Download as docx, pdf, or txt

You might also like

- 10 Merger Model Case Study Jos A Bank Mens WearhouseDocument6 pages10 Merger Model Case Study Jos A Bank Mens WearhouseTayyaba YounasNo ratings yet

- Cost Old DeptalsDocument9 pagesCost Old Deptalsyugyeom rojas0% (1)

- Cost Old DeptalsDocument9 pagesCost Old Deptalsyugyeom rojas0% (1)

- BSA181A Interim Assessment Bapaud3X: PointsDocument8 pagesBSA181A Interim Assessment Bapaud3X: PointsMary DenizeNo ratings yet

- Pas 17Document6 pagesPas 17AngelicaNo ratings yet

- Chapter 18Document20 pagesChapter 18Norman DelirioNo ratings yet

- Testbank Ch01 02 REV Acc STD PDFDocument7 pagesTestbank Ch01 02 REV Acc STD PDFheldiNo ratings yet

- Unit 5. Audit of Investments, Hedging Instruments, and Related Revenues - Handout - T21920 (Final)Document9 pagesUnit 5. Audit of Investments, Hedging Instruments, and Related Revenues - Handout - T21920 (Final)Alyna JNo ratings yet

- Ppe Depreciation and DepletionDocument21 pagesPpe Depreciation and DepletionEarl Lalaine EscolNo ratings yet

- Chapter 13 - Property, Plant, and Equipment Depreciation and DepletionDocument32 pagesChapter 13 - Property, Plant, and Equipment Depreciation and DepletionHamda AbdinasirNo ratings yet

- Psa 600Document9 pagesPsa 600Bhebi Dela CruzNo ratings yet

- FAR 2733 - Share-Based-Payment PDFDocument4 pagesFAR 2733 - Share-Based-Payment PDFPHI NGUYEN HOANGNo ratings yet

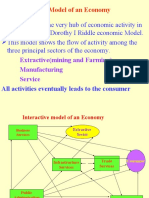

- Interactive Model of An EconomyDocument142 pagesInteractive Model of An Economyrajraj999No ratings yet

- PpeDocument5 pagesPpeRachel LeachonNo ratings yet

- 5rd Sessiom - Audit of LeaseDocument20 pages5rd Sessiom - Audit of LeaseRUFFA SANCHEZNo ratings yet

- ch11 Doc PDF - 2 PDFDocument39 pagesch11 Doc PDF - 2 PDFRenzo RamosNo ratings yet

- Quiz 1 Introduction To Managerial AccountingDocument7 pagesQuiz 1 Introduction To Managerial AccountingHera AsuncionNo ratings yet

- Ia1 5a Investments 15 FVDocument55 pagesIa1 5a Investments 15 FVJm SevallaNo ratings yet

- Audit of General Insurance CompaniesDocument16 pagesAudit of General Insurance CompaniesTACS & CO.No ratings yet

- Rey Ocampo Online! Financial Accounting and Reporting: Pfrs QuizDocument11 pagesRey Ocampo Online! Financial Accounting and Reporting: Pfrs QuizClyde RamosNo ratings yet

- Theory of AccountsDocument38 pagesTheory of AccountsJoovs JoovhoNo ratings yet

- Finals Reviewer AudtheoDocument36 pagesFinals Reviewer AudtheoMae VillarNo ratings yet

- MAS 09 - Quantitative TechniquesDocument6 pagesMAS 09 - Quantitative TechniquesClint Abenoja0% (1)

- Far - Mock BoardDocument11 pagesFar - Mock BoardKial PachecoNo ratings yet

- Module 4Document14 pagesModule 4Queenie ValleNo ratings yet

- Finals Conceptual Framework and Accounting Standards AnswerkeyDocument7 pagesFinals Conceptual Framework and Accounting Standards AnswerkeyMay Anne MenesesNo ratings yet

