Common and Preferred Stock Chapter 13.....

Common and Preferred Stock Chapter 13.....

Download as docx, pdf, or txt

At a glance

Powered by AI

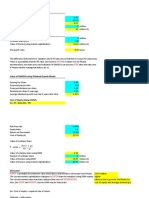

The key takeaways are the differences between common stock and preferred stock, how stockholders' equity is presented on the balance sheet, and how book value per share is calculated.

Common stockholders have voting rights and rights to dividends and liquidation proceeds, while preferred stockholders have preference over dividends and liquidation proceeds but no voting rights. Preferred stock may be cumulative or callable.

Stockholders' equity includes common stock, additional paid-in capital, retained earnings, and preferred stock. Treasury stock is deducted from stockholders' equity.

You might also like

- Asset Allocation 5E (PB): Balancing Financial Risk, Fifth EditionFrom EverandAsset Allocation 5E (PB): Balancing Financial Risk, Fifth EditionRating: 4 out of 5 stars4/5 (13)

- Certificate of Increase of Capital StockDocument2 pagesCertificate of Increase of Capital StockNarciso Reyes Jr.100% (6)

- Mahindra and Mahindra AnalysisDocument17 pagesMahindra and Mahindra Analysisrahul_raj198815220% (2)

- Ema Ge Berk CF 2GE SG 23Document12 pagesEma Ge Berk CF 2GE SG 23Sascha SaschaNo ratings yet

- Parallel LoansDocument6 pagesParallel LoansMurtaza HassanNo ratings yet

- Corporate Finance Ppt. SlideDocument24 pagesCorporate Finance Ppt. SlideMd. Jahangir Alam100% (1)

- Memorandum of UnderstandingDocument4 pagesMemorandum of UnderstandingDeepesh Mittal100% (1)

- Capital Market TerminologiesDocument4 pagesCapital Market Terminologiesnahid250100% (3)

- Introduction To Investment BankingDocument45 pagesIntroduction To Investment BankingNgọc Phan Thị BíchNo ratings yet

- Isbn6582-0 Ross ch24Document21 pagesIsbn6582-0 Ross ch24NurArianaNo ratings yet

- Convertible Bonds DefinitionsDocument3 pagesConvertible Bonds DefinitionsRocking LadNo ratings yet

- Capital Structure, The Determinants and FeaturesDocument5 pagesCapital Structure, The Determinants and FeaturesRianto StgNo ratings yet

- Introduction To Investment ManagementDocument11 pagesIntroduction To Investment ManagementAsif Abdullah KhanNo ratings yet

- Capital StructureDocument4 pagesCapital StructurenaveenngowdaNo ratings yet

- Title of The Paper:: Mergers and Acquisitions Financial ManagementDocument25 pagesTitle of The Paper:: Mergers and Acquisitions Financial ManagementfatinNo ratings yet

- Parity Conditions in International FinanceDocument68 pagesParity Conditions in International FinanceGaurav Kumar100% (2)

- Alternative InvestmentsDocument29 pagesAlternative InvestmentsIMOTEP100% (1)

- Financial Markets and InstitutionsDocument14 pagesFinancial Markets and InstitutionsHashir Khan100% (1)

- Financial InstitutionsDocument76 pagesFinancial InstitutionsGaurav Rathaur100% (1)

- Working Capital Finance Trade Credit, Bank Finance and Commercial PaperDocument105 pagesWorking Capital Finance Trade Credit, Bank Finance and Commercial PaperNishkushNo ratings yet

- Commercial Bank OperationsDocument20 pagesCommercial Bank OperationsPradnyesh GanuNo ratings yet

- Asset Backed SecuritiesDocument179 pagesAsset Backed SecuritiesShivani NidhiNo ratings yet

- Financial Accounting and Accounting StandardsDocument51 pagesFinancial Accounting and Accounting StandardsTapas GuptaNo ratings yet

- Leveraged Buyout (LBO) Private EquityDocument4 pagesLeveraged Buyout (LBO) Private EquityAmit Kumar RathNo ratings yet

- Financial Management QuestionsDocument3 pagesFinancial Management Questionsjagdish002No ratings yet

- Discussion QuestionsDocument19 pagesDiscussion QuestionsrahimNo ratings yet

- Evolution of Financial SystemDocument12 pagesEvolution of Financial SystemGautam JayasuryaNo ratings yet

- The Principle of Limited LiabilityDocument24 pagesThe Principle of Limited LiabilityMuhammad NumanNo ratings yet

