K Discussion Questions (3 Points Each)

K Discussion Questions (3 Points Each)

Download as docx, pdf, or txt

You might also like

- Extended Withholding Tax Configuration - SAP FIDocument18 pagesExtended Withholding Tax Configuration - SAP FInaysarNo ratings yet

- Should People Be Encouraged by The Government To Always Maintain Sustainable and Environmentally-Friendly Lifestyle?Document1 pageShould People Be Encouraged by The Government To Always Maintain Sustainable and Environmentally-Friendly Lifestyle?Glezer NiezNo ratings yet

- JE, GL, TB - Ace BarbershopDocument14 pagesJE, GL, TB - Ace BarbershopJasmine ActaNo ratings yet

- Mid Term IDocument10 pagesMid Term Ichaos1989No ratings yet

- The Impact of School Bullying On Students Academic Achievement From Teachers Point of View Prepared by Dr. Hana Khaled Al - RaqqadDocument17 pagesThe Impact of School Bullying On Students Academic Achievement From Teachers Point of View Prepared by Dr. Hana Khaled Al - RaqqadTeam BEE100% (4)

- Chapter 1 Introduction To Taxation: Chapter Overview and ObjectivesDocument30 pagesChapter 1 Introduction To Taxation: Chapter Overview and ObjectivesNoeme LansangNo ratings yet

- DISCUSSION QUESTIONS - Income Taxation Chap 1Document2 pagesDISCUSSION QUESTIONS - Income Taxation Chap 1Vivienne Rozenn LaytoNo ratings yet

- Chapter 3 MotivationDocument193 pagesChapter 3 MotivationAndra GrigoreNo ratings yet

- Good Gov 7-9 With Q&ADocument74 pagesGood Gov 7-9 With Q&AJoshua JunsayNo ratings yet

- Tax Vs TollDocument4 pagesTax Vs TollKris Joseph LasayNo ratings yet

- Chapt-7 Dealings in PropDocument14 pagesChapt-7 Dealings in Prophumnarvios0% (1)

- Operations MGT Module #8Document3 pagesOperations MGT Module #8Jude VicenteNo ratings yet

- You Are at YourDocument1 pageYou Are at YourPrince SanjiNo ratings yet

- Chapter 11Document50 pagesChapter 11Randi ZamrajjasaNo ratings yet

- Oblicon Reviewer Chapter 1Document9 pagesOblicon Reviewer Chapter 1Carlos Hidalgo100% (1)

- Chapter 3Document12 pagesChapter 3geexellNo ratings yet

- Advantage and Disadvantages of Business OrganizationDocument3 pagesAdvantage and Disadvantages of Business OrganizationJustine VeralloNo ratings yet

- Approved CAE - BSA BSMA BSAIS BSIA - ACC 311 - Clarito - Page-0055-0064Document17 pagesApproved CAE - BSA BSMA BSAIS BSIA - ACC 311 - Clarito - Page-0055-0064Peng GuinNo ratings yet

- Chapter 13-A DraftDocument29 pagesChapter 13-A DraftRouve BontuyanNo ratings yet

- Regular Income TaxationDocument6 pagesRegular Income TaxationAnabel Lajara Angeles0% (1)

- HRM Case Study - Red - LobsterDocument1 pageHRM Case Study - Red - Lobsteramitbharadwaj70% (1)

- Siena College of Taytay Inc. Taxation 1 - Income Taxation College of Business and AccountancyDocument2 pagesSiena College of Taytay Inc. Taxation 1 - Income Taxation College of Business and AccountancyDonnan OreaNo ratings yet

- Bam 199 - Quiz#1 - 03062021Document26 pagesBam 199 - Quiz#1 - 03062021NeighvestNo ratings yet

- Cooperative Organization and Practical Applications (COOP 20073)Document2 pagesCooperative Organization and Practical Applications (COOP 20073)ErianneNo ratings yet