- Pas 32 Pfrs 9 Part 2Document8 pagesPas 32 Pfrs 9 Part 2Carmel Therese100% (1)

- Afar Income Recognition Installment Sales Franchise Long Term Construction PDFDocument10 pagesAfar Income Recognition Installment Sales Franchise Long Term Construction PDFKim Nicole ReyesNo ratings yet

- Self Practice Cost AccountingDocument17 pagesSelf Practice Cost AccountingLara Alyssa GarboNo ratings yet

- Intangible Assets PDFDocument9 pagesIntangible Assets PDFFery AnnNo ratings yet

- Chapter 3 Quiz KeyDocument2 pagesChapter 3 Quiz KeyAmna MalikNo ratings yet

- Property, Plant and Equipment (PAS 16)Document10 pagesProperty, Plant and Equipment (PAS 16)VIRGIL KIT AUGUSTIN ABANILLANo ratings yet

- Chapter 10 Investments in Debt SecuritiesDocument24 pagesChapter 10 Investments in Debt SecuritiesChristian Jade Lumasag NavaNo ratings yet

- Audit Problems FinalDocument48 pagesAudit Problems FinalShane TabunggaoNo ratings yet

- Module 4 - ImpairmentDocument5 pagesModule 4 - ImpairmentLuiNo ratings yet

- Auditing Theory - Risk AssessmentDocument10 pagesAuditing Theory - Risk AssessmentYenelyn Apistar CambarijanNo ratings yet

- Chapter 3 (Auditing Theory)Document7 pagesChapter 3 (Auditing Theory)Rae YaNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument23 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsFery AnnNo ratings yet

- 2.8 Substantive Tests - AR and SalesDocument2 pages2.8 Substantive Tests - AR and SalesBrian Jeric MorilloNo ratings yet

- FAR 4308 Investment in AssociatesDocument4 pagesFAR 4308 Investment in AssociatesATHALIAH LUNA MERCADEJASNo ratings yet

- Pas 40 Investment PropertyDocument4 pagesPas 40 Investment PropertykristineNo ratings yet

- BPS Quiz Intangibles PRINTDocument3 pagesBPS Quiz Intangibles PRINTSheena CalderonNo ratings yet

- Income Based ValuationDocument25 pagesIncome Based ValuationApril Joy ObedozaNo ratings yet

- Afar 2019Document9 pagesAfar 2019TakuriNo ratings yet

- Audit of LiabilitiesDocument12 pagesAudit of LiabilitiesAcier KozukiNo ratings yet

- PFRS 17Document2 pagesPFRS 17Annie JuliaNo ratings yet

- Cash and Accrual Discussion301302Document2 pagesCash and Accrual Discussion301302Gloria BeltranNo ratings yet

- Mikong Due MARCH 30 Hospital and HmosDocument6 pagesMikong Due MARCH 30 Hospital and HmosCoke Aidenry SaludoNo ratings yet

- Ais Master Reviewer 1 8 Accounting Info System Test BankDocument59 pagesAis Master Reviewer 1 8 Accounting Info System Test BankNico ErnestoNo ratings yet

- QUIZ-Audit Evidence and Audit ProgramsDocument12 pagesQUIZ-Audit Evidence and Audit ProgramsKathleenNo ratings yet

- Financial Asset MILLANDocument6 pagesFinancial Asset MILLANAlelie Joy dela CruzNo ratings yet

- B. A Liability of Uncertain Timing or AmountDocument15 pagesB. A Liability of Uncertain Timing or Amountcherry blossomNo ratings yet

- MA Cabrera 2010 - SolManDocument4 pagesMA Cabrera 2010 - SolManCarla Francisco Domingo40% (5)

- Pas 36Document1 pagePas 36Vinz Ray PitargueNo ratings yet

- Pas 21-The Effects of Changes in Foreign Exchange RatesDocument3 pagesPas 21-The Effects of Changes in Foreign Exchange RatesAryan LeeNo ratings yet

