Working Capital Desicion: Unit - Iv

Working Capital Desicion: Unit - Iv

Download as doc, pdf, or txt

You might also like

- The Open Banking StandardDocument148 pagesThe Open Banking StandardOpen Data Institute95% (21)

- Mba-III-Advanced Financial Management (14mbafm304) - NotesDocument48 pagesMba-III-Advanced Financial Management (14mbafm304) - NotesSyeda GazalaNo ratings yet

- Budgeting: What Is A Budget?Document16 pagesBudgeting: What Is A Budget?Cecilia Mfene Sekubuwane100% (1)

- Working Capital Management AssignmentDocument12 pagesWorking Capital Management AssignmentDiana B BashantNo ratings yet

- Chapter 2 Job Analysis and Job DesignDocument27 pagesChapter 2 Job Analysis and Job DesignIzza Nabilah AbasNo ratings yet

- WCM at Bevcon PVT LTD.Document65 pagesWCM at Bevcon PVT LTD.moula nawazNo ratings yet

- 0927 ShannonDocument30 pages0927 Shannonstephane95% (21)

- 9706 Accounting: MARK SCHEME For The May/June 2008 Question PaperDocument8 pages9706 Accounting: MARK SCHEME For The May/June 2008 Question PaperShona MaheshwariNo ratings yet

- Principle Marketin-1Document102 pagesPrinciple Marketin-1bikilahussen100% (1)

- Research Methodology MBADocument3 pagesResearch Methodology MBAYogesh KumarNo ratings yet

- Research Methodology MbaDocument99 pagesResearch Methodology MbaAjin RkNo ratings yet

- Accounting: Scope of Practice of AccountancyDocument6 pagesAccounting: Scope of Practice of AccountancyKl HumiwatNo ratings yet

- Cost Accounting - Course Study Guide. (Repaired)Document9 pagesCost Accounting - Course Study Guide. (Repaired)syed Hassan100% (1)

- Operations Strategy and Competitiveness PDFDocument20 pagesOperations Strategy and Competitiveness PDFGUnndiNo ratings yet

- KCA University Bachelor of Commerce PRINCIPLES of MANAGEMENTDocument2 pagesKCA University Bachelor of Commerce PRINCIPLES of MANAGEMENTCalvince Ouma100% (1)

- Operations Management ComprehensiveDocument9 pagesOperations Management ComprehensiveashishNo ratings yet

- Working Capital ManagementDocument59 pagesWorking Capital ManagementjuanferchoNo ratings yet

- Q#2 Psalm 23 Jabez PrayerDocument5 pagesQ#2 Psalm 23 Jabez PrayerHarsey Joy PunzalanNo ratings yet

- MGT06 TQM - Syllabus - 2016-2017 (2ND)Document8 pagesMGT06 TQM - Syllabus - 2016-2017 (2ND)Christelle De Los CientosNo ratings yet

- Financial Analysis Project - Rite Aid CorporationDocument15 pagesFinancial Analysis Project - Rite Aid Corporationapi-302665852No ratings yet

- Operations Management - Chapter 4Document6 pagesOperations Management - Chapter 4David Van De FliertNo ratings yet

- Financial Accounting Vs Managerial AccountingDocument1 pageFinancial Accounting Vs Managerial AccountingHafizUmarArshadNo ratings yet

- Chapter 16 - Lean Systems Answers To Questions, Problems, and Case Problems Answers To QuestionsDocument13 pagesChapter 16 - Lean Systems Answers To Questions, Problems, and Case Problems Answers To QuestionsomkarNo ratings yet

- Chapter 7 ForecastingDocument32 pagesChapter 7 ForecastingRaghuram Seshabhattar100% (1)

- MGT 498 Chapter 10 AnswersDocument47 pagesMGT 498 Chapter 10 Answersjewelz15overNo ratings yet

- Case 1 Farmers RestaurantDocument63 pagesCase 1 Farmers RestaurantMendel Dela CruzNo ratings yet

- Principle and Strategies in TQMDocument60 pagesPrinciple and Strategies in TQMmarkedsingle75% (4)

- The Nature and Purpose of Financial Management - NotesDocument2 pagesThe Nature and Purpose of Financial Management - NotesWsxQaz100% (4)

- GAP Management Managing Interest Rate Risk at Banks and ThriftsDocument18 pagesGAP Management Managing Interest Rate Risk at Banks and ThriftsrunawayyyNo ratings yet

