0% found this document useful (0 votes)

42 viewsBachelor of Administration (Hons) in Islamic Finance: Islamic Financial Products and Services EBB20503 (IF10)

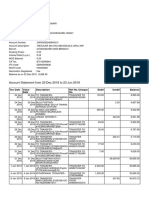

This document contains information about a final assessment submission for a Bachelor of Administration (Hons) in Islamic Finance program. The submission date is June 16, 2020 and it was prepared by Zul Irfan Hazim Bin Sururi for Wan Muhd Nasrul Hadi Bin Wan Abdul Aziz. The document discusses potential financial products and services that could be offered to or customized for two customers, Mr. Nasrul and Mr. Hadi, to improve their customer relationship and portfolio management.

Uploaded by

irfan sururiCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

42 viewsBachelor of Administration (Hons) in Islamic Finance: Islamic Financial Products and Services EBB20503 (IF10)

This document contains information about a final assessment submission for a Bachelor of Administration (Hons) in Islamic Finance program. The submission date is June 16, 2020 and it was prepared by Zul Irfan Hazim Bin Sururi for Wan Muhd Nasrul Hadi Bin Wan Abdul Aziz. The document discusses potential financial products and services that could be offered to or customized for two customers, Mr. Nasrul and Mr. Hadi, to improve their customer relationship and portfolio management.

Uploaded by

irfan sururiCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

/ 6