- May 2020 - AP Drill 1 (SHE & Liabs) - FinalDocument10 pagesMay 2020 - AP Drill 1 (SHE & Liabs) - FinalROMAR A. PIGANo ratings yet

- Questionnaire Expenditure CycleDocument1 pageQuestionnaire Expenditure Cycleleodenin tulangNo ratings yet

- Chapter 19Document6 pagesChapter 19Joan Angelica ManaloNo ratings yet

- Reviewer For Liabilities and Substantive Test of LiabilitiesDocument4 pagesReviewer For Liabilities and Substantive Test of LiabilitiesErica FlorentinoNo ratings yet

- Naqdown Final Round 2013Document8 pagesNaqdown Final Round 2013MJ YaconNo ratings yet

- Exercise 6-1 (Classification of Cost Drivers)Document18 pagesExercise 6-1 (Classification of Cost Drivers)Barrylou ManayanNo ratings yet

- Test BankDocument26 pagesTest BankMonica BuscatoNo ratings yet

- Full Multiple Choice For StudentsDocument80 pagesFull Multiple Choice For StudentsÝ ThủyNo ratings yet

- MODULE 3 Step 1Document7 pagesMODULE 3 Step 1yugyeom rojasNo ratings yet

- Module in Cash To Accrual and Vice VersaDocument12 pagesModule in Cash To Accrual and Vice Versayugyeom rojasNo ratings yet

- CFAS - Final Examination - 1st Sem 2019-2020Document10 pagesCFAS - Final Examination - 1st Sem 2019-2020yugyeom rojasNo ratings yet

- 300 200 10 10 100 7 3 42 C1 X1 X2 10 0 0 10 C2 X1 X2 6 0 0 14 Feasible RegionDocument2 pages300 200 10 10 100 7 3 42 C1 X1 X2 10 0 0 10 C2 X1 X2 6 0 0 14 Feasible Regionyugyeom rojasNo ratings yet

- Learning Modules: Chapter 4 - Linear Programming: Modelling ExamplesDocument3 pagesLearning Modules: Chapter 4 - Linear Programming: Modelling Examplesyugyeom rojasNo ratings yet

- CFAS - Final Examination - 1st Sem 2019-2020Document10 pagesCFAS - Final Examination - 1st Sem 2019-2020yugyeom rojasNo ratings yet

- 1outline On Sales by Dean Villanueva 2015 1outline On Sales by Dean Villanueva 2015Document52 pages1outline On Sales by Dean Villanueva 2015 1outline On Sales by Dean Villanueva 2015yugyeom rojasNo ratings yet

- Workforce Planning 12345Document3 pagesWorkforce Planning 12345yugyeom rojasNo ratings yet

- Financial Statements: Historical Results 2012 2013 2014Document2 pagesFinancial Statements: Historical Results 2012 2013 2014yugyeom rojasNo ratings yet

- Workforce Planning:: A Practical GuideDocument31 pagesWorkforce Planning:: A Practical Guideyugyeom rojasNo ratings yet

- BAFS - Mock Paper 2A - Set 10 - EngDocument9 pagesBAFS - Mock Paper 2A - Set 10 - Enghannahho0723No ratings yet

- Unit III Cash Flow Statement: BenefitsDocument7 pagesUnit III Cash Flow Statement: BenefitsnamrataNo ratings yet

- Instant Download Ebook PDF Financial Management Principles and Applications 7th Edition PDF ScribdDocument42 pagesInstant Download Ebook PDF Financial Management Principles and Applications 7th Edition PDF Scribdcheryl.morgan378100% (50)

- Amazon Fba Calculator 2023Document7 pagesAmazon Fba Calculator 2023DWIJ MEWADANo ratings yet

- Laporan Neraca 2011Document3 pagesLaporan Neraca 2011afick abidzarNo ratings yet