- Lecture Note 1 - Global Sourcing - FTDocument21 pagesLecture Note 1 - Global Sourcing - FTTc. Mohd Nazrul100% (1)

- Management Control Systems: Question IM 16.1 IntermediateDocument12 pagesManagement Control Systems: Question IM 16.1 IntermediateLegogie Moses AnoghenaNo ratings yet

- Presentation Week 1 - BSBHRM513Document10 pagesPresentation Week 1 - BSBHRM513Xavar XanNo ratings yet

- Module 3 - PPT - Operation Management TQMDocument57 pagesModule 3 - PPT - Operation Management TQMMacsNo ratings yet

- Summary of Differential Analysis, The Key To Decision MakingDocument6 pagesSummary of Differential Analysis, The Key To Decision Makingali akbarNo ratings yet

- Managerial Accounting STANDARD PDFDocument0 pagesManagerial Accounting STANDARD PDFMichael YuNo ratings yet

- Short-Term Financial PlanningDocument64 pagesShort-Term Financial PlanningSheila Mae LaputNo ratings yet

- Performance Appraisal Method AssignmentDocument10 pagesPerformance Appraisal Method Assignmentjami_rockstars3707No ratings yet

- POM SyllabusDocument2 pagesPOM SyllabusMehul JainNo ratings yet

- Mg1351 Principles of Management 1Document19 pagesMg1351 Principles of Management 1s.reegan100% (1)

- Chapter-Two: Competitiveness, Strategies, and Productivity in OperationsDocument63 pagesChapter-Two: Competitiveness, Strategies, and Productivity in OperationsChernet AyenewNo ratings yet

- Environmental ScanningDocument20 pagesEnvironmental ScanningnakhoNo ratings yet

- Started On Tuesday, 28 September 2021, 10:45 AM State Finished Completed On Tuesday, 28 September 2021, 10:49 AM Time Taken 3 Mins 48 Secs Grade 15.00 Out of 15.00 (100%)Document6 pagesStarted On Tuesday, 28 September 2021, 10:45 AM State Finished Completed On Tuesday, 28 September 2021, 10:49 AM Time Taken 3 Mins 48 Secs Grade 15.00 Out of 15.00 (100%)Ronalyn C. Carias100% (1)

- Chapter 10Document20 pagesChapter 10RosyLeeNo ratings yet

- Avon Case SolutionDocument6 pagesAvon Case SolutionAmal TomNo ratings yet

- Budgetring ControlDocument16 pagesBudgetring ControlNamrata NeopaneyNo ratings yet

- 1 An Overview of Financial ManagementDocument14 pages1 An Overview of Financial ManagementSadia AfrinNo ratings yet

- Group 5: Cornejo, Sue Cleo Pedroza, Pia Loraine Rodrigo, Karla Angela Therese Yutico, Roxane Mae Imperial, SheenaDocument12 pagesGroup 5: Cornejo, Sue Cleo Pedroza, Pia Loraine Rodrigo, Karla Angela Therese Yutico, Roxane Mae Imperial, SheenaVenn Bacus RabadonNo ratings yet

- Questionnaire & Form DesignDocument41 pagesQuestionnaire & Form DesignAjithreddy BasireddyNo ratings yet

- Project Report - Working Capital Management Working Capital - Meaning of Working CapitalDocument6 pagesProject Report - Working Capital Management Working Capital - Meaning of Working CapitalAmartya Bodh TripathiNo ratings yet

- Working Capital Kesoram FinanceDocument56 pagesWorking Capital Kesoram FinanceRamana GNo ratings yet

- WORKING CAPITAL Kesoram FinanceDocument48 pagesWORKING CAPITAL Kesoram Financerajinikanth dasiNo ratings yet

- Project PDFDocument74 pagesProject PDFAniketNo ratings yet

- Working Capital Black BookDocument35 pagesWorking Capital Black Bookomprakash shindeNo ratings yet

- Shyam Prakash Project - Feb 12 2022Document71 pagesShyam Prakash Project - Feb 12 2022Sairam DasariNo ratings yet

- Introduction To Working CapitalDocument17 pagesIntroduction To Working Capitalaejaz ahmedNo ratings yet

- Working Capital ManagementDocument26 pagesWorking Capital ManagementAjay Singh PanwarNo ratings yet

- WDCCB Working CapitalDocument53 pagesWDCCB Working Capital2562923No ratings yet

