Audit of Cash

Audit of Cash

Download as pdf or txt

You might also like

- Auditing Problems Roque 2023-2024Document385 pagesAuditing Problems Roque 2023-2024Roisu De Kuri100% (1)

- Pub - California Real Estate Finance 9th Edition PDFDocument534 pagesPub - California Real Estate Finance 9th Edition PDFThai chheanghourt100% (1)

- Chapter 1 Audit of Cash and Cash EquivalentsDocument127 pagesChapter 1 Audit of Cash and Cash EquivalentsAgatha de Castro82% (22)

- MasterCard - Transaction Processing RulesDocument403 pagesMasterCard - Transaction Processing RulesmoltilibriNo ratings yet

- Quiz 3 Cash Bank Recon Past Exam CompressDocument8 pagesQuiz 3 Cash Bank Recon Past Exam CompressAubrey Shaiyne OfianaNo ratings yet

- Auditing and Assurance Principles Pre TestDocument9 pagesAuditing and Assurance Principles Pre TestKryzzel Anne JonNo ratings yet

- IR1 CashcashEquivDocument4 pagesIR1 CashcashEquivMadielyn Santarin MirandaNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Agamata Answer KeyDocument5 pagesAgamata Answer KeyBromanineNo ratings yet

- Technical AnalysisDocument34 pagesTechnical AnalysisBromanine100% (1)

- ACCTG102 MidtermQ1.5 Cash Make Up ExamDocument6 pagesACCTG102 MidtermQ1.5 Cash Make Up ExamBarrylou Manayan100% (1)

- Audit of CashDocument9 pagesAudit of CashRizzel SubaNo ratings yet

- Long Quiz 1 Acc 205Document6 pagesLong Quiz 1 Acc 205Philip LarozaNo ratings yet

- AUD02 - 05 Audit of Cash and Cash EquivalentsDocument3 pagesAUD02 - 05 Audit of Cash and Cash EquivalentsMark BajacanNo ratings yet

- Audit of Cash (Printable Handout)Document6 pagesAudit of Cash (Printable Handout)katrinailagan3131No ratings yet

- AUDITING - PRELIM - For PrintingDocument4 pagesAUDITING - PRELIM - For PrintingAndreiu Mark EsmeleNo ratings yet

- Review CashDocument2 pagesReview Cashcc aaNo ratings yet

- Special Exam-Prelims: Audit of Cash and Cash Equivalents Problem No. 1Document4 pagesSpecial Exam-Prelims: Audit of Cash and Cash Equivalents Problem No. 1Ma Yra YmataNo ratings yet

- PrAE 304 Auditing and Assurance - MidtermsDocument6 pagesPrAE 304 Auditing and Assurance - MidtermsJeryl AlfantaNo ratings yet

- 1st Activity Cash and Cash Equivalents Bank Reconciliation Proof of CashDocument7 pages1st Activity Cash and Cash Equivalents Bank Reconciliation Proof of CashSheidee ValienteNo ratings yet

- ExtAud 3 Midterm Exam W AnswersDocument12 pagesExtAud 3 Midterm Exam W AnswersJANET ILLESESNo ratings yet

- Bank Reconciliation (IA)Document7 pagesBank Reconciliation (IA)rufamaegarcia07No ratings yet

- Audit of Cash PDFDocument11 pagesAudit of Cash PDFShaira UntalanNo ratings yet

- Refresher Course: Audit of Cash and Cash EquivalentsDocument4 pagesRefresher Course: Audit of Cash and Cash EquivalentsFery Ann100% (1)

- Substantive Testing For Cash and Cash EquivalentDocument20 pagesSubstantive Testing For Cash and Cash EquivalentPaul Anthony AspuriaNo ratings yet

- Post Test Audit Problems Cash and Cash EquivalentsDocument3 pagesPost Test Audit Problems Cash and Cash EquivalentsAlma Vargas DayondonNo ratings yet

