Spectral Dilation

Spectral Dilation

Download as pdf or txt

You might also like

- Mastering Hurst Cycle Analysis: A modern treatment of Hurst's original system of financial market analysisFrom EverandMastering Hurst Cycle Analysis: A modern treatment of Hurst's original system of financial market analysisRating: 4.5 out of 5 stars4.5/5 (2)

- High Dive PortfolioDocument6 pagesHigh Dive Portfoliosophienorton0% (1)

- Ehlers (Bandpass)Document7 pagesEhlers (Bandpass)Jim Baxter100% (1)

- ACT Summary Manual PDFDocument21 pagesACT Summary Manual PDFTrashHeadNo ratings yet

- Mathematical Basis of Elliot WaveDocument3 pagesMathematical Basis of Elliot Wavejaneb7982No ratings yet

- STOCHASDocument24 pagesSTOCHASNarendra BholeNo ratings yet

- Adaptive Cyber Cycle IndicatorDocument1 pageAdaptive Cyber Cycle IndicatordocbraunNo ratings yet

- Fouriertransforms PDFDocument10 pagesFouriertransforms PDFPinky BhagwatNo ratings yet

- The Birth of Pivots and The PitchforkDocument14 pagesThe Birth of Pivots and The PitchforkashokrajanNo ratings yet

- Ehlers. The CG OscillatorDocument4 pagesEhlers. The CG OscillatorPapy RysNo ratings yet

- Rhythmic Wave DiagramsDocument6 pagesRhythmic Wave DiagramsCameron GardnerNo ratings yet

- DeCycler by EHLERSDocument5 pagesDeCycler by EHLERSbulut33No ratings yet

- Zimmel, M. - Bradley Siderograph For 2004 (2003)Document6 pagesZimmel, M. - Bradley Siderograph For 2004 (2003)skorpiohpNo ratings yet

- Pasavento Instructions For Zup Pattern IndicatorDocument13 pagesPasavento Instructions For Zup Pattern IndicatormleefxNo ratings yet

- Ehlers FiltersDocument13 pagesEhlers Filtersmic101100% (1)

- Full Trading Circle - 2012 - Yu - Harmonic Pattern TradingDocument16 pagesFull Trading Circle - 2012 - Yu - Harmonic Pattern TradingParminder Singh MatharuNo ratings yet

- Hursts Eight Principals of Cycle AnalysisDocument1 pageHursts Eight Principals of Cycle AnalysisVijay VijiNo ratings yet

- John Ehlers - TheInverseFisherTransform PDFDocument5 pagesJohn Ehlers - TheInverseFisherTransform PDFArc Angel MNo ratings yet

- Ehlers (Measuring Cycles)Document7 pagesEhlers (Measuring Cycles)chauchauNo ratings yet

- Elliott Wave TheoryDocument8 pagesElliott Wave Theorygursharan4marchNo ratings yet

- Timing Solutions For Swing Traders - 2012 - Lee - Ruling Planets of The Natural HoroscopeDocument2 pagesTiming Solutions For Swing Traders - 2012 - Lee - Ruling Planets of The Natural HoroscopeSourav KunduNo ratings yet

- Emmett T.J. Fibonacci Forecast ExamplesDocument9 pagesEmmett T.J. Fibonacci Forecast ExamplesAnantJaiswal100% (1)

- Investment Educators: Free Charting LessonDocument2 pagesInvestment Educators: Free Charting Lessonpderby1No ratings yet

- The Tillman MethodDocument5 pagesThe Tillman Methodss100% (1)

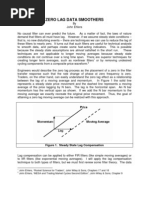

- Zero Lag Data Smoothers: Figure 1. Steady State Lag CompensationDocument8 pagesZero Lag Data Smoothers: Figure 1. Steady State Lag Compensationnanaa0100% (2)

- Recurring Phase of Cycle Analysis - John EhlersDocument8 pagesRecurring Phase of Cycle Analysis - John EhlersTrader CatNo ratings yet

- Eliot WaveDocument8 pagesEliot Wavegagan585No ratings yet

- Walter Russell & Gann Vortex Analysis. Price Is A Wave MagnetDocument9 pagesWalter Russell & Gann Vortex Analysis. Price Is A Wave MagnethofrathNo ratings yet