- Assessment On The Practice of Corporate Social ResponsibilityDocument12 pagesAssessment On The Practice of Corporate Social ResponsibilityJayson Tom Briva Capaz100% (1)

- AEC12 - Governance, Business Ethics, Risk Management and Internal ControlDocument1 pageAEC12 - Governance, Business Ethics, Risk Management and Internal ControlRhea May BaluteNo ratings yet

- I. Physically Impossible ConditionDocument8 pagesI. Physically Impossible Conditionleshz zynNo ratings yet

- FAR LT1 Answer KeyDocument5 pagesFAR LT1 Answer KeypehikNo ratings yet

- RRL ProgressedDocument14 pagesRRL ProgressedMonique100% (1)

- Philippine Accounting Standard (PAS) 1: Presentation of Financial StatementsDocument30 pagesPhilippine Accounting Standard (PAS) 1: Presentation of Financial StatementsJhon Cydric TiosaycoNo ratings yet

- Tata SeloDocument4 pagesTata SeloMoon Min RaNo ratings yet

- BAM 127 Day 7 - TGDocument11 pagesBAM 127 Day 7 - TGPaulo BelenNo ratings yet

- Various Entry Strategies Used by Firms To Initiate International Business ActivityDocument14 pagesVarious Entry Strategies Used by Firms To Initiate International Business Activitymvlg26No ratings yet

- Task PerformanceDocument4 pagesTask PerformanceAngelica CaesarNo ratings yet

- Tax - Post Test 1&2Document2 pagesTax - Post Test 1&2lena cpaNo ratings yet

- Which Is Subject To FINAL TAXDocument1 pageWhich Is Subject To FINAL TAXbutterfly kisses0217No ratings yet

- Lim Tong Lim v. Phil Fishing Gear IndustriesDocument10 pagesLim Tong Lim v. Phil Fishing Gear IndustriesPatrick Jorge SibayanNo ratings yet

- Orge University. AnjieDocument4 pagesOrge University. AnjieKim Kyun SiNo ratings yet

- 3.1 Nature of Cost, Cost Pools, Cost Objects, and Cost DriversDocument6 pages3.1 Nature of Cost, Cost Pools, Cost Objects, and Cost Driverslang droidNo ratings yet

- BAM 127 Day 11 - TGDocument8 pagesBAM 127 Day 11 - TGPaulo BelenNo ratings yet

- ANSWER Midterm Financial ManagementDocument3 pagesANSWER Midterm Financial ManagementSymon EsagaNo ratings yet

- The Philippine Banking SystemDocument2 pagesThe Philippine Banking Systemthephantom096No ratings yet

- Tax 1 - GPDocument7 pagesTax 1 - GPJayson ChanNo ratings yet

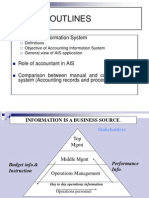

- Chapter 1: Introduction To AISDocument29 pagesChapter 1: Introduction To AISFatiha YusofNo ratings yet

- Week 8 Scope and Taxation Reforms of The PhilippinesDocument4 pagesWeek 8 Scope and Taxation Reforms of The PhilippinesAngie Olpos Boreros BaritugoNo ratings yet

- 2021 Audited Financial Statement of Puregold Price Club Inc Parent 1 111021Document64 pages2021 Audited Financial Statement of Puregold Price Club Inc Parent 1 111021Merille Vasquez100% (1)

- Chapter 7 Economic Dev'tDocument6 pagesChapter 7 Economic Dev'tmonique payong100% (2)

- Eco - ReviewerDocument7 pagesEco - ReviewerKRISTINA CASSANDRA CUEVASNo ratings yet

- Unfair Labor Practices in Nutri Asia Post Pandemic RemediesDocument24 pagesUnfair Labor Practices in Nutri Asia Post Pandemic RemediesGiella MagnayeNo ratings yet

- TaxationDocument13 pagesTaxationEmperiumNo ratings yet

- Burundi - Reaction Paper PDFDocument2 pagesBurundi - Reaction Paper PDFThird MontefalcoNo ratings yet

