Acg5205 Solutions Ch.11 - Christensen 12e

Acg5205 Solutions Ch.11 - Christensen 12e

Download as docx, pdf, or txt

You might also like

- AHM13e - Chapter 01 - Key To EOC Problems and CasesDocument14 pagesAHM13e - Chapter 01 - Key To EOC Problems and CasesArunesh SN100% (1)

- Doug and Susan Clark Case Study.2017Document45 pagesDoug and Susan Clark Case Study.2017Ryan Nguyen0% (1)

- Midterm 2 (Fall 2020) FMGT 2293Document7 pagesMidterm 2 (Fall 2020) FMGT 2293brendonNo ratings yet

- Use The Following Information For The Next Three Questions:: Activity 3.2Document2 pagesUse The Following Information For The Next Three Questions:: Activity 3.2Tine Vasiana DuermeNo ratings yet

- Use The Following Information For The Next Three Questions:: Activity 3.2Document11 pagesUse The Following Information For The Next Three Questions:: Activity 3.2Jade jade jadeNo ratings yet

- Kasus Chapter 2-AnswerDocument3 pagesKasus Chapter 2-Answermadesugandhi100% (1)

- 1943191Document5 pages1943191mohitgaba19No ratings yet

- Nobles Finman6e SMQ CH23Document77 pagesNobles Finman6e SMQ CH23Ryan Nguyen100% (2)

- Electricity BillDocument1 pageElectricity Billsreeram yadavNo ratings yet

- Quiz Adv Acc 2Document3 pagesQuiz Adv Acc 2georgius gabrielNo ratings yet

- MCQ With AnswersDocument27 pagesMCQ With AnswersAnonymous qi4PZkNo ratings yet

- Financial Accounting - Tugas 2 - 9 Oktober 2019Document3 pagesFinancial Accounting - Tugas 2 - 9 Oktober 2019AlfiyanNo ratings yet

- Kristianto Harikatan 210611040176 Pa1Document9 pagesKristianto Harikatan 210611040176 Pa1Christianto HarikatanNo ratings yet

- Tugas 12 AKL 2 - Lidia Ayu Lestari - 21043043Document7 pagesTugas 12 AKL 2 - Lidia Ayu Lestari - 21043043Lidya Ayu LestariNo ratings yet

- ACCT 210-Fall 21-22-Revision Sheet - FinalDocument3 pagesACCT 210-Fall 21-22-Revision Sheet - FinalAndrew PhilipsNo ratings yet

- Devia Febrina 43221110106 - Kuis 10 AKL 2Document4 pagesDevia Febrina 43221110106 - Kuis 10 AKL 2nara kimNo ratings yet

- Kelompok 1 (Intan)Document14 pagesKelompok 1 (Intan)Amanda VeronikaNo ratings yet

- Ika Rani Widiastuti 22219914 2EB15 M5 ModalDocument4 pagesIka Rani Widiastuti 22219914 2EB15 M5 ModalIka RaniNo ratings yet

- Book Value Per Share 950,000.00 500,000.00 250,000.00 (Add) 100,000.00 Bvps 17Document9 pagesBook Value Per Share 950,000.00 500,000.00 250,000.00 (Add) 100,000.00 Bvps 17jose.labianoNo ratings yet

- Akl Felix UasDocument36 pagesAkl Felix UasBlue WhileNo ratings yet

- Advanced Financial Accounting Chapter 11 Problem SolutionsDocument6 pagesAdvanced Financial Accounting Chapter 11 Problem SolutionsEmily PiperNo ratings yet

- p4 2Document5 pagesp4 2Ernike SariNo ratings yet

- Acct 4010 Ch2-Handout-SolutionDocument4 pagesAcct 4010 Ch2-Handout-Solutionlokyee801mikiNo ratings yet

- Translation 1Document4 pagesTranslation 1Pasha HarahapNo ratings yet

- Foreign Currency Transactions and DerivativesDocument4 pagesForeign Currency Transactions and Derivativesmartinfaith958No ratings yet

- Dayag 9Document2 pagesDayag 9dmangiginNo ratings yet

- Latihan Soal Akl CH 1 Dan 2Document12 pagesLatihan Soal Akl CH 1 Dan 2DheaNo ratings yet

- IFR - Tutorial W4 - Extra ExerciseDocument2 pagesIFR - Tutorial W4 - Extra Exercises.h.j.braamhaarNo ratings yet

- Kunci Kuis AKL 2Document9 pagesKunci Kuis AKL 2Ilham Dwi NoviantoNo ratings yet

- Plantilla Tarea 1 1 ACCO 3150 4mjjDocument5 pagesPlantilla Tarea 1 1 ACCO 3150 4mjjcrispyy turonNo ratings yet

- Akuntansi Account ReceivableDocument8 pagesAkuntansi Account Receivablem habiburrahman55No ratings yet

- Problems WPS OfficeDocument6 pagesProblems WPS Officelaica valderasNo ratings yet