- 03 Quiz On Topic 03 Theories and FAR Problems With Answer KeyDocument4 pages03 Quiz On Topic 03 Theories and FAR Problems With Answer KeyNye NyeNo ratings yet

- E-Handout On Audit of Cash and Cash EquivalentsDocument12 pagesE-Handout On Audit of Cash and Cash EquivalentsAsnifah AlinorNo ratings yet

- FAR 02 - Cash and Cash EquivalentsDocument5 pagesFAR 02 - Cash and Cash EquivalentsLorreine MartinezNo ratings yet

- Quiz 1Document11 pagesQuiz 1Sam VeraNo ratings yet

- Quiz - CashDocument8 pagesQuiz - CashChristian QuintansNo ratings yet

- Audit of Cash and Cash Equivalent Problem 1 (Adapted)Document6 pagesAudit of Cash and Cash Equivalent Problem 1 (Adapted)Robelyn Asuna LegaraNo ratings yet

- Ap Tip Preweek 2017Document58 pagesAp Tip Preweek 2017Jay-L Tan100% (1)

- Auditing Problems: Audit of Cash and Cash Equivalents Problem No. 1Document21 pagesAuditing Problems: Audit of Cash and Cash Equivalents Problem No. 1ATLASNo ratings yet

- Cash and Cash Equivalent QuizDocument3 pagesCash and Cash Equivalent QuizApril Rose Sobrevilla DimpoNo ratings yet

- ACCO30053-AACA1 Final-Examination 1st-Semester AY2021-2022 QUESTIONNAIREDocument12 pagesACCO30053-AACA1 Final-Examination 1st-Semester AY2021-2022 QUESTIONNAIREKabalaNo ratings yet

- PA QE - CCE HandoutsDocument6 pagesPA QE - CCE HandoutsBenicel Lane M. D. V.No ratings yet

- Ac3a Qe Oct2014 (TQ)Document15 pagesAc3a Qe Oct2014 (TQ)Julrick Cubio EgbusNo ratings yet

- Practice SetDocument4 pagesPractice SetXena Natividad100% (1)

- Holy Cross College: B. Cause and EffectDocument12 pagesHoly Cross College: B. Cause and EffectSam VeraNo ratings yet

- Audit of Cash and Cash Equivalents: Problem No. 20Document6 pagesAudit of Cash and Cash Equivalents: Problem No. 20Robel MurilloNo ratings yet

- Audit Reviewaudit of CashDocument14 pagesAudit Reviewaudit of CashAndy LaluNo ratings yet

- 1st Long Exam (Summer 2022) WITHOUT ANSWERDocument10 pages1st Long Exam (Summer 2022) WITHOUT ANSWERDaphnie Kitch CatotalNo ratings yet

- Audit of Receivables CaseDocument4 pagesAudit of Receivables CaseJohn Victor Mancilla MonzonNo ratings yet

- Bank Recon & Proof-Set ADocument2 pagesBank Recon & Proof-Set AJaypee BignoNo ratings yet

- Acc 106 Quiz BR and Ar NoakDocument8 pagesAcc 106 Quiz BR and Ar Noakhoneyjoy salapantanNo ratings yet

- Audit of Cash and Cash EquivalentsDocument4 pagesAudit of Cash and Cash EquivalentsstillwinmsNo ratings yet

- Cash and Cash Equivalents (Problems)Document9 pagesCash and Cash Equivalents (Problems)IAN PADAYOGDOGNo ratings yet

- F CFAS-EXAM - Docx 143874436Document48 pagesF CFAS-EXAM - Docx 143874436Athena AthenaNo ratings yet

- Midterm Examination Suggested AnswersDocument9 pagesMidterm Examination Suggested AnswersJoshua CaraldeNo ratings yet

- Review Material ACC PRINTDocument11 pagesReview Material ACC PRINTtjcute125No ratings yet

- Ap Cash Cash Equivalents QuizDocument8 pagesAp Cash Cash Equivalents QuizJenny BernardinoNo ratings yet

- Practice MIDTERM EXAM INTACC 1Document17 pagesPractice MIDTERM EXAM INTACC 1miusdiarieNo ratings yet