- Catching Currency Moves With Schaff Trend CycleDocument6 pagesCatching Currency Moves With Schaff Trend CycleNick Riviera100% (1)

- Follow Fibonacci Ratio Dynamic Approach in TradeDocument4 pagesFollow Fibonacci Ratio Dynamic Approach in TradeLatika DhamNo ratings yet

- Market Cycle Timing and Forecast 2016 2017 PDFDocument22 pagesMarket Cycle Timing and Forecast 2016 2017 PDFpravinyNo ratings yet

- Delta - Tides - Astro-Events Feb 15th To May 15th 2012Document4 pagesDelta - Tides - Astro-Events Feb 15th To May 15th 2012Salim MarchantNo ratings yet

- Market Technician No40Document20 pagesMarket Technician No40ppfahd100% (1)

- Planet - : EconomicsDocument9 pagesPlanet - : EconomicsVenkatNo ratings yet

- Journal 1978 MayDocument64 pagesJournal 1978 MaySumit Verma100% (1)

- Swami ChartsDocument5 pagesSwami Chartscyrus68No ratings yet

- What Is The Time FactorDocument35 pagesWhat Is The Time FactorPravin Yeluri0% (1)

- 5th WAVE CALCULATORDocument4 pages5th WAVE CALCULATORrafa manggala100% (1)

- ESignal Manual Ch24 TJ EllipsDocument8 pagesESignal Manual Ch24 TJ EllipslaxmiccNo ratings yet

- Treasury Bonds A Longer Term Perspective: by Robert R. LussierDocument31 pagesTreasury Bonds A Longer Term Perspective: by Robert R. LussierGajini Satish100% (1)

- Forecast For 1929Document33 pagesForecast For 1929James RiceNo ratings yet

- A Course in Cycles (Public)Document63 pagesA Course in Cycles (Public)hofrath100% (4)

- 05 - 1979 MayDocument70 pages05 - 1979 MayLinda ZwaneNo ratings yet

- Erman,+W.T.+ (2002) Log+Spirals+in+the+Stock+MarketDocument12 pagesErman,+W.T.+ (2002) Log+Spirals+in+the+Stock+MarketNishant ThakkarNo ratings yet

- EhlersDecycler IIDocument3 pagesEhlersDecycler IIAlireza P100% (1)

- Tim Morge InterviewDocument4 pagesTim Morge Interviewtawhid anamNo ratings yet

- TD Sequential and Ermano Me TryDocument70 pagesTD Sequential and Ermano Me Trynikesh_prasadNo ratings yet

- Planetary TradingDocument22 pagesPlanetary TradingArunKumarNo ratings yet

- Ehlers, J. - Cycles TutorialDocument17 pagesEhlers, J. - Cycles Tutorialpoli666100% (3)

- Mesa (Maximum Entropy Spectral Analysis)Document9 pagesMesa (Maximum Entropy Spectral Analysis)Francis LinNo ratings yet

- Bressert, Walter (Article) Cycle Timing Can Improve Your Timing Performance - RDocument6 pagesBressert, Walter (Article) Cycle Timing Can Improve Your Timing Performance - Rhofrath100% (1)

- Home Software Prices Download Yahoo Charts: MM Lines Description (From Tim Kruzel)Document46 pagesHome Software Prices Download Yahoo Charts: MM Lines Description (From Tim Kruzel)SOLARSOULNo ratings yet

- Don K. Mak - The Science of Financial Market Trading-World Scientific Publishing Company (2003)Document260 pagesDon K. Mak - The Science of Financial Market Trading-World Scientific Publishing Company (2003)Kusuriuri Accountsman100% (2)

- Traders World Issue 48Document101 pagesTraders World Issue 48clarkpd6100% (1)

- Cycles In Our History Predict A (Nuclear?) World War: History Cycles, Time FractualsFrom EverandCycles In Our History Predict A (Nuclear?) World War: History Cycles, Time FractualsNo ratings yet

- Millard on Channel Analysis: The Key to Share Price PredictionFrom EverandMillard on Channel Analysis: The Key to Share Price PredictionRating: 5 out of 5 stars5/5 (1)

