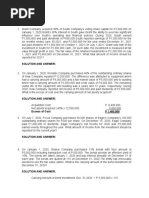

Cfas Nca & NCL

Cfas Nca & NCL

Download as docx, pdf, or txt

You might also like

- 2023 CFA L2 Book 2 FRA - CI-2Document100 pages2023 CFA L2 Book 2 FRA - CI-2PR100% (2)

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2024 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2024 Edition)Rating: 5 out of 5 stars5/5 (1)

- Far Theory Test BankDocument15 pagesFar Theory Test BankKimberly Etulle Celona100% (1)

- Solutions (Quiz1 &2)Document8 pagesSolutions (Quiz1 &2)Aaron Arellano50% (2)

- Diagnostic Test: Fundamental of Accounting Business & Management 1Document3 pagesDiagnostic Test: Fundamental of Accounting Business & Management 1Dindin Oromedlav Lorica75% (4)

- FAR Theory Quiz 1Document7 pagesFAR Theory Quiz 1Ednalyn CruzNo ratings yet

- Practice Multiple Choice Questions For First Test PDFDocument10 pagesPractice Multiple Choice Questions For First Test PDFBringinthehypeNo ratings yet

- Sanicomodule 2Document11 pagesSanicomodule 2Luigi Enderez BalucanNo ratings yet

- Cash and Cash Equi Theories and ProblemsDocument29 pagesCash and Cash Equi Theories and ProblemsIris Mnemosyne100% (5)

- Test Bank Advanced Accounting Part 2 Millan PDFDocument433 pagesTest Bank Advanced Accounting Part 2 Millan PDFAmie Jane MirandaNo ratings yet

- Accounting For Price Level ChangesDocument5 pagesAccounting For Price Level ChangesIndu Gupta100% (2)

- Current AssetsDocument53 pagesCurrent AssetsIris Mnemosyne100% (1)

- FAR Questions With AnswersDocument43 pagesFAR Questions With AnswersBryan AdrianoNo ratings yet

- Statement of Financial PositionDocument7 pagesStatement of Financial PositionshengNo ratings yet

- Finals Exam - IaDocument8 pagesFinals Exam - IaJennifer Rasonabe100% (1)

- Intacc PpeDocument32 pagesIntacc PpeIris MnemosyneNo ratings yet

- ALL SubjectsDocument11 pagesALL SubjectsMJ YaconNo ratings yet

- Corporate Reporting 100 QSDocument21 pagesCorporate Reporting 100 QSSabarishNo ratings yet

- CFAS Semestral ProjectDocument21 pagesCFAS Semestral ProjectCASSANDRANo ratings yet

- University of CalicutDocument24 pagesUniversity of CalicutArchanaNo ratings yet

- FA (1-3 W Answers)Document17 pagesFA (1-3 W Answers)imsana minatozakiNo ratings yet

- Theory of Accounts (No Ak)Document10 pagesTheory of Accounts (No Ak)Irish Joy AlaskaNo ratings yet

- Mock ExamDocument22 pagesMock ExamAlyana DubloisNo ratings yet

- Corporate Accounting MCQ With PDFDocument8 pagesCorporate Accounting MCQ With PDFMukesh yadavNo ratings yet

- GEN 010 P1 ExamDocument20 pagesGEN 010 P1 ExamJulian Adam PagalNo ratings yet

- Cpa Review School of The Philippines ManilaDocument4 pagesCpa Review School of The Philippines ManilaAljur SalamedaNo ratings yet

- Cfas - Midterm Exam GuideDocument9 pagesCfas - Midterm Exam GuideAngel Madelene BernardoNo ratings yet

- Analysis of Financial Statements Solved MCQs (Set-1)Document6 pagesAnalysis of Financial Statements Solved MCQs (Set-1)VenkataRamana IkkurthiNo ratings yet

- Financial AccountingDocument5 pagesFinancial AccountingMelissa Kayla ManiulitNo ratings yet

- ACC 111 Review MaterialDocument8 pagesACC 111 Review MaterialMikaela G. ParasNo ratings yet

- Acc3 Intermediate Acctg 1aDocument9 pagesAcc3 Intermediate Acctg 1aKaren UmaliNo ratings yet

- Pre BoardDocument7 pagesPre BoardJose Dula II50% (2)

- Amoni Edome Coc Sample Exam-Level LLLDocument13 pagesAmoni Edome Coc Sample Exam-Level LLLAmoni EdomeNo ratings yet

- 1234449Document19 pages1234449Jade MarkNo ratings yet

- pdf (1)Document35 pagespdf (1)dexter daysoNo ratings yet

- Mock PreboardDocument12 pagesMock PreboardArvin John MasuelaNo ratings yet

- Midterm ExaminationDocument10 pagesMidterm ExaminationJo KeNo ratings yet

- Practice Questions For Conceptual FrameworkDocument6 pagesPractice Questions For Conceptual Frameworkaxel BNo ratings yet

