesDocument4 pagesCbc-5Dmr: Assay Values and Expected Rangesrose_almonteNo ratings yet

- ABB Balance SheetDocument6 pagesABB Balance SheetJyoti Prakash KhataiNo ratings yet

- Corporate Presentation - BEPLDocument38 pagesCorporate Presentation - BEPLRamadugula Rama Subrahmanya VenkateswararaoNo ratings yet

- Passport Magazine: Joshua David & Robert Hammond, Co-Founders of Friends of The High LineDocument3 pagesPassport Magazine: Joshua David & Robert Hammond, Co-Founders of Friends of The High LineroodelooNo ratings yet

- Mid-Semester Examinations Project Management MBAWPDocument5 pagesMid-Semester Examinations Project Management MBAWPSujit ThiruNo ratings yet

- Contractualization Rodrigo On The Issue Contractualization: For Filipino Workers"Document4 pagesContractualization Rodrigo On The Issue Contractualization: For Filipino Workers"JackNo ratings yet

- The Scope of Corporate FinanceDocument2 pagesThe Scope of Corporate FinanceooitzandyooNo ratings yet

- Worldclass Preventative & Predictive Maintenance: ND RDDocument10 pagesWorldclass Preventative & Predictive Maintenance: ND RDAgung PriambodhoNo ratings yet

- Designing Organizational Structure: Specialization and CoordinationDocument47 pagesDesigning Organizational Structure: Specialization and CoordinationMas JackNo ratings yet

- Introduction To MarketingDocument17 pagesIntroduction To MarketingajaynagreNo ratings yet

- Tax 1 AnsDocument1 pageTax 1 AnsEMMANUEL JASON CASASNo ratings yet

- Mpu 2222-PampletDocument8 pagesMpu 2222-PampletNur SyarafanaNo ratings yet

- CF YpphDocument9 pagesCF YpphashxerNo ratings yet

- Tube Lines Accepted OfferDocument4 pagesTube Lines Accepted OfferRMT UnionNo ratings yet

- Ch04 Problem Solving Is BSDocument30 pagesCh04 Problem Solving Is BShjhjhjNo ratings yet

- Curriculum Vitae: Career ObjectiveDocument3 pagesCurriculum Vitae: Career ObjectiveArif KhanNo ratings yet

- Prtintversion Vol 13 No 681 PDFDocument64 pagesPrtintversion Vol 13 No 681 PDFamare_abebaw100% (1)

- Brochure Regn Form NRDC Priority Partner RegistrationDocument6 pagesBrochure Regn Form NRDC Priority Partner RegistrationSaurav yadavNo ratings yet

- Fact ListDocument3 pagesFact Listvictorhugomenasalazar229No ratings yet

- Dos Donts TreasurerDocument9 pagesDos Donts Treasurergrexter0% (1)

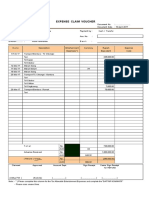

- Expense Claim Voucher: PT Trakindo UtamaDocument1 pageExpense Claim Voucher: PT Trakindo UtamaadityapwNo ratings yet

- CavinkareDocument22 pagesCavinkarepravin pawar100% (1)

- Longyuan-Arrk (Macao) Pte LTD V Show and Tell Productions Pte LTD and Another Suit (2013) SGHC 160Document84 pagesLongyuan-Arrk (Macao) Pte LTD V Show and Tell Productions Pte LTD and Another Suit (2013) SGHC 160EH ChngNo ratings yet

- Nikiforuk - PowerTrip - Ralph Klein Promised Deregulating ElectricityDocument9 pagesNikiforuk - PowerTrip - Ralph Klein Promised Deregulating ElectricityBarret WeberNo ratings yet