- Toaz - Info Chapter 10 Compensation Income True or False 1 PRDocument22 pagesToaz - Info Chapter 10 Compensation Income True or False 1 PRErna DavidNo ratings yet

- Specialized Government BanksDocument5 pagesSpecialized Government BanksCarazelli A. FurigayNo ratings yet

- Introduction To Global Finance With Electronic 1 BankingDocument4 pagesIntroduction To Global Finance With Electronic 1 Bankingcharlenealvarez59No ratings yet

- Business Transactions Their Analysis With Answers by AlagangwencyDocument4 pagesBusiness Transactions Their Analysis With Answers by AlagangwencyHello KittyNo ratings yet

- Which of The Following Is The Correct Tax Implication of The Foregoing Data With Respect To Payment of Income Tax?Document3 pagesWhich of The Following Is The Correct Tax Implication of The Foregoing Data With Respect To Payment of Income Tax?ROSEMARIE CRUZNo ratings yet

- Term Exam Essay PartDocument1 pageTerm Exam Essay PartCristine Jewel CorpuzNo ratings yet

- BMGT 28 Lesson 1Document8 pagesBMGT 28 Lesson 1gerome llagasNo ratings yet

- Discussion QuestionsDocument7 pagesDiscussion QuestionsPoison IvyNo ratings yet

- Fundamental Principles of TaxationDocument115 pagesFundamental Principles of TaxationDoren Joy BatucanNo ratings yet

- Portfolio: Results-Based Performance Management System (RPMS) School Year 2020-2021Document6 pagesPortfolio: Results-Based Performance Management System (RPMS) School Year 2020-2021Team BEENo ratings yet

- Natural Number-Exponential FunctionDocument13 pagesNatural Number-Exponential FunctionTeam BEENo ratings yet

- The Role of Visual and Non-Visual Information in The Control of LocomotionDocument35 pagesThe Role of Visual and Non-Visual Information in The Control of LocomotionTeam BEENo ratings yet

- ISBN-1-564'99-026-5 95 177p. Valley,: Help Teachers Instill Moral Values DeliberatelyDocument177 pagesISBN-1-564'99-026-5 95 177p. Valley,: Help Teachers Instill Moral Values DeliberatelyTeam BEENo ratings yet

- Role of Teachers in Inculcating Values Among Students c1256Document6 pagesRole of Teachers in Inculcating Values Among Students c1256Team BEENo ratings yet

- Value Inculcation Through Co-Curricular Co-Scholastic Activities in School StudentsDocument4 pagesValue Inculcation Through Co-Curricular Co-Scholastic Activities in School StudentsTeam BEE0% (1)

- Visual Information and MediaDocument2 pagesVisual Information and MediaTeam BEENo ratings yet

- Lab3Handout Osmosis PDFDocument4 pagesLab3Handout Osmosis PDFTeam BEENo ratings yet

- 3 ProteinsDocument42 pages3 ProteinsTeam BEENo ratings yet

- Read Me (Tolong Dibaca, Panduan Template Project)Document1 pageRead Me (Tolong Dibaca, Panduan Template Project)Team BEENo ratings yet

- Lesson 2: Muscle and Bone Activities For A Stronger BodyDocument8 pagesLesson 2: Muscle and Bone Activities For A Stronger BodyTeam BEENo ratings yet

- Zone 6, Poblacion Poblacion, Lantapan, 8722Document2 pagesZone 6, Poblacion Poblacion, Lantapan, 8722Team BEENo ratings yet

- Advantages of Taking Up Stem in Senior High School: Preparation For CollegeDocument45 pagesAdvantages of Taking Up Stem in Senior High School: Preparation For CollegeTeam BEE100% (1)

- Part - I (MCQS) All Mcqs Are Compulsory: Permission Is Punishable OffenceDocument12 pagesPart - I (MCQS) All Mcqs Are Compulsory: Permission Is Punishable OffenceShashwat SharmaNo ratings yet