- Audit of CashDocument6 pagesAudit of CashMark Lord Morales Bumagat100% (3)

- Reviewees IntaccDocument6 pagesReviewees IntaccKimberly BalontongNo ratings yet

- Reviewees IntaccDocument6 pagesReviewees IntaccMarvic Cabangunay0% (2)

- Cash and Cash Equivalents (Continuation)Document7 pagesCash and Cash Equivalents (Continuation)rufamaegarcia07No ratings yet

- AP Module 2 - Audit of Revenue-Receipt CycleDocument8 pagesAP Module 2 - Audit of Revenue-Receipt CycleHannah Jane ToribioNo ratings yet

- Bookkeeping for Nonprofits: A Step-by-Step Guide to Nonprofit AccountingFrom EverandBookkeeping for Nonprofits: A Step-by-Step Guide to Nonprofit AccountingRating: 4 out of 5 stars4/5 (2)

- 21St Century Computer Solutions: A Manual Accounting SimulationFrom Everand21St Century Computer Solutions: A Manual Accounting SimulationNo ratings yet

- AK Mock BA 99.2 1st LEDocument4 pagesAK Mock BA 99.2 1st LEBromanineNo ratings yet

- AK Mock BA 118.1 2nd LEDocument6 pagesAK Mock BA 118.1 2nd LEBromanineNo ratings yet

- AK Mock BA 141 1st LEDocument2 pagesAK Mock BA 141 1st LEBromanineNo ratings yet

- Partners (Because TAC TCC PAC (New)Document5 pagesPartners (Because TAC TCC PAC (New)BromanineNo ratings yet

- Tariff and Customs Code - CPALEDocument3 pagesTariff and Customs Code - CPALEBromanineNo ratings yet

- 5ea7fb0c57f53 SEC Form 17A Dec2019Document222 pages5ea7fb0c57f53 SEC Form 17A Dec2019BromanineNo ratings yet

- Revised CPALE Syllabus - EditableDocument19 pagesRevised CPALE Syllabus - EditableBromanineNo ratings yet

- Abatement: "A Reduction in The Assessment of Tax, Penalty or Interest When It Is Determined The Assessment Is Incorrect"Document1 pageAbatement: "A Reduction in The Assessment of Tax, Penalty or Interest When It Is Determined The Assessment Is Incorrect"BromanineNo ratings yet

- Mock Board Answer KeyDocument2 pagesMock Board Answer KeyBromanineNo ratings yet

- (Pfrs/Ifrs 16) LeasesDocument11 pages(Pfrs/Ifrs 16) LeasesBromanineNo ratings yet

- 6th Practice Qs 99.2Document3 pages6th Practice Qs 99.2BromanineNo ratings yet

- PRTC Oct2019 1st PB Answer Key PDFDocument2 pagesPRTC Oct2019 1st PB Answer Key PDFBromanineNo ratings yet

- University of The Philippines VisayasDocument2 pagesUniversity of The Philippines VisayasBromanineNo ratings yet

- Hyperinflation and Current CostDocument3 pagesHyperinflation and Current CostBromanineNo ratings yet

- AP 8603 - Audit of Property, Plant and EquipmentDocument6 pagesAP 8603 - Audit of Property, Plant and EquipmentBromanineNo ratings yet

- Mas 8611 PDFDocument11 pagesMas 8611 PDFBromanineNo ratings yet

- Single Entry and Error CorrectionDocument2 pagesSingle Entry and Error CorrectionBromanine0% (1)

- Ap 8605Document6 pagesAp 8605BromanineNo ratings yet

- Opening BalancesDocument37 pagesOpening BalancesBromanineNo ratings yet

- AP 8601 - Audit of Shareholders' EquityDocument8 pagesAP 8601 - Audit of Shareholders' EquityBromanineNo ratings yet

- PDF DocumentDocument4 pagesPDF DocumentmandymariemechtlyNo ratings yet

- KFS HBL Islamic Basic Banking Account - Jul 19Document1 pageKFS HBL Islamic Basic Banking Account - Jul 19M-Waseem AnsariNo ratings yet

