Akuntansi Keuangan Ii Sesi 6

Akuntansi Keuangan Ii Sesi 6

Download as docx, pdf, or txt

You might also like

- New Heritage Doll Company:: Capital BudgetingDocument27 pagesNew Heritage Doll Company:: Capital BudgetingInêsRosário100% (10)

- Q1: Complete The Valuation Exercise Given in The Sheet R-ToolDocument4 pagesQ1: Complete The Valuation Exercise Given in The Sheet R-ToolSuryakant Burman100% (1)

- Soal Debt InvestmentDocument5 pagesSoal Debt InvestmentKyle Kuro0% (1)

- ch17 180206123815 PDFDocument75 pagesch17 180206123815 PDFYeni Amelia100% (1)

- Problem: Andres Adi Putra S 43220110067 AKM2-Forum 6Document17 pagesProblem: Andres Adi Putra S 43220110067 AKM2-Forum 6tes doang100% (1)

- AKM 2 - Forum 7 - Andres - 43220110067Document13 pagesAKM 2 - Forum 7 - Andres - 43220110067tes doangNo ratings yet

- Intermediate Accounting: Assignment 2Document2 pagesIntermediate Accounting: Assignment 2Putri SerlyNo ratings yet

- E13.2 (LO 1) (Accounts and Notes Payable) The Following Are Selected 2022 Transactions ofDocument4 pagesE13.2 (LO 1) (Accounts and Notes Payable) The Following Are Selected 2022 Transactions ofChupa HesNo ratings yet

- E10 7Document7 pagesE10 7fabiarachid100% (1)

- Pembahasan CH 3 4 5Document30 pagesPembahasan CH 3 4 5bella50% (2)

- Wahyudi-Syaputra Assignment-2 Akl-IiDocument4 pagesWahyudi-Syaputra Assignment-2 Akl-IiWahyudi Syaputra100% (1)

- Wey IFRS 4e PPT Ch03Document88 pagesWey IFRS 4e PPT Ch03Ruiran CuiNo ratings yet

- Tugas Jatuh Tempo Sesi 9Document8 pagesTugas Jatuh Tempo Sesi 9Araminta DewatiNo ratings yet

- Jawaban BE15 - AKMDocument3 pagesJawaban BE15 - AKMMazz BadruezNo ratings yet

- E21.4 (LO 2, 4) (Lessee Entries, Unguaranteed Residual Value) Assume That OnDocument3 pagesE21.4 (LO 2, 4) (Lessee Entries, Unguaranteed Residual Value) Assume That OnWarmthx0% (1)

- Ammar Yasir - 041911333245 - Tugas AKM III WEEK 8Document7 pagesAmmar Yasir - 041911333245 - Tugas AKM III WEEK 8sari ayuNo ratings yet

- Rika Ristiani - Akuntansi Keuangan Menengah 2 - TM-02Document5 pagesRika Ristiani - Akuntansi Keuangan Menengah 2 - TM-02MARCHO AGUSTANo ratings yet

- KasdanPiutang 4B Kelompok1Document11 pagesKasdanPiutang 4B Kelompok1Estin TasyaNo ratings yet

- Chapter 18Document10 pagesChapter 18Ali Abu Al Saud100% (2)

- Soal Kiesio Chapter 16Document4 pagesSoal Kiesio Chapter 16helfiani putri100% (1)

- Tugas Latihan Soal EPSDocument4 pagesTugas Latihan Soal EPSNaoya FaldinyNo ratings yet

- 302 CH 14 Class ProblemsDocument7 pages302 CH 14 Class ProblemsBettie Sanchez100% (1)

- Latihan Kas PiutangDocument2 pagesLatihan Kas Piutangrismaaai0% (1)

- Week1 SolutionsDocument14 pagesWeek1 SolutionsM Mustafa100% (1)

- KIeso Chapter 18 Part 1Document8 pagesKIeso Chapter 18 Part 1Pelangi DiamondNo ratings yet

- Nisha Nur Aini - 43219110183 - TM 01 - AKM IIDocument11 pagesNisha Nur Aini - 43219110183 - TM 01 - AKM IInisha nuraini100% (1)

- Akuntansi KeuanganDocument11 pagesAkuntansi KeuanganDyan NoviaNo ratings yet

- Week13 SolutionsDocument14 pagesWeek13 SolutionsRian Rorres100% (1)