- Tax Exemption LetterDocument1 pageTax Exemption Letterprem_k_sNo ratings yet

- Deduction PDFDocument207 pagesDeduction PDFdeepluthra6No ratings yet

- Personal Tax ChecklistDocument4 pagesPersonal Tax Checklistben.hoangNo ratings yet

- Ast TX 901 Fringe Benefits Tax (Batch 22)Document8 pagesAst TX 901 Fringe Benefits Tax (Batch 22)Julious CaalimNo ratings yet

- Chapter9-Accounting For LaborDocument46 pagesChapter9-Accounting For LaborNashaNo ratings yet

- Donors' Tax (NA)Document6 pagesDonors' Tax (NA)Diane PascualNo ratings yet

- Misamis Oriental Association of Coco Traders VS DofDocument1 pageMisamis Oriental Association of Coco Traders VS DofCharles Roger RayaNo ratings yet

- Taxation Law MCQsDocument17 pagesTaxation Law MCQsNoemi Hill100% (1)

- Assignments-1 (IBF-SP-20-MBA-0041) Syed Anees AliDocument10 pagesAssignments-1 (IBF-SP-20-MBA-0041) Syed Anees AliSYED ANEES ALINo ratings yet

- Annex B-2 RR 11-2018Document1 pageAnnex B-2 RR 11-2018Kristine JoyceNo ratings yet

- Web Generated Bill: Feeder: Riffle Range Road (078109) Sub Division: D.H.A West Division: Defence DivDocument1 pageWeb Generated Bill: Feeder: Riffle Range Road (078109) Sub Division: D.H.A West Division: Defence DivSalim Ahmed Automoiles LahoreNo ratings yet

- Annex 37 - QSRP - CabangtalanDocument12 pagesAnnex 37 - QSRP - CabangtalanLikey PromiseNo ratings yet

- 2008 Sro 947Document3 pages2008 Sro 947Faheem ShaukatNo ratings yet

- Taxguru - in-TDS Rate Chart FY 2024-25 AY 2025-26Document5 pagesTaxguru - in-TDS Rate Chart FY 2024-25 AY 2025-26arifbaba678No ratings yet

- LU1 - Value-Added TaxDocument24 pagesLU1 - Value-Added Taxmandisanomzamo72No ratings yet

- Project On GSTDocument38 pagesProject On GSTGourav Pareek100% (1)

- Tax 1 CasesDocument625 pagesTax 1 CasesDence Cris RondonNo ratings yet

- Balance Sheet 2022Document4 pagesBalance Sheet 2022Llus NaruamNo ratings yet

- Sap Cin-MM Customizing For Tax Procedure - Taxinn: Hide TOCDocument7 pagesSap Cin-MM Customizing For Tax Procedure - Taxinn: Hide TOCsreekumarNo ratings yet

- Jio Broadband BillDocument3 pagesJio Broadband Billpoojendra2No ratings yet

- Cases For Feb 8Document13 pagesCases For Feb 8PJANo ratings yet

- Taxation Law - 2013 Dimaampao Lecture Notes PDFDocument90 pagesTaxation Law - 2013 Dimaampao Lecture Notes PDFPaul Joseph MercadoNo ratings yet

- Abhishek - Form 16Document2 pagesAbhishek - Form 16hrrecruiter.vhtbsNo ratings yet

- Tax Research MemoDocument7 pagesTax Research MemoalexNo ratings yet

- Debt & DeficitDocument6 pagesDebt & DeficitPreethi GopalanNo ratings yet

- Term Paper, Yohannes TesfayeDocument18 pagesTerm Paper, Yohannes TesfayeYohannes TesfayeNo ratings yet

- Fiscal Policy NotesDocument5 pagesFiscal Policy NotesJaydenausNo ratings yet

- RP-US Tax TreatyDocument36 pagesRP-US Tax TreatyCharles Augustine AlbañoNo ratings yet