0% found this document useful (0 votes)

1K viewsFABM2 Module 5 - FS Analysis

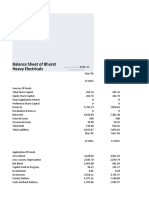

This document provides lecture notes on analyzing financial statements through horizontal analysis, vertical analysis, and calculating financial ratios. It defines the different types of financial statement analysis, provides examples of how to conduct horizontal and vertical analysis, and defines common financial ratios like gross profit ratio, operating income ratio, and debt-to-equity ratio. The document includes an illustrative problem using sample financial statement data from Dina Eng's Company to demonstrate how to compute various ratios.

Uploaded by

Kimberly Abella CabreraCopyright

© © All Rights Reserved

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

1K viewsFABM2 Module 5 - FS Analysis

This document provides lecture notes on analyzing financial statements through horizontal analysis, vertical analysis, and calculating financial ratios. It defines the different types of financial statement analysis, provides examples of how to conduct horizontal and vertical analysis, and defines common financial ratios like gross profit ratio, operating income ratio, and debt-to-equity ratio. The document includes an illustrative problem using sample financial statement data from Dina Eng's Company to demonstrate how to compute various ratios.

Uploaded by

Kimberly Abella CabreraCopyright

© © All Rights Reserved

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

/ 11