ABC Internal Controls PDF

ABC Internal Controls PDF

Download as pdf or txt

You might also like

- End of Chapter Questions and Cases ForDocument102 pagesEnd of Chapter Questions and Cases Fortoton ak14% (7)

- Cincinnatii Southern Railway Investment Advisor Presentation SummaryDocument4 pagesCincinnatii Southern Railway Investment Advisor Presentation SummarySACoolidgeNo ratings yet

- Research Report On General Ledger FraudDocument8 pagesResearch Report On General Ledger FraudAnupam KharatNo ratings yet

- Case 2 (1-4)Document6 pagesCase 2 (1-4)zikril94No ratings yet

- Collections 101Document0 pagesCollections 101pacopepe7750% (2)

- GAs and Oil Processes - WCGW - ControlsDocument10 pagesGAs and Oil Processes - WCGW - Controlsabdullahsaleem91100% (1)

- Auditing and Assurance Services 5th Edition Chapter One Solutions Chapter 1Document9 pagesAuditing and Assurance Services 5th Edition Chapter One Solutions Chapter 1wsvivi100% (3)

- Cry, The Beloved Country Chapter 1-17Document4 pagesCry, The Beloved Country Chapter 1-17api-17546757100% (2)

- Fixed Assets Internal ControlsDocument2 pagesFixed Assets Internal Controlspaiashok100% (1)

- Accounts Payable Sox TestingDocument2 pagesAccounts Payable Sox TestingStephen JonesNo ratings yet

- Audit and Assurance: TestbankDocument12 pagesAudit and Assurance: TestbankBrandonNo ratings yet

- Illustrative Work-Paper Template For Testing ROMM and Performing WalkthroughsDocument35 pagesIllustrative Work-Paper Template For Testing ROMM and Performing Walkthroughsdroidant100% (1)

- Manual Journal Entry Testing: Data Analytics and The Risk of FraudDocument14 pagesManual Journal Entry Testing: Data Analytics and The Risk of FraudArtho KasihNo ratings yet

- Sample Audit ProgramsDocument53 pagesSample Audit ProgramsMinhaj Sikander100% (2)

- Banking Audit Practice Guide II KPMGDocument320 pagesBanking Audit Practice Guide II KPMGInfotomathiNo ratings yet

- Revenue Cycle Audit Answers)Document13 pagesRevenue Cycle Audit Answers)Sulav PoudelNo ratings yet

- The Operational Auditing Handbook: Auditing Business and IT ProcessesFrom EverandThe Operational Auditing Handbook: Auditing Business and IT ProcessesRating: 4.5 out of 5 stars4.5/5 (5)

- AICPA Released Questions AUD 2015 DifficultDocument26 pagesAICPA Released Questions AUD 2015 DifficultTavan ShethNo ratings yet

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsFrom EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsRating: 4.5 out of 5 stars4.5/5 (2)

- Audit Program Budgeting & MISDocument7 pagesAudit Program Budgeting & MISSarang SinghNo ratings yet

- 104 2022 223 PWCDocument23 pages104 2022 223 PWCJason BramwellNo ratings yet

- Audit Risk and MaterialityDocument5 pagesAudit Risk and Materialitycharmsonin12No ratings yet

- AU Locks Auditing Services: Audit Program Batangas Bestfeeds Multipurpose CooperativeDocument5 pagesAU Locks Auditing Services: Audit Program Batangas Bestfeeds Multipurpose CooperativeMirai KuriyamaNo ratings yet

- AP 55 Accrued LiabilitiesDocument5 pagesAP 55 Accrued LiabilitiesMichelle SumayopNo ratings yet

- Account PayableDocument11 pagesAccount PayableShintia Ayu PermataNo ratings yet

- Whole Audit NoteDocument34 pagesWhole Audit NoteBijoy SalahuddinNo ratings yet

- AICPA Newly Released MCQsDocument59 pagesAICPA Newly Released MCQsDaljeet Singh100% (2)

- Related Parties PT 2Document8 pagesRelated Parties PT 2Caterina De LucaNo ratings yet

- Chapter01 - Overview of The Audit ProcessDocument3 pagesChapter01 - Overview of The Audit ProcessCristy Estrella0% (1)

- Case Audit Planning Risk AssessmentDocument10 pagesCase Audit Planning Risk AssessmentХалиун ТунгалагNo ratings yet

- Auditing and Assurance ServicesDocument8 pagesAuditing and Assurance ServicesHelena Thomas75% (4)

