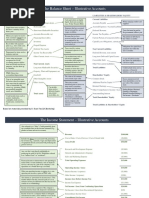

Accounting: Assets Liabilities + Equity A L + E

Accounting: Assets Liabilities + Equity A L + E

Download as docx, pdf, or txt

You might also like

- Chart of Accounts For Small Business Template V 1.0Document3 pagesChart of Accounts For Small Business Template V 1.0Siva Naga Prasad TadipartiNo ratings yet

- CJC Jensen Filter - ManualDocument73 pagesCJC Jensen Filter - Manualbrunokfouri40% (5)

- Non-VAT Goods Chart of AccountsDocument13 pagesNon-VAT Goods Chart of AccountsJenny BernardinoNo ratings yet

- Inbm 110 - Accounts Study Sheet: Chapter 1 & 2Document5 pagesInbm 110 - Accounts Study Sheet: Chapter 1 & 2Laura Tai100% (1)

- Heywood Chapter 3 NotesDocument7 pagesHeywood Chapter 3 NotesCath ;100% (2)

- Account ClassificationDocument3 pagesAccount ClassificationUsama Mukhtar100% (2)

- Accounting Journal Entries Flowchart PDFDocument1 pageAccounting Journal Entries Flowchart PDFMary71% (7)

- Accounting TransactionsDocument28 pagesAccounting TransactionsPaolo100% (1)

- 4 Chart of AccountsDocument115 pages4 Chart of Accountsresti rahmawatiNo ratings yet

- Account ClassificationDocument2 pagesAccount ClassificationAzeemAkram100% (2)

- Bench - Co Income Statement Excel TemplateDocument31 pagesBench - Co Income Statement Excel TemplateMay CañebaNo ratings yet

- The Basic Process in Recording TransactionsDocument13 pagesThe Basic Process in Recording TransactionsJoseph LimbongNo ratings yet

- Hot Desert Case Study - Sahara DesertDocument1 pageHot Desert Case Study - Sahara DesertCamilleNo ratings yet

- Summary of Accounting Basics PDFDocument4 pagesSummary of Accounting Basics PDFEmille YuloNo ratings yet

- Basic Financial Accounting Notes.Document6 pagesBasic Financial Accounting Notes.Babar AbbasNo ratings yet

- Basic Financial Accounting Notes Very Helpfull Must SeeDocument5 pagesBasic Financial Accounting Notes Very Helpfull Must SeeBabar AbbasNo ratings yet

- Double Entry Accounting Exercise Workbook Bookkeeping Cases Free PDFDocument139 pagesDouble Entry Accounting Exercise Workbook Bookkeeping Cases Free PDFayiahNo ratings yet

- Posting, Adjusting Entries, Process of Doing A 10-Columnar Worksheets, Closing Entries For Service Type of BusinessDocument18 pagesPosting, Adjusting Entries, Process of Doing A 10-Columnar Worksheets, Closing Entries For Service Type of BusinessRalphjoseph Tuazon100% (1)

- Excel Skills - Basic Accounting Template: InstructionsDocument39 pagesExcel Skills - Basic Accounting Template: InstructionsStorage Bank100% (1)

- Dr. Domingo Clinic Chart of Accounts: Account Numbers Account Titles Current AssetsDocument2 pagesDr. Domingo Clinic Chart of Accounts: Account Numbers Account Titles Current AssetsmariaNo ratings yet

- Formula Business FinanceDocument1 pageFormula Business FinanceRonald CatapangNo ratings yet

- Chart of AccountsDocument4 pagesChart of AccountsVu LuongNo ratings yet

- Bookkeeping Practice SetDocument16 pagesBookkeeping Practice SeteugNo ratings yet

- Accounting Adjusting EntryDocument20 pagesAccounting Adjusting EntryClemencia Masiba100% (1)

- Adjusting EntriesDocument7 pagesAdjusting EntriesJon Pangilinan100% (1)

- Midterm Cheat SheetDocument4 pagesMidterm Cheat SheetvikasNo ratings yet

- Financial Statements For A Sole Proprietorship: Accounting Chapter 7Document22 pagesFinancial Statements For A Sole Proprietorship: Accounting Chapter 7Nur SiaNo ratings yet

