No. L-7271 (Case2)

No. L-7271 (Case2)

Download as pdf or txt

You might also like

- Negotiable Instruments CasesDocument27 pagesNegotiable Instruments CasesJanice PolinarNo ratings yet

- Philippine National Bank, Plaintiff-Appellant, vs. Jose C. ZuluetaDocument46 pagesPhilippine National Bank, Plaintiff-Appellant, vs. Jose C. ZuluetaLavin AguilarNo ratings yet

- 5 G.R. No. L-7271 PNB V ZuluetaDocument6 pages5 G.R. No. L-7271 PNB V ZuluetaApril Eloise M. BorjaNo ratings yet

- PNB V ZuluetaDocument10 pagesPNB V ZuluetaThomas EdisonNo ratings yet

- PNB V Zulueta 2Document9 pagesPNB V Zulueta 2april750% (1)

- PNB Vs ZuluetaDocument4 pagesPNB Vs ZuluetaRhona MarasiganNo ratings yet

- PNB vs. Zulueta - Republic vs. Equitable BankDocument2 pagesPNB vs. Zulueta - Republic vs. Equitable BankLoubert BartolomeNo ratings yet

- 01 Belman Inc. v. Central Bank (104 Phil. 877)Document4 pages01 Belman Inc. v. Central Bank (104 Phil. 877)Mary LeandaNo ratings yet

- Belman Compania Vs Central Bank of The Phil 2Document1 pageBelman Compania Vs Central Bank of The Phil 2eunice demaclidNo ratings yet

- NIL CasesDocument51 pagesNIL CasesLope Nam-iNo ratings yet

- Civ 2 Cases - Contracts Part 1Document45 pagesCiv 2 Cases - Contracts Part 1Rolan Jeff Amoloza LancionNo ratings yet

- Kauffman vs. PNB, G.R. No. 16454, September 29, 1921Document3 pagesKauffman vs. PNB, G.R. No. 16454, September 29, 1921Calma, Anwar, G.No ratings yet

- Supreme Court: InsolventDocument14 pagesSupreme Court: InsolventpatrixiaNo ratings yet

- Yuliongsiu v. PNB G.R. No. L 19227Document3 pagesYuliongsiu v. PNB G.R. No. L 19227Lexa L. DotyalNo ratings yet

- Supreme Court: Roman J. Lacson For Appellant. Ross and Lawrence For AppelleeDocument40 pagesSupreme Court: Roman J. Lacson For Appellant. Ross and Lawrence For AppelleeColeen Navarro-RasmussenNo ratings yet

- NEGO Assignment #3Document53 pagesNEGO Assignment #3Ýel ÄcedilloNo ratings yet

- Digests 212-225 Non-Impairment ClauseDocument18 pagesDigests 212-225 Non-Impairment ClauseJane100% (1)

- Supreme CourtDocument46 pagesSupreme CourtTrisha AmorantoNo ratings yet

- PledgeDocument10 pagesPledgeirishNo ratings yet

- Clements vs. Nolting 42 Phil. 702Document4 pagesClements vs. Nolting 42 Phil. 702angelica balatong100% (1)

- 1 - Philippine Education Company Vs SorianoDocument4 pages1 - Philippine Education Company Vs SorianoKeej DalonosNo ratings yet

- Bank of Nova Scotia v. San Miguel, 214 F.2d 102, 1st Cir. (1954)Document6 pagesBank of Nova Scotia v. San Miguel, 214 F.2d 102, 1st Cir. (1954)Scribd Government DocsNo ratings yet

- Assignment AdminDocument17 pagesAssignment AdminAngel SosaNo ratings yet

- Digest Kauffman VS PNBDocument3 pagesDigest Kauffman VS PNBcodearcher27100% (1)

- Associated Bank vs. CA (G.R. No. 123793 June 29, 1998) - 6Document9 pagesAssociated Bank vs. CA (G.R. No. 123793 June 29, 1998) - 6Amir Nazri KaibingNo ratings yet