- Statement of Financial Position (Balance Sheet) Assertions: Government Accounting & AuditingDocument3 pagesStatement of Financial Position (Balance Sheet) Assertions: Government Accounting & AuditingCarmelo CuyosNo ratings yet

- Internal Audit Procedures ManualDocument11 pagesInternal Audit Procedures ManualLeizza Ni Gui DulaNo ratings yet

- Chapter 7 Test For Forensic Accounting & Fraud Examination, 1 e Mary-Jo Kranacher ISBN-10 047043774X Wiley 2010Document17 pagesChapter 7 Test For Forensic Accounting & Fraud Examination, 1 e Mary-Jo Kranacher ISBN-10 047043774X Wiley 2010Shoniqua JohnsonNo ratings yet

- How Do Different Levels of Control Risk in The RevDocument3 pagesHow Do Different Levels of Control Risk in The RevHenry L BanaagNo ratings yet

- Audit of Cash On Hand and in BankDocument2 pagesAudit of Cash On Hand and in Bankdidiaen100% (1)

- Name of Auditee Nature of Audit Audit Period Audit Start Date End Date Audit StaffDocument3 pagesName of Auditee Nature of Audit Audit Period Audit Start Date End Date Audit StaffAmitmil MbbsNo ratings yet

- 2011 AICPA Business QuestionsDocument45 pages2011 AICPA Business Questionsjklein2588100% (2)

- Auditing Lecture Notes 04172022Document16 pagesAuditing Lecture Notes 04172022Abegail Cadacio100% (2)

- LECTURE 7 - Chapter 10 Auditing The Revenue ProcessDocument35 pagesLECTURE 7 - Chapter 10 Auditing The Revenue Processamy100% (1)

- 2017 AICPA Newly Released Questions-AuditingDocument62 pages2017 AICPA Newly Released Questions-AuditingEvita Faith LeongNo ratings yet

- All Scrutiny of Record For Audit PurposesDocument4 pagesAll Scrutiny of Record For Audit PurposesAdv Muhammad Wasim Awan43% (7)

- Audit UniverseDocument4 pagesAudit UniverseabcdefgNo ratings yet

- 50 Audit Manual For Small Entities Balance Sheet ItemsDocument86 pages50 Audit Manual For Small Entities Balance Sheet Itemssharmaatul95100% (1)

- Synthesis - Auditprobfinalsss 1Document35 pagesSynthesis - Auditprobfinalsss 1Thirdy Mocky100% (1)

- Ais MCQSDocument7 pagesAis MCQSAbdul wahabNo ratings yet

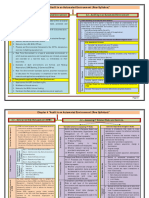

- Chapter 4 - Audit in An Automated Environment by CA - Pankaj GargDocument4 pagesChapter 4 - Audit in An Automated Environment by CA - Pankaj GargAnjali P ANo ratings yet

- Solution Manual For Auditing A Business Risk Approach 8th Edition by Rittenburg Complete Downloadable File atDocument35 pagesSolution Manual For Auditing A Business Risk Approach 8th Edition by Rittenburg Complete Downloadable File atmichelle100% (1)

- Multiple Choice QuestionsDocument20 pagesMultiple Choice QuestionsPhoebe LanoNo ratings yet

- Audit and Working PapersDocument2 pagesAudit and Working PapersJoseph PamaongNo ratings yet

- Consideration of Internal ControlDocument69 pagesConsideration of Internal Controlmah loveNo ratings yet

- Audit Report Cash SalesDocument30 pagesAudit Report Cash SalesPlanco RosanaNo ratings yet

- 2008 Auditing Released MC QuestionsDocument50 pages2008 Auditing Released MC QuestionsOpiey RofiahNo ratings yet

- Revenue Audit ProgrammeDocument6 pagesRevenue Audit ProgrammeDaniela BulardaNo ratings yet

- Audit and Accounting Guide - Depository and Lending Institutions: Banks and Savings Institutions, Credit Unions, Finance Companies, and Mortgage CompaniesFrom EverandAudit and Accounting Guide - Depository and Lending Institutions: Banks and Savings Institutions, Credit Unions, Finance Companies, and Mortgage CompaniesNo ratings yet

- Audit. Review. Compilation. What's the Difference?From EverandAudit. Review. Compilation. What's the Difference?Rating: 5 out of 5 stars5/5 (1)

- Guidelines for Organization of Working Papers on Operational AuditsFrom EverandGuidelines for Organization of Working Papers on Operational AuditsNo ratings yet

- Chapter 11 - Answer PDFDocument7 pagesChapter 11 - Answer PDFjhienellNo ratings yet