- Chart of Accounts ExplanationDocument9 pagesChart of Accounts Explanationellapot89No ratings yet

- Chapter 2 Review Sheet AnswersDocument7 pagesChapter 2 Review Sheet AnswersKenneth DayohNo ratings yet

- Analysis of Financial StatementsDocument80 pagesAnalysis of Financial Statementsmano cherian mathew100% (1)

- Accounting Journal Entries With Business TransactionsDocument7 pagesAccounting Journal Entries With Business TransactionsMhel DemabogteNo ratings yet

- Cost of Goods Sold WorksheetDocument4 pagesCost of Goods Sold Worksheetbutch listangco100% (1)

- Mr. Addams' EditingDocument15 pagesMr. Addams' EditingKim KoalaNo ratings yet

- Accounting CycleDocument12 pagesAccounting CycleHarjinder Singh100% (1)

- Basic Accounting EquationDocument17 pagesBasic Accounting EquationArienaya100% (1)

- Financial Accounting 3Document47 pagesFinancial Accounting 3Roxana Istrate100% (1)

- The Balance SheetDocument14 pagesThe Balance SheetHeherson CustodioNo ratings yet

- ACCTG 1 Week 2-3 - Accounting in BusinessDocument13 pagesACCTG 1 Week 2-3 - Accounting in BusinessReygie FabrigaNo ratings yet

- Adjusting Entries Chapter $Document56 pagesAdjusting Entries Chapter $Arzan AliNo ratings yet

- Accounting Adjustment-Accrued & PrepaidDocument30 pagesAccounting Adjustment-Accrued & PrepaidEida HidayahNo ratings yet

- 2016 14 PPT Acctg1 Adjusting EntriesDocument20 pages2016 14 PPT Acctg1 Adjusting Entriesash wu100% (3)

- Balance Sheet Income StatementDocument2 pagesBalance Sheet Income StatementKamaljit Singh100% (1)

- ACC1002X Cheat Sheet 2Document1 pageACC1002X Cheat Sheet 2jieboNo ratings yet

- Basic Accounting EquationDocument3 pagesBasic Accounting EquationMaria Charise Tongol100% (1)

- Classification of AccountsDocument3 pagesClassification of AccountsSaurav Aradhana100% (3)

- Closing EntriesDocument14 pagesClosing EntriesAlbert Moreno100% (1)

- 1.-Bookkeeping (1) LessonDocument25 pages1.-Bookkeeping (1) LessonRodel Carreon Candelaria100% (1)

- Step 1 - Transactions And/or EventsDocument5 pagesStep 1 - Transactions And/or EventsJEFFREY GALANZA0% (1)

- Accounting Cycle, Entries and ConceptDocument64 pagesAccounting Cycle, Entries and Conceptdude devil100% (1)

- Purchase Journal and Accounts Payable Subsidiary LedgerDocument4 pagesPurchase Journal and Accounts Payable Subsidiary LedgerMary100% (6)

- Periodic and Perpetual Inventory System ComparedDocument2 pagesPeriodic and Perpetual Inventory System Comparedkim aeong100% (2)

- Chart of AccountDocument5 pagesChart of Accountsana82966534100% (1)

- Accounting 101 Sample ExercisesDocument12 pagesAccounting 101 Sample ExercisesFloidette JimenezNo ratings yet

- Chart of Accounts For Small Business Template V 1.1Document3 pagesChart of Accounts For Small Business Template V 1.1Zubair Alam100% (1)

- Basis of Debit and CreditDocument17 pagesBasis of Debit and CreditBanaras KhanNo ratings yet

- Adjusting Entries - Theory #4Document27 pagesAdjusting Entries - Theory #4Rae Antonette Solana100% (1)

- Accounting Terms & DefinitionsDocument5 pagesAccounting Terms & DefinitionsMa Glenda Brequillo SañgaNo ratings yet

- Chapter 4 AccountingDocument22 pagesChapter 4 AccountingChan Man SeongNo ratings yet

- Accounting Cycle of A Merchandising BusinessDocument31 pagesAccounting Cycle of A Merchandising BusinessAresta, Novie Mae100% (1)

- Accounts Payable Job Interview Preparation GuideDocument15 pagesAccounts Payable Job Interview Preparation GuideHarshSuri0% (1)