- AC503 - Finals Reviewer 2Document10 pagesAC503 - Finals Reviewer 2Ashley Levy San Pedro100% (1)

- Auditing.: A. B. C. DDocument12 pagesAuditing.: A. B. C. DbiniamNo ratings yet

- IntAcc 1 Reviewer - Module 2 (Theories)Document8 pagesIntAcc 1 Reviewer - Module 2 (Theories)Lizette Janiya SumantingNo ratings yet

- Quiz 3Document4 pagesQuiz 3denniseescobido07No ratings yet

- Basic Accounting ReviewerDocument4 pagesBasic Accounting ReviewerColeen Del RosarioNo ratings yet

- Practice Multiple Choice Questions For First Test PDFDocument10 pagesPractice Multiple Choice Questions For First Test PDFBringinthehypeNo ratings yet

- Final Exam CDocument12 pagesFinal Exam Cnhorelajne03No ratings yet

- Polytechnic University of The Philippines College of AccountancyDocument11 pagesPolytechnic University of The Philippines College of AccountancyRonel CacheroNo ratings yet

- BSA 2105 Carandang CFAS Sem ProjectDocument16 pagesBSA 2105 Carandang CFAS Sem Project21-55654No ratings yet

- Pcu - Cfas - 1ST Quiz - Midterm - 2ND Sem 2019-2020Document4 pagesPcu - Cfas - 1ST Quiz - Midterm - 2ND Sem 2019-2020Anie MartinezNo ratings yet

- CFASDocument7 pagesCFASchoigyu031301No ratings yet

- Analysis of Financial Statements Set 1Document6 pagesAnalysis of Financial Statements Set 1Arpita DagliaNo ratings yet

- The Assets That Can Be Converted Into Cash Within A Short Period (1 Year or Less) Are Known AsDocument17 pagesThe Assets That Can Be Converted Into Cash Within A Short Period (1 Year or Less) Are Known As4- Desiree FuaNo ratings yet

- Document 4Document5 pagesDocument 4Bal QisNo ratings yet

- Bcom I Fa 103 MCQSDocument11 pagesBcom I Fa 103 MCQSTushar GuptaNo ratings yet

- 120 General Accounting Principles MCQs - WatermarkedDocument25 pages120 General Accounting Principles MCQs - WatermarkedNamrata SrivastavaNo ratings yet

- AE 16 Prelims TheoriesDocument7 pagesAE 16 Prelims TheoriesJheally SeirNo ratings yet

- Review Questions - New Conceptual Framework - Summer 2015Document7 pagesReview Questions - New Conceptual Framework - Summer 2015Roen Jasper EviaNo ratings yet

- Chapter 5Document16 pagesChapter 5desi permataNo ratings yet

- Toa 2Document16 pagesToa 2Ray Jhon OrtizNo ratings yet

- fabm1_tq_q3Document6 pagesfabm1_tq_q3Shirly AvesNo ratings yet

- FAR - First Preboard ExaminationsDocument13 pagesFAR - First Preboard ExaminationsMonique PendijitoNo ratings yet

- 211 EO Finals REVIEWERDocument9 pages211 EO Finals REVIEWERmarites yuNo ratings yet

- Jan 24 sem 1 Management AccountingDocument5 pagesJan 24 sem 1 Management Accountingmiltondsouza29No ratings yet

- Ateneo de Zamboanga University: Final Examination Finacc ODocument14 pagesAteneo de Zamboanga University: Final Examination Finacc OMelanie JadeNo ratings yet

- Questionnaire: Act112 - Intermediate Accounting IDocument20 pagesQuestionnaire: Act112 - Intermediate Accounting IMichaelNo ratings yet

- CFAS Consolidated Mock Exam 2Document3 pagesCFAS Consolidated Mock Exam 2josevgomez1234567No ratings yet

- FPQP Practice Question Workbook: 1,000 Comprehensive Practice Questions (2024 Edition)From EverandFPQP Practice Question Workbook: 1,000 Comprehensive Practice Questions (2024 Edition)No ratings yet

- Receivables ProblemsDocument13 pagesReceivables ProblemsIris Mnemosyne0% (1)

- Coneptual Frameworks and Accounting Standards Probs and TheoriesDocument17 pagesConeptual Frameworks and Accounting Standards Probs and TheoriesIris MnemosyneNo ratings yet

- Conceptual Frameworks and Accounting Standard - ProblemsDocument3 pagesConceptual Frameworks and Accounting Standard - ProblemsIris Mnemosyne100% (1)

- Receivables TheoriesDocument8 pagesReceivables TheoriesIris MnemosyneNo ratings yet