- Tugas Ch.14Document6 pagesTugas Ch.14Chupa HesNo ratings yet

- Zulfitri Handayani - A031191125 (Akkeu P15-3)Document6 pagesZulfitri Handayani - A031191125 (Akkeu P15-3)RismayantiNo ratings yet

- Muh - Syukur (A031191077) Akuntansi Keuangan - Exercise E.12.9Document3 pagesMuh - Syukur (A031191077) Akuntansi Keuangan - Exercise E.12.9Rismayanti100% (1)

- Nisha Nur Aini - 43219110183 - TM 02 - AKM IIDocument11 pagesNisha Nur Aini - 43219110183 - TM 02 - AKM IInisha nuraini100% (1)

- Tugas Akuntansi Menengah Ii Dilutive Securities & Earnings Per ShareDocument2 pagesTugas Akuntansi Menengah Ii Dilutive Securities & Earnings Per ShareClarissa NastaniaNo ratings yet

- DDDocument4 pagesDDAmelia Salini100% (1)

- Jawaban Soal Latihan Ch.11Document2 pagesJawaban Soal Latihan Ch.11Wira DinataNo ratings yet

- Tugas AKM II Minggu 9Document2 pagesTugas AKM II Minggu 9Clarissa Nastania100% (1)

- Problem 14-10Document2 pagesProblem 14-10annisaNo ratings yet

- Chapter 16 Homework SolutionsDocument11 pagesChapter 16 Homework Solutionsyuri100% (2)

- CH 14Document71 pagesCH 14Febriana Nurul HidayahNo ratings yet

- E14-8 (Entries and Questions For Bond Transactions) On June 30, 2010, Mackers CompanyDocument3 pagesE14-8 (Entries and Questions For Bond Transactions) On June 30, 2010, Mackers CompanySandra SholehahNo ratings yet

- 13 2Document2 pages13 2Evelyn Roldan100% (8)

- Exercise 6Document1 pageExercise 6Kayla SheltonNo ratings yet

- Individual Assignments 2Document8 pagesIndividual Assignments 2Arista Yuliana SariNo ratings yet

- Week 2 Homework (Chap. 4) - PostedDocument4 pagesWeek 2 Homework (Chap. 4) - PostedMs. Nina100% (5)

- Ch. 17 Exercises and Answers - TaggedDocument6 pagesCh. 17 Exercises and Answers - TaggedHaitham Ebrahim100% (1)

- AKM - Kelompok 5Document8 pagesAKM - Kelompok 5lailafitriyani100% (1)

- A1C019118 Jurati Latihan7Document6 pagesA1C019118 Jurati Latihan7jurati100% (1)

- Soal Ch. 15Document6 pagesSoal Ch. 15Kyle KuroNo ratings yet

- Solman Dulu DehDocument3 pagesSolman Dulu Dehbaru uuNo ratings yet

- E14-3 (Entries For Bond Transactions) Presented Below Are Two Independent SituationsDocument3 pagesE14-3 (Entries For Bond Transactions) Presented Below Are Two Independent SituationsAsuna SanNo ratings yet

- E18-1 p18-10Document4 pagesE18-1 p18-10ariena alifia s100% (1)

- CH 4 - Brief Exercises - 16thDocument18 pagesCH 4 - Brief Exercises - 16thkesey100% (2)

- E22-6 (LO 2) Accounting Changes-DepreciationDocument6 pagesE22-6 (LO 2) Accounting Changes-DepreciationRiana DeztianiNo ratings yet

- T4 - (Assets) - Qs and SolutionDocument22 pagesT4 - (Assets) - Qs and SolutionCalvin MaNo ratings yet

- ACY4001 Individual Assignment 2 SolutionsDocument7 pagesACY4001 Individual Assignment 2 SolutionsMorris LoNo ratings yet

- Chapter 7 SolutionsDocument6 pagesChapter 7 SolutionsJay100% (1)

- Jawaban TugasDocument7 pagesJawaban TugasRani AdhirasariNo ratings yet

- Aset TetapDocument9 pagesAset TetapMAYONA MEGAHTANo ratings yet

- Presented Below Is The Trial Balance of Vivaldi Spa at December 31, 2019Document2 pagesPresented Below Is The Trial Balance of Vivaldi Spa at December 31, 2019SalsabiilaNo ratings yet

- Modul 04 - Dilutive Securities and Earning Per ShareDocument4 pagesModul 04 - Dilutive Securities and Earning Per ShareHilma Nahla SawalyaNo ratings yet