- Quiz 2 - QUESTIONSDocument18 pagesQuiz 2 - QUESTIONSNaseer Ahmad AziziNo ratings yet

- CH - 04 Mutual Funds and Other Investment CompaniesDocument27 pagesCH - 04 Mutual Funds and Other Investment CompaniesshomudrokothaNo ratings yet

- Investment BankingDocument16 pagesInvestment BankingSudarshan DhavejiNo ratings yet

- ACCG871 Week 10 Financial Instruments (Autosaved)Document27 pagesACCG871 Week 10 Financial Instruments (Autosaved)Sophie DaoNo ratings yet

- Capital MarketDocument26 pagesCapital MarkethimanshusangaNo ratings yet

- Bond MarketDocument29 pagesBond MarketShintia Ayu PermataNo ratings yet

- Financial Crisis 2008Document59 pagesFinancial Crisis 2008007rumana9306100% (7)

- Teaching Notes-FMI-342 PDFDocument162 pagesTeaching Notes-FMI-342 PDFArun PatelNo ratings yet

- Preferred Stock Primer 2009Document9 pagesPreferred Stock Primer 2009oliverzzeng1152No ratings yet

- Debt RatioDocument7 pagesDebt RatioAamir BilalNo ratings yet

- Banking & Financial Markets: Bülent ŞenverDocument73 pagesBanking & Financial Markets: Bülent ŞenverjamesburdenNo ratings yet

- Finance Terms DefinitionDocument1 pageFinance Terms DefinitionMaheish AyyerNo ratings yet

- Consolidation or Business CombinationsDocument17 pagesConsolidation or Business CombinationsTimothy Kawuma100% (1)

- Capital Structure and Dividend TheoriesDocument16 pagesCapital Structure and Dividend Theoriesmusa_scorpionNo ratings yet

- Syllabus BANK-MANAGEMENT-AND-FINANCIAL-SERVICES-huytpDocument8 pagesSyllabus BANK-MANAGEMENT-AND-FINANCIAL-SERVICES-huytpPhạm Thúy HằngNo ratings yet

- Asset Classes and Financial InstrumentsDocument33 pagesAsset Classes and Financial Instrumentskaylakshmi8314No ratings yet

- Hybrid Finance - EssayDocument6 pagesHybrid Finance - EssayMalina TatarovaNo ratings yet

- Chapter Three: Financial Instruments, Financial Markets, and Financial InstitutionsDocument62 pagesChapter Three: Financial Instruments, Financial Markets, and Financial InstitutionsE-man HuckymNo ratings yet

- Mutual Funds and Other Investment Companies (Lecture Notes) PDFDocument8 pagesMutual Funds and Other Investment Companies (Lecture Notes) PDFNgọc Phan Thị BíchNo ratings yet

- Investment PhilosophyDocument5 pagesInvestment PhilosophyDan KumagaiNo ratings yet

- Bond RatingsDocument2 pagesBond RatingscciesaadNo ratings yet

- Managing Financial Resources and DecisionsDocument11 pagesManaging Financial Resources and DecisionsangelomercedeblogNo ratings yet

- Lecture 1 - Introduction of Financial ManagementDocument18 pagesLecture 1 - Introduction of Financial ManagementMaazNo ratings yet

- Advantages and Disadvantages of Preferred StockDocument5 pagesAdvantages and Disadvantages of Preferred StockVaibhav Rolihan100% (2)

- AC301 Off Balance Sheet FinancingDocument25 pagesAC301 Off Balance Sheet Financinghui7411No ratings yet

- Analyzing A Bank's Financial StatementsDocument8 pagesAnalyzing A Bank's Financial StatementsMinh Thu Nguyen100% (1)

- Agency Theory Suggests That The Firm Can Be Viewed As A Nexus of ContractsDocument5 pagesAgency Theory Suggests That The Firm Can Be Viewed As A Nexus of ContractsMilan RathodNo ratings yet

- Company Accounts: - in Law, Company' Is Termed As An Entity Which Is Formed andDocument9 pagesCompany Accounts: - in Law, Company' Is Termed As An Entity Which Is Formed andAnshul BajpaiNo ratings yet

- CH 15Document86 pagesCH 15saadsaaidNo ratings yet

- Chap 006Document51 pagesChap 006kel458100% (1)

- Critical Financial Review: Understanding Corporate Financial InformationFrom EverandCritical Financial Review: Understanding Corporate Financial InformationNo ratings yet