- Financing Equity ProblemsDocument14 pagesFinancing Equity ProblemsIris MnemosyneNo ratings yet

- Financing Equity TheoriesDocument7 pagesFinancing Equity TheoriesIris MnemosyneNo ratings yet

- Investments (Theories)Document41 pagesInvestments (Theories)Iris Mnemosyne100% (1)

- Income Statement - ProblemsDocument19 pagesIncome Statement - ProblemsIris Mnemosyne50% (2)

- Cfas Cash Flow Theories and ProblemsDocument30 pagesCfas Cash Flow Theories and ProblemsIris MnemosyneNo ratings yet

- Inventories - ProblemDocument17 pagesInventories - ProblemIris Mnemosyne100% (4)

- Reviewer CFASDocument4 pagesReviewer CFASChinNo ratings yet

- Sellfa 2Document21 pagesSellfa 2ashokawijesingheNo ratings yet

- Cost and Management Accouting PDFDocument472 pagesCost and Management Accouting PDFMaxwell chanda100% (1)

- Accounting Concepts Principles WPS OfficeDocument43 pagesAccounting Concepts Principles WPS OfficeMa Vifie TigalloNo ratings yet

- ACFrOgDZ7Mb1kEnd0SWTabZ8VTNHoE2URvhT8DhCJGcSZcROTUArMhbEM93WzGm2kI1BwFxq0 x1Pf-HKvzBDZ5dplRt2Zs - hEPqbAFI0Fc3z2m0dtyYdxz8KJGo8dJYsrypTjAUs2oYzuZ - TDDocument38 pagesACFrOgDZ7Mb1kEnd0SWTabZ8VTNHoE2URvhT8DhCJGcSZcROTUArMhbEM93WzGm2kI1BwFxq0 x1Pf-HKvzBDZ5dplRt2Zs - hEPqbAFI0Fc3z2m0dtyYdxz8KJGo8dJYsrypTjAUs2oYzuZ - TDTwish BarriosNo ratings yet

- Old Pfrs For SmesDocument12 pagesOld Pfrs For SmesDennis VelasquezNo ratings yet

- Comparison IFRS VASDocument43 pagesComparison IFRS VAStieuquan42100% (3)

- FACR MCQS Theory AllDocument46 pagesFACR MCQS Theory Alluroojfatima21299No ratings yet

- CHAPTER 1.an Introduction To Accounting TheoryDocument15 pagesCHAPTER 1.an Introduction To Accounting TheoryIsmi Fadhliati100% (2)

- 2018 Financial Statements 11Document64 pages2018 Financial Statements 11Jamilene PandanNo ratings yet

- Cae05-Chapter 1 Current LiabilitiesDocument15 pagesCae05-Chapter 1 Current LiabilitiesSteffany RoqueNo ratings yet

- Chapter 10-Investments in Noncurrent Operating Assets-AcquisitionDocument34 pagesChapter 10-Investments in Noncurrent Operating Assets-AcquisitionYukiNo ratings yet

- This Study Resource Was: FAR Ocampo/Cabarles/Soliman/Ocampo Quiz No. 3 Set A OCTOBER 2019Document3 pagesThis Study Resource Was: FAR Ocampo/Cabarles/Soliman/Ocampo Quiz No. 3 Set A OCTOBER 2019ChjxksjsgskNo ratings yet

- Canvass Ia QuizDocument32 pagesCanvass Ia QuizLhowellaAquinoNo ratings yet

- Chapter 22 Current LiabilitiesDocument17 pagesChapter 22 Current Liabilitiesnoryn40% (5)

- BNU Question Paper QuestionsDocument9 pagesBNU Question Paper QuestionsAdith MNo ratings yet

- DQ 4Document3 pagesDQ 4Jazzen MartinezNo ratings yet

- Branch AccountsDocument13 pagesBranch Accountstanuj_baruNo ratings yet

- Accounting Concepts and PrinciplesDocument25 pagesAccounting Concepts and PrinciplesSook LyeNo ratings yet

- Toaz - Info Investment Property PRDocument6 pagesToaz - Info Investment Property PRJulian CheezeNo ratings yet

- ACC 100 FE Set 2Document5 pagesACC 100 FE Set 2Helaena Ruvie Quitoras PallayaNo ratings yet

- This Study Resource Was: InvestmentsDocument9 pagesThis Study Resource Was: InvestmentsMs VampireNo ratings yet

- IFRS9 Final Handout CFAPv2Document69 pagesIFRS9 Final Handout CFAPv2rafid aliNo ratings yet

- Accounting StandardsDocument105 pagesAccounting Standardskrishnakantpachouri026No ratings yet

- ABM 11 - FABM 1 - Q3 - W2 - Module 2-v2Document15 pagesABM 11 - FABM 1 - Q3 - W2 - Module 2-v2Erra Peñaflorida - PedroNo ratings yet