0% found this document useful (0 votes)

52 viewsModule 1 Lesson 3

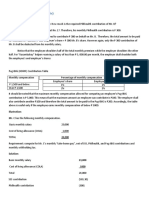

The document discusses donor's taxation in the Philippines, including donor's tax credit which allows deduction of taxes paid in the Philippines and foreign countries from donor's tax due. It provides examples to illustrate the computation of donor's tax payable and limitations on foreign tax credit.

Uploaded by

Rich Ann Redondo VillanuevaCopyright

© © All Rights Reserved

Available Formats

Download as PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

52 viewsModule 1 Lesson 3

The document discusses donor's taxation in the Philippines, including donor's tax credit which allows deduction of taxes paid in the Philippines and foreign countries from donor's tax due. It provides examples to illustrate the computation of donor's tax payable and limitations on foreign tax credit.

Uploaded by

Rich Ann Redondo VillanuevaCopyright

© © All Rights Reserved

Available Formats

Download as PDF, TXT or read online on Scribd

/ 6