- Microsoft Word - Challan FormDocument1 pageMicrosoft Word - Challan FormOm ParkashNo ratings yet

- Study Material: Free Master Class SeriesDocument9 pagesStudy Material: Free Master Class SeriesRakesh AgarwalNo ratings yet

- TXN 04122020 23092020 04122020 NatWestDocument8 pagesTXN 04122020 23092020 04122020 NatWestwendyclaridg75No ratings yet

- General Banking of EXPORT IMPORT BANK OF BANGLADESH LIMITED (EXIM BANK)Document45 pagesGeneral Banking of EXPORT IMPORT BANK OF BANGLADESH LIMITED (EXIM BANK)Moyan HossainNo ratings yet

- List of BBL AB Outlets August 2020Document21 pagesList of BBL AB Outlets August 2020Arif AhmedNo ratings yet

- SME Database and Analysis of SME DataDocument37 pagesSME Database and Analysis of SME DataADBI EventsNo ratings yet

- E BankingDocument74 pagesE BankingKritika Shiva100% (2)

- Sample Procurement Process SBLC PROCEDURES 170Document2 pagesSample Procurement Process SBLC PROCEDURES 170Abraham ArdiansyahNo ratings yet

- Urban Cooperative Banks in India: A Current Scenario and Future ProspectsDocument8 pagesUrban Cooperative Banks in India: A Current Scenario and Future ProspectselunshsharmaNo ratings yet

- University of Mauritius: Faculty of Law and ManagementDocument3 pagesUniversity of Mauritius: Faculty of Law and ManagementRevatee HurilNo ratings yet

- 02 Fin MarketDocument89 pages02 Fin MarketyovitaNo ratings yet

- An Evaluation of Deposit Schemes of United Commercial Bank LimitedDocument51 pagesAn Evaluation of Deposit Schemes of United Commercial Bank LimitedHarunur RashidNo ratings yet

- The Tools of Monetary PolicyDocument53 pagesThe Tools of Monetary Policyrichard kapimpaNo ratings yet

- Mitc CCDocument20 pagesMitc CCinthu389No ratings yet

- Overview of Legal and Regulatory Framework of Islamic FinanceDocument13 pagesOverview of Legal and Regulatory Framework of Islamic FinancenanaNo ratings yet

- SBLC OmanDocument28 pagesSBLC OmanSAMRAT SIL67% (3)

- Weekly Bond ListDocument83 pagesWeekly Bond ListMohan MirpuriNo ratings yet

- Law On Bouncing Checks: Batas Pambansa Blg.22 (1979)Document6 pagesLaw On Bouncing Checks: Batas Pambansa Blg.22 (1979)Jm SantosNo ratings yet

- Dishonour of ChequeDocument4 pagesDishonour of ChequeRaj Kumar100% (1)

- Speculation Demon BankDocument3 pagesSpeculation Demon BankFreya RenataNo ratings yet

- Baucar Bayaran - AinDocument7 pagesBaucar Bayaran - AinAienShafaainNo ratings yet

- 3-Months-Bank-Statement-Absa 63104622 1 63104906 63107485 63129820 63148896Document2 pages3-Months-Bank-Statement-Absa 63104622 1 63104906 63107485 63129820 63148896O'nako KadeniNo ratings yet

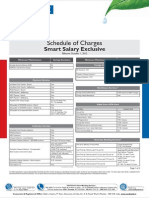

- Schedule of Charges: Smart Salary ExclusiveDocument2 pagesSchedule of Charges: Smart Salary ExclusivevedavakNo ratings yet

- Crypto Survey - Google FormsDocument5 pagesCrypto Survey - Google Forms208vaibhav bajajNo ratings yet

- Ppbi NotesDocument10 pagesPpbi Notespriteshkasar51No ratings yet

- TVM Pratice Question-1Document12 pagesTVM Pratice Question-1Neetu Dubey100% (4)