- Fabozzi Handbook Fixed Income 7th EditionDocument2 pagesFabozzi Handbook Fixed Income 7th EditionBhagyeshGhagiNo ratings yet

- Translation QuestionsDocument6 pagesTranslation QuestionsVeenal BansalNo ratings yet

- Date Account Titles & Explanation Debit Credit: A. Prepare EntriesDocument4 pagesDate Account Titles & Explanation Debit Credit: A. Prepare Entriesyogi fetriansyahNo ratings yet

- Home Assignment Ch.1Document6 pagesHome Assignment Ch.1Sausan SaniaNo ratings yet

- Accounts From Incomplete RecordsDocument7 pagesAccounts From Incomplete RecordsShahzaib ShaikhNo ratings yet

- ACT 310part B PDFDocument5 pagesACT 310part B PDFNiloy NeogiNo ratings yet

- Forex Exercises With TranslationDocument4 pagesForex Exercises With TranslationViky Rose EballeNo ratings yet

- AKM Week 3Document4 pagesAKM Week 3ELSA SYAFIRA ANANTANo ratings yet

- baitap-sinhvien-IAS 21Document12 pagesbaitap-sinhvien-IAS 21tonight752No ratings yet

- Sherlin - 198110790 - Tugas 1 Akuntansi Keuangan LanjutanDocument6 pagesSherlin - 198110790 - Tugas 1 Akuntansi Keuangan LanjutanSherlin KhuNo ratings yet

- KasdanPiutang 4B Kelompok1Document11 pagesKasdanPiutang 4B Kelompok1Estin TasyaNo ratings yet

- TP 1 - Accounting IIDocument11 pagesTP 1 - Accounting IIAbiNo ratings yet

- AA Chap 9Document42 pagesAA Chap 9Thu NguyenNo ratings yet

- Akl P4.3 & P4.4Document18 pagesAkl P4.3 & P4.4Dhivena JeonNo ratings yet

- LU4 Class QuestionsDocument8 pagesLU4 Class QuestionsAmanda FumbaNo ratings yet

- Chapter 2 International AccountingDocument6 pagesChapter 2 International AccountingmonaelshamiNo ratings yet

- Example 1: Princess Ella IncorporatedDocument4 pagesExample 1: Princess Ella IncorporatedStanly ChanNo ratings yet

- Mas DocumentsDocument12 pagesMas DocumentsLorie Grace LagunaNo ratings yet

- Chapter 11 Tugas DosenDocument11 pagesChapter 11 Tugas DosenElsa Siregar100% (1)

- E 16.3 Date Account Ref DR CRDocument13 pagesE 16.3 Date Account Ref DR CRNicolas ErnestoNo ratings yet

- E18-7 Bennis Company ExerciseDocument1 pageE18-7 Bennis Company ExerciseTagowearNo ratings yet

- P3.5 Different Forms of Business CombinationDocument8 pagesP3.5 Different Forms of Business CombinationAgnes CahyaNo ratings yet

- Tugas P11 AkuntansiDocument3 pagesTugas P11 Akuntansikim95kthNo ratings yet

- SOLUTION MANUAL Akm 1 PDFDocument4 pagesSOLUTION MANUAL Akm 1 PDFRizka khairunnisaNo ratings yet

- 5i - Elsa Rosalinda - 2102015030 - Tugas DISKUSI 2 AFTER UTS - Materi 11Document5 pages5i - Elsa Rosalinda - 2102015030 - Tugas DISKUSI 2 AFTER UTS - Materi 11Elsa RosalindaNo ratings yet

- Finals Quiz No. 1 AnswersDocument4 pagesFinals Quiz No. 1 AnswersMergierose DalgoNo ratings yet

- FA TableDocument8 pagesFA TableVy Duong TrieuNo ratings yet

- MYLcDdlJEeiLrQ7oUIZkDg Week 5 SlidesDocument20 pagesMYLcDdlJEeiLrQ7oUIZkDg Week 5 SlidesKashif RazaNo ratings yet

- Chap11 ConnectDocument5 pagesChap11 ConnectThanh PhuongNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- Acg5205 Solutions Ch.16 - Christensen 12eDocument10 pagesAcg5205 Solutions Ch.16 - Christensen 12eRyan NguyenNo ratings yet

- Acg5205 Solutions Ch.15 - Christensen 12eDocument19 pagesAcg5205 Solutions Ch.15 - Christensen 12eRyan NguyenNo ratings yet

- Acg5205 Solutions Ch.08 - SL - Christensen 12eDocument15 pagesAcg5205 Solutions Ch.08 - SL - Christensen 12eRyan NguyenNo ratings yet

- ACG4940 - Spring 2020Document9 pagesACG4940 - Spring 2020Ryan NguyenNo ratings yet

- 016 JockstrapDocument1 page016 JockstrapRyan NguyenNo ratings yet

- ACG 3113 Syllabus s601 Fall 2019Document10 pagesACG 3113 Syllabus s601 Fall 2019Ryan NguyenNo ratings yet