- Financial Fine Print: Uncovering a Company's True ValueFrom EverandFinancial Fine Print: Uncovering a Company's True ValueRating: 3 out of 5 stars3/5 (3)

- Notes HSEDocument59 pagesNotes HSEMuhammad AyazNo ratings yet

- Muhammad Ayaz: Roll Num 71 Topics Index Number, Introduction, Types, Uses and LimitationDocument7 pagesMuhammad Ayaz: Roll Num 71 Topics Index Number, Introduction, Types, Uses and LimitationMuhammad AyazNo ratings yet

- Common and Preferred StockDocument14 pagesCommon and Preferred StockMuhammad AyazNo ratings yet

- FA 1st AssignmentDocument6 pagesFA 1st AssignmentMuhammad AyazNo ratings yet

- Accounting Test For ClassDocument19 pagesAccounting Test For ClassMuhammad AyazNo ratings yet

- M Ayaz Sweet Peace BakeryDocument14 pagesM Ayaz Sweet Peace BakeryMuhammad AyazNo ratings yet

- Slide AKT 405 Teori Akuntansi 8 GodfreyDocument30 pagesSlide AKT 405 Teori Akuntansi 8 GodfreypietysantaNo ratings yet

- Manual Form Registered PV Service Providers DirectoryDocument7 pagesManual Form Registered PV Service Providers DirectoryKoh Siew KiemNo ratings yet

- Presentation Akuntansi Lanjutan II Chapter 2 Beams :: ConsolidationDocument21 pagesPresentation Akuntansi Lanjutan II Chapter 2 Beams :: ConsolidationAndreas JimanNo ratings yet

- Test Paper 11Document8 pagesTest Paper 11Sukhjinder SinghNo ratings yet

- Stock Market ForecastingDocument18 pagesStock Market ForecastingOm Prakash100% (1)

- Forest City Realty Trust Preliminary Proxy Document, Sept. 21, 2018Document223 pagesForest City Realty Trust Preliminary Proxy Document, Sept. 21, 2018Norman OderNo ratings yet

- DividendDocument11 pagesDividendManish KumarNo ratings yet

- CSR and Corporate GovernanceDocument13 pagesCSR and Corporate GovernanceArchana NeppolianNo ratings yet

- (042322) (Case 11) 9-1 Xytech, Inc.Document2 pages(042322) (Case 11) 9-1 Xytech, Inc.Michael SusenoNo ratings yet

- Chapter No 06 Final Afs-1Document58 pagesChapter No 06 Final Afs-1salwaburiroNo ratings yet

- Contoh Soal Mutual Holding Pendekatan KonvensionalDocument10 pagesContoh Soal Mutual Holding Pendekatan KonvensionalPutri ShaniaNo ratings yet

- Q&A InvestorDocument2 pagesQ&A Investorjns1992No ratings yet

- Valution of Common Stocks PDFDocument38 pagesValution of Common Stocks PDFMandeep SinghNo ratings yet

- 2018 19Document4 pages2018 19Jony SaifulNo ratings yet

- Eicher Motors Profit and Loss AccountDocument2 pagesEicher Motors Profit and Loss AccountVaishnav Sunil100% (1)

- Pilgan Lat UASDocument9 pagesPilgan Lat UASashilahila04No ratings yet

- CK TangsDocument21 pagesCK TangsEfendiNo ratings yet

- Difference Between Shares and DebenturesDocument4 pagesDifference Between Shares and DebenturesVinodKumarMNo ratings yet

- Tutorial 4Document4 pagesTutorial 4JIA ERN GOHNo ratings yet

- Altman's Z-Score ReportDocument19 pagesAltman's Z-Score ReportSaif Muhammad FahadNo ratings yet

- Founder Institute - Fundraising-1Document15 pagesFounder Institute - Fundraising-1Bryan JaneczkoNo ratings yet

- Indofood Agri-Resources - IndoAgri Ar2013Document162 pagesIndofood Agri-Resources - IndoAgri Ar2013Appie Koekange100% (1)

- Vijay El MbfsDocument2 pagesVijay El MbfsPraveen KumarNo ratings yet

- FinQuiz - Smart Summary - Study Session 14 - Reading 50Document4 pagesFinQuiz - Smart Summary - Study Session 14 - Reading 50Rafael100% (1)

- EVA in GodrejDocument5 pagesEVA in GodrejRavi ChandranNo ratings yet

- Hybrid Finance - EssayDocument6 pagesHybrid Finance - EssayMalina TatarovaNo ratings yet