- What Is Bank Reconciliation.Document11 pagesWhat Is Bank Reconciliation.Sabrena FennaNo ratings yet

- QuickBooks Online for Beginners: The Step by Step Guide to Bookkeeping and Financial Accounting for Small Businesses and FreelancersFrom EverandQuickBooks Online for Beginners: The Step by Step Guide to Bookkeeping and Financial Accounting for Small Businesses and FreelancersNo ratings yet

- Accounting: Assets Liabilities + Equity A L + EDocument4 pagesAccounting: Assets Liabilities + Equity A L + EJohn LeeNo ratings yet

- SEG3101-Ch3-2 - Requirements Documentation Standards - IEEE830Document18 pagesSEG3101-Ch3-2 - Requirements Documentation Standards - IEEE830Mohammed AlshamiNo ratings yet

- Csc443 Test 2Document13 pagesCsc443 Test 2muhammad ali imranNo ratings yet

- Types and Applications of MaterialsDocument53 pagesTypes and Applications of MaterialsGeno Martinez100% (1)

- Srs On Online Booking System PDFDocument9 pagesSrs On Online Booking System PDFZeeshan AbbasNo ratings yet

- Business Policy Activity 2Document3 pagesBusiness Policy Activity 2Motopatz BrionesNo ratings yet

- I3 Module 1Document2 pagesI3 Module 1jaylordyoNo ratings yet

- Contest Sweepstakes Rules-Garth Brooks Contest Ticket GiveawayDocument6 pagesContest Sweepstakes Rules-Garth Brooks Contest Ticket GiveawayKBTX100% (1)

- Rural Marketing of Hero HondaDocument41 pagesRural Marketing of Hero HondaAJAYNo ratings yet

- Exploiting Software How To Break Code PDFDocument2 pagesExploiting Software How To Break Code PDFShantelNo ratings yet

- Twofold Magazine - Issue 20 - AdvertisingDocument14 pagesTwofold Magazine - Issue 20 - AdvertisingMaryNo ratings yet

- Piston Ring ManfDocument3 pagesPiston Ring ManfMahesh AtyaleNo ratings yet

- Cold Chain TransportationDocument6 pagesCold Chain TransportationGokul David100% (1)

- Optimal FX Market Making Under Inventory Risk and Adverse Selection ConstraintsDocument12 pagesOptimal FX Market Making Under Inventory Risk and Adverse Selection ConstraintsJose Antonio Dos RamosNo ratings yet

- Charge of Income TaxDocument7 pagesCharge of Income TaxYuvi SinghNo ratings yet

- Mod Menu Log - Com - Tencent.igliteDocument30 pagesMod Menu Log - Com - Tencent.iglitemdabir44567No ratings yet

- Residential StatusDocument7 pagesResidential StatusquickcabitesNo ratings yet

- Valvulas Watts PDFDocument140 pagesValvulas Watts PDFJuan PerazaNo ratings yet

- Wa0018 Compressed CompressedDocument1 pageWa0018 Compressed CompressedShaik RahamanNo ratings yet

- Netflix Pengantar ManajemenDocument1 pageNetflix Pengantar ManajemenAisyah muthmainnahNo ratings yet

- San Miguel Foundation Monitoring SystemDocument89 pagesSan Miguel Foundation Monitoring SystemMio Betty J. MebolosNo ratings yet

- Imo Bunker ConventionDocument16 pagesImo Bunker Conventionpari2005No ratings yet

- Role Play T The AirportDocument1 pageRole Play T The AirportRosa GuindosNo ratings yet

- OBS - Online Banking System SynopsisDocument2 pagesOBS - Online Banking System SynopsisMajidNo ratings yet

- Historical Records of Survey of India Vol 3 by Col R H PhillimoreDocument590 pagesHistorical Records of Survey of India Vol 3 by Col R H PhillimoreSonam Gyamtso100% (3)

- Agpalo Notes - Statutory Construction, CH 5Document2 pagesAgpalo Notes - Statutory Construction, CH 5Chi Koy100% (3)

- Manual of Examination Automation SystemDocument11 pagesManual of Examination Automation SystemSabha NayaghamNo ratings yet

- MetroDocument3 pagesMetroAnonymous oZNS7QuAdNo ratings yet