- CH 02Document36 pagesCH 02api-3804982100% (1)

- Bert and Ernie Accounts Prep QuestionDocument3 pagesBert and Ernie Accounts Prep Questioncons theNo ratings yet

- HDFC Bank - FM AssignmentDocument9 pagesHDFC Bank - FM AssignmentaditiNo ratings yet

- Analysis To Financial Statement: FLEX Course MaterialDocument29 pagesAnalysis To Financial Statement: FLEX Course MaterialElla Marie LopezNo ratings yet

- 6018 p1 Akuntansi Lembar Kerja SiklusDocument10 pages6018 p1 Akuntansi Lembar Kerja SiklusnarwanNo ratings yet

- Multiple Choice AssetDocument4 pagesMultiple Choice AssetRianntyD98No ratings yet

- CH005Document52 pagesCH005Lana LoaiNo ratings yet

- Financial Statement AnalysisDocument77 pagesFinancial Statement AnalysisChetan PatelNo ratings yet

- Share Based Payments-ExercisesDocument6 pagesShare Based Payments-ExercisesReign TambasacanNo ratings yet

- ACCA - FR Financial Reporting - CBEs 18-19 - FR - CBE Mock - 1Document52 pagesACCA - FR Financial Reporting - CBEs 18-19 - FR - CBE Mock - 1NgọcThủyNo ratings yet

- Sri Lanka Accounting Standard-LKAS 31: Interests in Joint VenturesDocument17 pagesSri Lanka Accounting Standard-LKAS 31: Interests in Joint VenturesMaithri Vidana KariyakaranageNo ratings yet

- Test Bank For Introduction To Governmental and Not For Profit Accounting 7th Edition by Ives DownloadDocument19 pagesTest Bank For Introduction To Governmental and Not For Profit Accounting 7th Edition by Ives DownloadTeresaMoorecsrby100% (49)

- ACC311 SUMMARYpdfDocument22 pagesACC311 SUMMARYpdfHalibut SidraNo ratings yet

- Module 5&6Document29 pagesModule 5&6Lee DokyeomNo ratings yet

- Applied Auditing Quiz #1 (Diagnostic Exam)Document15 pagesApplied Auditing Quiz #1 (Diagnostic Exam)xjammerNo ratings yet

- Alpha BetaDocument13 pagesAlpha BetaJoel Christian MascariñaNo ratings yet

- Format of Profit and Loss and Other Comprehensive StatementDocument5 pagesFormat of Profit and Loss and Other Comprehensive StatementIleo AliNo ratings yet

- Quiz 1 Midterm Bac100Document12 pagesQuiz 1 Midterm Bac100G Rosal, Denice Angela A.No ratings yet

- CH 09Document84 pagesCH 09trang lêNo ratings yet

- Special Liabilities San Carlos CollegeDocument23 pagesSpecial Liabilities San Carlos CollegeRowbby Gwyn100% (1)

- Nama Anggota: Ardhe Nareswari S Ghaida Aulia P Salsabila Eka S Kelas: 2B - Keuangan Syariah P6-6A March 1 (195144033) (195144042) (195144057)Document5 pagesNama Anggota: Ardhe Nareswari S Ghaida Aulia P Salsabila Eka S Kelas: 2B - Keuangan Syariah P6-6A March 1 (195144033) (195144042) (195144057)Ghaida AuliaNo ratings yet

- Team MembersDocument8 pagesTeam MembersUyen HoangNo ratings yet

- ACCT 211 Introductory Accounting I Mock Final Exam 2016Document4 pagesACCT 211 Introductory Accounting I Mock Final Exam 2016Nguyễn Ngọc MaiNo ratings yet

- Project Sunrise: Molson Coors International, India SAP Implementation - Project Sunrise Module: ControllingDocument43 pagesProject Sunrise: Molson Coors International, India SAP Implementation - Project Sunrise Module: ControllingKaveri BangarNo ratings yet