- Shields Investment 2019Document3 pagesShields Investment 2019Ryan Nguyen0% (2)

- CFL1619 CourseDocument64 pagesCFL1619 CourseRyan NguyenNo ratings yet

- Ryan Nguyen ResumeDocument1 pageRyan Nguyen ResumeRyan NguyenNo ratings yet

- Revival eDocument50 pagesRevival eRyan NguyenNo ratings yet

- Chap 001 MRDocument34 pagesChap 001 MRRyan NguyenNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument17 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancekartikraviraj2No ratings yet

- Practice CF Scooter KeyDocument4 pagesPractice CF Scooter KeyAllie LinNo ratings yet

- Current & Saving Account Statement: Khurshid Alam S/O Amirul Hasan Ansari Vill Po Hatta Ps Chainpur Distt Kaimur BhabhuaDocument5 pagesCurrent & Saving Account Statement: Khurshid Alam S/O Amirul Hasan Ansari Vill Po Hatta Ps Chainpur Distt Kaimur BhabhuaKhurshid AlamNo ratings yet

- Mobile Services: Your Account Summary This Month'S ChargesDocument2 pagesMobile Services: Your Account Summary This Month'S ChargesRoushanKumarAbaperNo ratings yet

- "Chapter VI Transitory and Miscellaneous ProvisionsDocument2 pages"Chapter VI Transitory and Miscellaneous ProvisionsthebeautyinsideNo ratings yet

- Your Quarterly Bill: How To PayDocument2 pagesYour Quarterly Bill: How To PayPaul Climas100% (1)

- The Study of Implementation of GST and I PDFDocument9 pagesThe Study of Implementation of GST and I PDFAsma KhanNo ratings yet

- Vat 220-223-224Document2 pagesVat 220-223-224timotheoigogo100% (1)

- Hardwick Enterprises Is Evaluating Alternative Uses For A Three Story ManufacturingDocument1 pageHardwick Enterprises Is Evaluating Alternative Uses For A Three Story Manufacturingtrilocksp SinghNo ratings yet

- Bank One - Mauritius - Tariffs and Charges GuideDocument1 pageBank One - Mauritius - Tariffs and Charges GuidedoegoodNo ratings yet

- RR 2 - 98 As AmendedDocument130 pagesRR 2 - 98 As AmendedHB AldNo ratings yet

- Income Taxation NotesDocument45 pagesIncome Taxation NotesIlonah HizonNo ratings yet

- Postbank Good To Know Current AccountDocument7 pagesPostbank Good To Know Current AccountClement KankuNo ratings yet

- Study On Payment BankDocument65 pagesStudy On Payment BankMukesh MauryaNo ratings yet

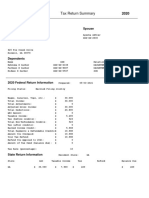

- Tax Return 2020Document27 pagesTax Return 2020Sadman Sakib Tazwar100% (1)

- ds4194 PDFDocument3 pagesds4194 PDFBen DzhonsNo ratings yet

- Section 44AD (Practical)Document43 pagesSection 44AD (Practical)fintech ConsultancyNo ratings yet

- Ibs Seksyen 18, Shah Alam 1 30/09/22Document3 pagesIbs Seksyen 18, Shah Alam 1 30/09/22Hamdan Abu BakarNo ratings yet

- Battle For A BargainDocument2 pagesBattle For A Bargainapi-457882816No ratings yet

- Hope Kinderland Daycare Centre InvoiceDocument2 pagesHope Kinderland Daycare Centre InvoiceshafiqhqalNo ratings yet

- Juliet Apparels Pvt. LTDDocument1 pageJuliet Apparels Pvt. LTDraj sahil100% (1)

- Sample Questions On WTWDocument1 pageSample Questions On WTWBaldovino VenturesNo ratings yet

- St. Aloysius College: (Autonomous) Affiliated To Rani Durgawati Vishwavidhyalaya, Jabalpur (M.P.)Document10 pagesSt. Aloysius College: (Autonomous) Affiliated To Rani Durgawati Vishwavidhyalaya, Jabalpur (M.P.)Abhishek AroraNo ratings yet

- Form 16-2223Document5 pagesForm 16-2223Arthur JosephNo ratings yet

- BIR Ruling (DA - (IL-045) 516-08)Document7 pagesBIR Ruling (DA - (IL-045) 516-08)Jerwin DaveNo ratings yet

- TINA Bank StatementDocument2 pagesTINA Bank Statementmohamed elmakhzniNo ratings yet

- Stayzilla Rate Sheet: Signed On Behalf of Stayzilla: Signed On Behalf of HotelDocument2 pagesStayzilla Rate Sheet: Signed On Behalf of Stayzilla: Signed On Behalf of HotelAbdulrahim SanthuNo ratings yet

- MTC - 40Document14 pagesMTC - 40Anonymous eCUVunlzKaNo ratings yet

- Typesof ClearingDocument3 pagesTypesof Clearingteliumar100% (1)