0% found this document useful (0 votes)

534 viewsRevision Notes Group Accounts PDF

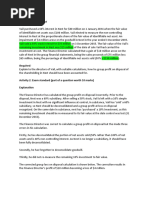

The document provides definitions and guidance on group accounts, subsidiaries, associates, and joint ventures. A group comprises a parent and at least one subsidiary. A subsidiary is consolidated using acquisition accounting so the parent and subsidiaries are presented as a single economic entity. Control of a subsidiary requires power over it, exposure to variable returns, and the ability to affect returns. Associates are entities with significant influence, not control, over financial and operating policies. Joint ventures require joint control over arrangements with rights to net assets.

Uploaded by

EhsanulCopyright

© © All Rights Reserved

Available Formats

Download as PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

534 viewsRevision Notes Group Accounts PDF

The document provides definitions and guidance on group accounts, subsidiaries, associates, and joint ventures. A group comprises a parent and at least one subsidiary. A subsidiary is consolidated using acquisition accounting so the parent and subsidiaries are presented as a single economic entity. Control of a subsidiary requires power over it, exposure to variable returns, and the ability to affect returns. Associates are entities with significant influence, not control, over financial and operating policies. Joint ventures require joint control over arrangements with rights to net assets.

Uploaded by

EhsanulCopyright

© © All Rights Reserved

Available Formats

Download as PDF, TXT or read online on Scribd

/ 11