- Working Capital - Meaning of Working Capital: All Project ReportsDocument22 pagesWorking Capital - Meaning of Working Capital: All Project Reportspriyanka yadavNo ratings yet

- Project WCMDocument36 pagesProject WCMmohammedabdullah2162No ratings yet

- Chapter - 1: Introduction of Working CapitalDocument39 pagesChapter - 1: Introduction of Working CapitalSamayra royNo ratings yet

- Working Capital Imp3Document100 pagesWorking Capital Imp3SamNo ratings yet

- Project Report - Working Capital ManagementDocument45 pagesProject Report - Working Capital ManagementSumit mukherjeeNo ratings yet

- Working Capital Management in Vardhman-Final ProjectDocument84 pagesWorking Capital Management in Vardhman-Final ProjectRaj Kumar100% (3)

- Entrepreneurship Unit 05Document5 pagesEntrepreneurship Unit 05SURAJ KUMARNo ratings yet

- AK Mock BA 141 1st LEDocument3 pagesAK Mock BA 141 1st LEElmer BonakNo ratings yet

- Wholesale Individual Application Form: Delivery InstructionsDocument1 pageWholesale Individual Application Form: Delivery InstructionsJun ArranguezNo ratings yet

- Financial Ratio QuizDocument1 pageFinancial Ratio QuizMylene SantiagoNo ratings yet

- Burhan CVDocument2 pagesBurhan CVMustafa LimdiwalaNo ratings yet

- Smith & Associates, LLCDocument5 pagesSmith & Associates, LLCMario PuglisiNo ratings yet

- Final Math 2UDocument21 pagesFinal Math 2Uarav.zadNo ratings yet

- Invoice ToDocument1 pageInvoice ToTester Simplicity For BusinessNo ratings yet

- Reviwer 2ndQ APDocument3 pagesReviwer 2ndQ APMarxzia Alexzia Geraldez OonNo ratings yet

- Robert Earl Smith: ActivitiesDocument4 pagesRobert Earl Smith: ActivitiesTrevorNo ratings yet

- Performance Appraisal Maha Cement 222Document100 pagesPerformance Appraisal Maha Cement 222kartik100% (1)

- Financial and Managerial Accounting MCQDocument36 pagesFinancial and Managerial Accounting MCQdevansh1221100% (1)

- Nike Inc. Case StudyDocument17 pagesNike Inc. Case StudyAbeer KhodariNo ratings yet

- Rationale of The Study: Chapter: OneDocument22 pagesRationale of The Study: Chapter: OneHumayun KabirNo ratings yet

- Chapter 4 - Income From House PropertyDocument5 pagesChapter 4 - Income From House PropertyADARSH MISHRANo ratings yet

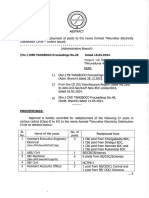

- BP No.29 (AB) Dated 15.03.2024Document3 pagesBP No.29 (AB) Dated 15.03.2024kannanchammyNo ratings yet

- Arnerich V DHC Assets LTD (2021) NZCA 225Document58 pagesArnerich V DHC Assets LTD (2021) NZCA 225PNo ratings yet

- Virgin Mobiles Pricing StrategyDocument5 pagesVirgin Mobiles Pricing StrategyMicah ThomasNo ratings yet

- Generally Accepted Accounting Principles (GAAP)Document20 pagesGenerally Accepted Accounting Principles (GAAP)Vijayanta PawaseNo ratings yet

- Sole Proprietorship Final AccountsDocument23 pagesSole Proprietorship Final Accountsjaiccha420No ratings yet

- Oct 23Document3 pagesOct 23Muneeb ShahzadNo ratings yet

- Accounting and Its Relationship To Engineering EconomyDocument53 pagesAccounting and Its Relationship To Engineering Economymacmolles2380% (5)

- Gamboa Vs Teves Case DigestDocument2 pagesGamboa Vs Teves Case DigestNatalie Anne Bambico MercadoNo ratings yet

- Chapter - 4 Intermediate Term FinancingDocument9 pagesChapter - 4 Intermediate Term FinancingmuzgunniNo ratings yet

- CFAS Reviewer PrelimDocument11 pagesCFAS Reviewer PrelimAlleah Mae Del RosarioNo ratings yet

- Agency Relationship and Creative AccountingDocument16 pagesAgency Relationship and Creative AccountingshomudrokothaNo ratings yet

- MD Abdus SalamDocument15 pagesMD Abdus SalamAkshay PophaleNo ratings yet