- Javellana Vs LimDocument4 pagesJavellana Vs LimCLark BarcelonNo ratings yet

- Torts CasesDocument94 pagesTorts CasesPrincess MelodyNo ratings yet

- Inchausti V YuloDocument17 pagesInchausti V YuloAlvin Lorenzo V. Ogena100% (1)

- Week 4 Case Digest - MANLUCOB, Lyra Kaye B.Document6 pagesWeek 4 Case Digest - MANLUCOB, Lyra Kaye B.LYRA KAYE MANLUCOBNo ratings yet

- Hidalgo v. Heirs of TuazonDocument3 pagesHidalgo v. Heirs of TuazonKooking JubiloNo ratings yet

- GR L-49494 Ponce Vs CADocument5 pagesGR L-49494 Ponce Vs CAJessie AncogNo ratings yet

- International Finance Corp. v. ImperialDocument4 pagesInternational Finance Corp. v. ImperialJerald Oliver MacabayaNo ratings yet

- 0 Collated Case Digests 100 160Document51 pages0 Collated Case Digests 100 160maebeldelapenaNo ratings yet

- Kalalo V LuzDocument2 pagesKalalo V LuzVian O.No ratings yet

- Case DigestDocument15 pagesCase DigestReyniere AloNo ratings yet

- Victor Yam - Yek Sun Lent vs. CADocument4 pagesVictor Yam - Yek Sun Lent vs. CAPatrisha AlmasaNo ratings yet

- Yam V CADocument9 pagesYam V CAslashNo ratings yet

- Colinares & Veloso v. Court of Appeals, G.R. No. 90828, 5 September 2000, 339 SCRA 609Document7 pagesColinares & Veloso v. Court of Appeals, G.R. No. 90828, 5 September 2000, 339 SCRA 609JMae MagatNo ratings yet

- CasesDocument24 pagesCasesTrisha AmorantoNo ratings yet

- Full Text Compiliation EvidenceDocument95 pagesFull Text Compiliation EvidenceBec Bec BecNo ratings yet

- Soriano vs. Ubat, G.R. No. L-11633, January 31, 1961.Document2 pagesSoriano vs. Ubat, G.R. No. L-11633, January 31, 1961.Lourdes LorenNo ratings yet

- L. D. Lockwood For Appellant. Camus and Delgado For AppelleeDocument26 pagesL. D. Lockwood For Appellant. Camus and Delgado For AppelleeDiane Cabral CalangiNo ratings yet

- CasesDocument24 pagesCasesTrisha AmorantoNo ratings yet

- Ayala y Compania vs. ArvachaDocument2 pagesAyala y Compania vs. ArvachaMay RMNo ratings yet

- Cases For IPL For Nov27 (Trust Receipts Law Cases)Document16 pagesCases For IPL For Nov27 (Trust Receipts Law Cases)Bruce WayneNo ratings yet

- Inciong Vs Ca Full TextDocument4 pagesInciong Vs Ca Full TextThea Jane MerinNo ratings yet

- Supreme Court: Plaintiff On Their Respective Due DatesDocument35 pagesSupreme Court: Plaintiff On Their Respective Due DatesJuris PoetNo ratings yet

- Yam v. CA (1999)Document2 pagesYam v. CA (1999)Fides DamascoNo ratings yet

- Plaintiff-Appellant Vs Vs Defendant-Appellant Ross, Selph, Carrascoso & Janda Del N L. Gonzalez Claro M. RectoDocument11 pagesPlaintiff-Appellant Vs Vs Defendant-Appellant Ross, Selph, Carrascoso & Janda Del N L. Gonzalez Claro M. RectoHannah MedNo ratings yet