- Pertemuan 4 Dilutive Securities and Earnings Per Share: Tim Asistensi AkuntansiDocument3 pagesPertemuan 4 Dilutive Securities and Earnings Per Share: Tim Asistensi AkuntansiIlyasa YusufNo ratings yet

- Modul 04 - Dilutive Securities and Earning Per ShareDocument4 pagesModul 04 - Dilutive Securities and Earning Per Shareκrιvαn mατιυsNo ratings yet

- 9TH Bonds Payable Part IIDocument8 pages9TH Bonds Payable Part IIAnthony DyNo ratings yet

- Solutions Guide: This Is Meant As A Solutions GuideDocument4 pagesSolutions Guide: This Is Meant As A Solutions GuideVivienne Lei BolosNo ratings yet

- Befa Question BankDocument9 pagesBefa Question Bank20bd1a6655No ratings yet

- ACC 108 P3 Quiz 1 Ans KeyDocument6 pagesACC 108 P3 Quiz 1 Ans Keyrago.cachero.auNo ratings yet

- Form 16 - 22-23Document9 pagesForm 16 - 22-23Trilok SHARMANo ratings yet

- Ambit Good & Clean Smallcap Fund (Emerging Giants) : Portfolio Management ServicesDocument26 pagesAmbit Good & Clean Smallcap Fund (Emerging Giants) : Portfolio Management ServicesSaurabh MukherjeeNo ratings yet

- FM014 - Feasibility Studies Preparation, Analysis EvaluationDocument4 pagesFM014 - Feasibility Studies Preparation, Analysis EvaluationMelkamu BazieNo ratings yet

- Cap BudgetDocument20 pagesCap Budgetprachik87No ratings yet

- Accounting Assignment Acc1103Document13 pagesAccounting Assignment Acc1103api-549748043No ratings yet

- Weaver Corporation AssignmentDocument2 pagesWeaver Corporation Assignmentmusozi marvinNo ratings yet

- Larsen& Toubro LTD Initiating Coverage 15062020Document8 pagesLarsen& Toubro LTD Initiating Coverage 15062020Aparna JRNo ratings yet

- Hafiz Salman Majeed: Composed & SolvedDocument13 pagesHafiz Salman Majeed: Composed & SolvedFun NNo ratings yet

- Create Asset SBDocument34 pagesCreate Asset SBchotabheem199523No ratings yet

- Chapter 15Document2 pagesChapter 15Asep KurniaNo ratings yet

- Topic 6 - Credit Management SlidesDocument10 pagesTopic 6 - Credit Management SlidesDr-Wasim Abbas ShaheenNo ratings yet

- Code Bài Material OutsourcingDocument3 pagesCode Bài Material OutsourcingTrịnh Hồng HàNo ratings yet

- What Is AccountingDocument3 pagesWhat Is AccountingEmmanuel James SevillaNo ratings yet

- Chilean Equity DashboardDocument6 pagesChilean Equity DashboardFrancisco CourbisNo ratings yet

- PAS 7 Statement of Cash FlowsDocument7 pagesPAS 7 Statement of Cash FlowsAbbie Young Dela CruzNo ratings yet

- LK Trio 2015Document109 pagesLK Trio 2015Allen AveskhaNo ratings yet

- ULOe - Financial Planning - 0Document19 pagesULOe - Financial Planning - 0pam pamNo ratings yet

- Chapter # 4 Foundations of Ratio and Financial AnalysisDocument49 pagesChapter # 4 Foundations of Ratio and Financial AnalysisAnna MahmudNo ratings yet

- Capital BudgetingDocument5 pagesCapital Budgetingshafiqul84No ratings yet

- Accounts ProjectDocument29 pagesAccounts ProjectazeemNo ratings yet

- Fixed Assets (FINAL)Document13 pagesFixed Assets (FINAL)Salman Saeed100% (1)

- Unit-4 Study MaterialDocument19 pagesUnit-4 Study MaterialSETHUMADHAVAN BNo ratings yet

- CH 11Document48 pagesCH 11Pham Khanh Duy (K16HL)No ratings yet

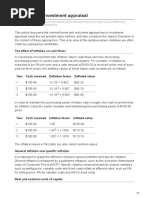

- D1 Inflation and Investment AppraisalDocument7 pagesD1 Inflation and Investment AppraisalTENGKU ANIS TENGKU YUSMANo ratings yet