- Paper Tech IndustriesDocument20 pagesPaper Tech IndustriesMargaret TaylorNo ratings yet

- TheProcure To PayCyclebyChristineDoxeyDocument6 pagesTheProcure To PayCyclebyChristineDoxeyrajus_cisa6423No ratings yet

- Forensic Techniques and Fraud SchemesDocument7 pagesForensic Techniques and Fraud Schemeskhadine PriceNo ratings yet

- Kant's Doctrine of Virtue Mark Timmons All Chapters Instant DownloadDocument33 pagesKant's Doctrine of Virtue Mark Timmons All Chapters Instant Downloadbluncktzelep100% (1)

- Corning Optical Communications ISO 14001 2015 Expiry 31 October 2022Document2 pagesCorning Optical Communications ISO 14001 2015 Expiry 31 October 2022Rene Pozo MuñozNo ratings yet

- 02-009 Smoking PolicyDocument6 pages02-009 Smoking PolicyJoachimNo ratings yet

- Test 5Document32 pagesTest 5Santosh JagtapNo ratings yet

- Sac & Fox Tribe 2015 Resolution On BlackhawksDocument1 pageSac & Fox Tribe 2015 Resolution On BlackhawksAdam HarringtonNo ratings yet

- Mercury Drug v. Huang, GR 172122, June 22, 2007Document19 pagesMercury Drug v. Huang, GR 172122, June 22, 2007Felix TumbaliNo ratings yet

- Resume Naga Revathi PediredlaDocument6 pagesResume Naga Revathi Pediredlamtra197979No ratings yet

- Yuli PritaniaDocument106 pagesYuli PritaniayoggsssNo ratings yet

- Kapyong Barracks Master PlanDocument56 pagesKapyong Barracks Master PlanElishaDaceyNo ratings yet

- J.V. Angeles Construction Corporation vs. NLRCDocument1 pageJ.V. Angeles Construction Corporation vs. NLRCMarie Chielo100% (1)

- Lawyer Testimony For Its Client That Disqualify Them As CounselDocument28 pagesLawyer Testimony For Its Client That Disqualify Them As CounselJoshua J. IsraelNo ratings yet

- OD429541568776631200Document3 pagesOD429541568776631200ramnonaNo ratings yet

- Salary Slip (32004897 April, 2019) PDFDocument1 pageSalary Slip (32004897 April, 2019) PDFAqsaNo ratings yet

- Advertisement Police ConstablesDocument4 pagesAdvertisement Police ConstablesStephen Ngigi KaranjaNo ratings yet

- Long Quiz 1Document3 pagesLong Quiz 1Ryan Jayson EnriquezNo ratings yet

- ECS - ECS Upgrade Procedures-ECS 2.0.x.x To 2.1.x.x Operating System Offline UpdateDocument18 pagesECS - ECS Upgrade Procedures-ECS 2.0.x.x To 2.1.x.x Operating System Offline Updatepedram.sarrafNo ratings yet

- Emaar Land Registration Title Deed FactsheetDocument3 pagesEmaar Land Registration Title Deed FactsheetHassan AliNo ratings yet

- GaapDocument10 pagesGaapraj4473No ratings yet

- Curriculum Vitae: Primary and Secondary EducationDocument2 pagesCurriculum Vitae: Primary and Secondary EducationkendoNo ratings yet

- Determine The Moment of Inertia of The Area About The Axis. XDocument10 pagesDetermine The Moment of Inertia of The Area About The Axis. XLuis Felipe CostaNo ratings yet

- School of Legal Studies Reva UniversityDocument2 pagesSchool of Legal Studies Reva Universityal aluviNo ratings yet

- The Battle of T AbukDocument3 pagesThe Battle of T AbukAmmar Yusoff100% (1)

- Ticket To ChittaranjanDocument2 pagesTicket To ChittaranjanDeviNo ratings yet

- MB Manual Ga-D525 (425) Tud v1.4 eDocument88 pagesMB Manual Ga-D525 (425) Tud v1.4 eMach MachhiNo ratings yet

- BE Form 1 and Form 1.1Document5 pagesBE Form 1 and Form 1.1MauiArandaSamonteNo ratings yet

- NIFTY Midcap Liquid 15 Apr2020Document1 pageNIFTY Midcap Liquid 15 Apr2020amitNo ratings yet

- Polity 04 - Daily Class Notes - UPSC Sankalp 3.0 (Hinglish)Document5 pagesPolity 04 - Daily Class Notes - UPSC Sankalp 3.0 (Hinglish)jakatiupdateclassesNo ratings yet