- Credit PledgeDocument26 pagesCredit PledgeGel de GraciaNo ratings yet

- Ponce de Leon v. Santiago Syjuco Inc.20170309-898-1ifyr63Document15 pagesPonce de Leon v. Santiago Syjuco Inc.20170309-898-1ifyr63Roseanne MateoNo ratings yet

- Credit YpliungsuiDocument6 pagesCredit YpliungsuiJoseph Adrian ToqueroNo ratings yet

- Case DigestDocument22 pagesCase DigestRichard Palopalo100% (3)

- Memorandum MonterealDocument6 pagesMemorandum MonterealKING ANTHONY MONTEREALNo ratings yet

- Nego Case 1 16Document4 pagesNego Case 1 16Joseph John Santos RonquilloNo ratings yet

- Obli DigestDocument9 pagesObli Digestken adams100% (1)

- JAVELLANA VS LimDocument2 pagesJAVELLANA VS Limcmv mendozaNo ratings yet

- Supreme Court Eminent Domain Case 09-381 Denied Without OpinionFrom EverandSupreme Court Eminent Domain Case 09-381 Denied Without OpinionNo ratings yet

- World Intellectual Property Organization - PilDocument1 pageWorld Intellectual Property Organization - Pilangel robedilloNo ratings yet

- Investment & Dev. Inc vs. CADocument3 pagesInvestment & Dev. Inc vs. CAangel robedilloNo ratings yet

- Katikbak Vs CADocument2 pagesKatikbak Vs CAangel robedilloNo ratings yet

- Law On SalesDocument5 pagesLaw On Salesangel robedilloNo ratings yet

- 2018 Contributions For SSS, Philhealth and Pag-Ibig. A. Philhealth ContributionDocument2 pages2018 Contributions For SSS, Philhealth and Pag-Ibig. A. Philhealth Contributionangel robedilloNo ratings yet

- Slides Explanation: Arah's ScriptDocument2 pagesSlides Explanation: Arah's Scriptangel robedilloNo ratings yet

- No. L-15380 (Casa1)Document2 pagesNo. L-15380 (Casa1)angel robedilloNo ratings yet

- Cases On SalesDocument2 pagesCases On Salesangel robedilloNo ratings yet

- Romulo Machetti vs. Hospicio de San JoseDocument2 pagesRomulo Machetti vs. Hospicio de San Joseangel robedilloNo ratings yet

- Felix Bucton and Nicanora Gabar Bucton, vs. Zosimo Gabar, Josefina Llamoso Gabar and The Honorable Court of AppealsDocument6 pagesFelix Bucton and Nicanora Gabar Bucton, vs. Zosimo Gabar, Josefina Llamoso Gabar and The Honorable Court of Appealsangel robedilloNo ratings yet

- Case Digest: Pantaleon Vs American Express Bank (2010) : FactsDocument2 pagesCase Digest: Pantaleon Vs American Express Bank (2010) : Factsangel robedilloNo ratings yet

- Alejandra Mina Et Al., Plaintiffs, vs. Ruperta Pascual Et Al., DefendantsDocument4 pagesAlejandra Mina Et Al., Plaintiffs, vs. Ruperta Pascual Et Al., Defendantsangel robedilloNo ratings yet

- G.R. No. L-22696Document4 pagesG.R. No. L-22696angel robedilloNo ratings yet

- Muniesa Et Al 2017 Capitalization (9865)Document21 pagesMuniesa Et Al 2017 Capitalization (9865)Camilo Andrés FajardoNo ratings yet

- Free Excel Bookkeeping Template Examples 1.0.017Document30 pagesFree Excel Bookkeeping Template Examples 1.0.017Gabriel LabasanNo ratings yet

- FrankingDocument6 pagesFrankingSuresh SharmaNo ratings yet

- JournalizingDocument29 pagesJournalizingChristian Jake RespicioNo ratings yet

- Jaiib-Ppb-Recollected QuestionsDocument23 pagesJaiib-Ppb-Recollected QuestionsAvijit GhoshNo ratings yet

