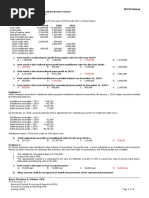

The document provides financial information for Appliance Company that reports gross profit using the installment method for the years 2018-2020. It includes data on installment sales, cost of goods sold, collections on installment contracts, and defaults/repossessions. It asks two multiple choice questions about calculating realized gross profit before loss on repossession for 2020 and the loss on repossession for 2020 based on the provided data.

The second part of the document provides similar financial data for Davao Company for 2018-2020 and asks what the total balance of Installment Accounts Receivable was on December 31, 2020 based on the data given.

It then provides additional context and financial details about a car sale by an entity to a customer in 2018 under

The document provides financial information for Appliance Company that reports gross profit using the installment method for the years 2018-2020. It includes data on installment sales, cost of goods sold, collections on installment contracts, and defaults/repossessions. It asks two multiple choice questions about calculating realized gross profit before loss on repossession for 2020 and the loss on repossession for 2020 based on the provided data.

The second part of the document provides similar financial data for Davao Company for 2018-2020 and asks what the total balance of Installment Accounts Receivable was on December 31, 2020 based on the data given.

It then provides additional context and financial details about a car sale by an entity to a customer in 2018 under

The document provides financial information for Appliance Company that reports gross profit using the installment method for the years 2018-2020. It includes data on installment sales, cost of goods sold, collections on installment contracts, and defaults/repossessions. It asks two multiple choice questions about calculating realized gross profit before loss on repossession for 2020 and the loss on repossession for 2020 based on the provided data.

The second part of the document provides similar financial data for Davao Company for 2018-2020 and asks what the total balance of Installment Accounts Receivable was on December 31, 2020 based on the data given.

It then provides additional context and financial details about a car sale by an entity to a customer in 2018 under

The document provides financial information for Appliance Company that reports gross profit using the installment method for the years 2018-2020. It includes data on installment sales, cost of goods sold, collections on installment contracts, and defaults/repossessions. It asks two multiple choice questions about calculating realized gross profit before loss on repossession for 2020 and the loss on repossession for 2020 based on the provided data.

The second part of the document provides similar financial data for Davao Company for 2018-2020 and asks what the total balance of Installment Accounts Receivable was on December 31, 2020 based on the data given.

It then provides additional context and financial details about a car sale by an entity to a customer in 2018 under

Defaults Unpaid balance of 2018 installment contracts 12,500 15,000 Value assigned to repossessed merchandise 6,500 6,000 Unpaid balance of 2019 installment contracts 16,000 Value assigned to repossessed merchandise 9,000

36. What is the realized gross profit before loss on repossession for 2020? A. 49,775 B. 57,625 C. 48,975 D. 56,625

1. What is the loss on repossession for 2020?

A. 5,250 B. 2,600 C. 7,850 D. 9,000

Page 14

Number 38 (Installment sales)

Davao Company uses the installment method of income recognition. The entity provided the following pertinent data:

2018 2019 2020

Installment sales 300,000 375,000 360,000 Cost of goods sold 225,000 285,000 252,000

What is the total balance of the Installment Accounts Receivable on December 31, 2020? A. 270,000 B. 277,500 C. 279,000 D. 300,000

Numbers 39 and 40 (Installment Sales)

On January 1, 2018, an entity sold a car to a customer at a price of P400,000 with a production cost of P300,000. It is the entity’s policy to employ installment method to recognize gross profit from installment sales.

At the time of sale, the entity received cash amounting to 25% of the selling price and old car with trade-in allowance of P50,000. The said old car has fair value of P150,000. The customer issued a 5-year note for the balance to be payable in equal annual installments every December 31 starting 2018. The note payable is interest bearing with 10% rate due on the remaining balance of the note.

The customer was able to pay the first annual installment and corresponding interest due. However, after the payment of the second interest due, the customer defaulted on the second annual installment which resulted to the repossession of the car sold with appraised value of P110,000. On December 31, 2019, the repossessed car was resold for P140,000 after reconditioning cost of P10,000.