- PRS Solution 130214Document20 pagesPRS Solution 130214tomoNo ratings yet

- FT-60R Quick Guide, Rev 3Document22 pagesFT-60R Quick Guide, Rev 3yu7bx2178No ratings yet

- Q and AnsDocument4 pagesQ and Ansnonu kumarNo ratings yet

- Technical Solution 5G v2.1Document25 pagesTechnical Solution 5G v2.1Juan E Perez PNo ratings yet

- AC DC Clamp and Range Meter - Model 2608ADocument2 pagesAC DC Clamp and Range Meter - Model 2608Achockanan suwanprasertNo ratings yet

- MSC - QP Setting For II MIDDocument5 pagesMSC - QP Setting For II MIDHarini VemulaNo ratings yet

- TMS 1000 Series Data Manual Dec76Document46 pagesTMS 1000 Series Data Manual Dec76Juan EstebanNo ratings yet

- Circuit MakerDocument8 pagesCircuit MakerCarlos PontesNo ratings yet

- Download Full Introduction to Electronic Engineering 1st Edition Valery Vodovozov PDF All ChaptersDocument40 pagesDownload Full Introduction to Electronic Engineering 1st Edition Valery Vodovozov PDF All Chaptersestischirawj100% (1)

- V1.1.2 User Manual: BlueboxDocument56 pagesV1.1.2 User Manual: BlueboxArthur ErpenNo ratings yet

- Courseplan For Avionics II - FinalDocument7 pagesCourseplan For Avionics II - FinalSonali SrivastavaNo ratings yet

- Samsung PL42S5S Chasis D72ADocument15 pagesSamsung PL42S5S Chasis D72AGerciano ChavesNo ratings yet

- MSM MSO+catalog PDFDocument10 pagesMSM MSO+catalog PDFAnonymous UdzF3EMIxINo ratings yet

- Amsat-Iaru Link Model Rev2.5.5Document122 pagesAmsat-Iaru Link Model Rev2.5.5Furkan KahramanNo ratings yet

- Resonant Converters 1Document17 pagesResonant Converters 1NagababuMutyalaNo ratings yet

- The Road To 600GDocument3 pagesThe Road To 600GDo Xuan HuuNo ratings yet

- Crystalpbx Programmingmanual-Rv03Document66 pagesCrystalpbx Programmingmanual-Rv03LalchandraPanickerNo ratings yet

- SEI15024 SELmanualDocument14 pagesSEI15024 SELmanualDani OvilorNo ratings yet

- Kidde PDC Bells by Potter K-75-022Document2 pagesKidde PDC Bells by Potter K-75-022Liana ThanNo ratings yet

- Ic 8279Document3 pagesIc 8279Akshat KaleNo ratings yet

- Instructions For Canceling A False Distress AlertDocument2 pagesInstructions For Canceling A False Distress AlertTuyen NguyenNo ratings yet

- Controlnet Coax Bnc2Tnc Adapter: What'S in This DocumentDocument12 pagesControlnet Coax Bnc2Tnc Adapter: What'S in This DocumentwilfredoNo ratings yet

- Computer Network Q - A Part-1Document7 pagesComputer Network Q - A Part-1Avi DahiyaNo ratings yet

- Interface Serial: Factory Line Ethernet Cable Factory Line Ethernet InfrastructureDocument1 pageInterface Serial: Factory Line Ethernet Cable Factory Line Ethernet InfrastructureRicardo EsquivelNo ratings yet

- Guide Anviz T5Pro T5 v1 4 EN PDFDocument2 pagesGuide Anviz T5Pro T5 v1 4 EN PDFLinneoSalgadoNo ratings yet

- AT8PE53B 1v02 011Document53 pagesAT8PE53B 1v02 011DiegoHilárioNo ratings yet

- Multiple Trading Price List 2023Document16 pagesMultiple Trading Price List 2023rubelNo ratings yet

- Fortune 500 Spreadsheet List 2015Document120 pagesFortune 500 Spreadsheet List 2015David BowmanNo ratings yet

- Assignment 1: PSDC Engineering Certificate Assessment: (CLO:)Document9 pagesAssignment 1: PSDC Engineering Certificate Assessment: (CLO:)Tay KoonleNo ratings yet

- 2 SC 3264Document2 pages2 SC 3264CESAR YONATHAN ALMANZA RIVERANo ratings yet