- Decision Analysis ProblemDocument2 pagesDecision Analysis ProblemGeejayFerrerPaculdo50% (2)

- Pas 1 Pas 2 SeatworkDocument2 pagesPas 1 Pas 2 SeatworkAnime LoverNo ratings yet

- Tmfi Hand NoteDocument64 pagesTmfi Hand NotesaidrajanNo ratings yet

- IBF PPT Lecture # 4 (17102023) (Time-Value-Of-Money)Document38 pagesIBF PPT Lecture # 4 (17102023) (Time-Value-Of-Money)Ala AminNo ratings yet

- CARF No. ASCI. Memet 27 Feb 23Document1 pageCARF No. ASCI. Memet 27 Feb 23Bangun SaranaNo ratings yet

- Corporation CodeDocument54 pagesCorporation Codecomkeeper1100% (3)

- CS Executive Important Questions and TopicsDocument10 pagesCS Executive Important Questions and Topics251105No ratings yet

- Lecture 6 Project Green Bonds. How Green Is Your AssetDocument26 pagesLecture 6 Project Green Bonds. How Green Is Your AssetLouis LagierNo ratings yet

- Lesson 1 Partnership FormationDocument21 pagesLesson 1 Partnership FormationDan Gabrielle SalacNo ratings yet

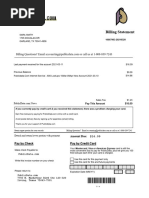

- PD BillingstatementDocument1 pagePD BillingstatementSteven ObryanNo ratings yet

- Absorption Costing and Variable CostingDocument29 pagesAbsorption Costing and Variable Costingmikyla malazzabNo ratings yet

- Rurnover: '.::::"" ':'U ' O, .-Ffhsffihr"ODocument1 pageRurnover: '.::::"" ':'U ' O, .-Ffhsffihr"OCPANo ratings yet

- Top 10 Mistakes (FOREX TRADING)Document12 pagesTop 10 Mistakes (FOREX TRADING)Marie Chris Abragan YañezNo ratings yet

- ICA Housing Profiles of A Movement - Co-Operative Housing Around The World Kopie PDFDocument92 pagesICA Housing Profiles of A Movement - Co-Operative Housing Around The World Kopie PDFFarooq NadeemNo ratings yet

- RL For Credit RiskDocument21 pagesRL For Credit Riskbenhayoun.fatiNo ratings yet

- Lesson 2 - Credit Where Credit Is DueDocument4 pagesLesson 2 - Credit Where Credit Is DueroxanformillezaNo ratings yet

- 1 MCQ PDFDocument37 pages1 MCQ PDFgzsdjyNo ratings yet

- Abacus Real Estate Development V Manila Banking Corp GDocument2 pagesAbacus Real Estate Development V Manila Banking Corp GIhon BaldadoNo ratings yet

- DAY - NULM (DAY - National Urban Livelihoods Mission) 'राष्ट्रीय शहरी आजीविका मिशन'Document9 pagesDAY - NULM (DAY - National Urban Livelihoods Mission) 'राष्ट्रीय शहरी आजीविका मिशन'Abinash MandilwarNo ratings yet

- Bike InsuranceDocument1 pageBike InsuranceTapan BadhaneNo ratings yet

- One Globe Trade AccountDocument5 pagesOne Globe Trade AccountKhushi VarshneyNo ratings yet

- Current Mandeep Dua ResumeDocument3 pagesCurrent Mandeep Dua ResumeMandeep Singh DuaNo ratings yet

- Lesson 2 FM: Money MarketDocument4 pagesLesson 2 FM: Money MarketChristina MalaibaNo ratings yet

- Fundamental Acc-I Chapert 2Document8 pagesFundamental Acc-I Chapert 2tsegaye andualemNo ratings yet

- Bank Management CIA 1Document14 pagesBank Management CIA 125.L Naman Jain.10-DNo ratings yet