4 Cir V Burmeister

4 Cir V Burmeister

Download as docx, pdf, or txt

You might also like

- Petitioner vs. vs. Respondent: First DivisionDocument7 pagesPetitioner vs. vs. Respondent: First DivisionRamon EldonoNo ratings yet

- Memorandum of Law On The NameDocument30 pagesMemorandum of Law On The NameJim Kushi0% (1)

- Pollo Vs DavidDocument4 pagesPollo Vs DavidIrish Asilo PinedaNo ratings yet

- Commissioner of Internal Revenue VDocument1 pageCommissioner of Internal Revenue VBeverly LegaspiNo ratings yet

- 33 Citigroup Inc. Vs Citystate Savings BankDocument12 pages33 Citigroup Inc. Vs Citystate Savings BankMistery GaimierNo ratings yet

- ME Holding Corp Vs CADocument1 pageME Holding Corp Vs CAjanhelNo ratings yet

- Pilipinas Shell Vs CirDocument1 pagePilipinas Shell Vs CirMj GarciaNo ratings yet

- 115 - SilkAir Vs CIRDocument8 pages115 - SilkAir Vs CIRCollen Anne PagaduanNo ratings yet

- Encarnacion v. AmigoDocument2 pagesEncarnacion v. Amigolouis jansenNo ratings yet

- 1 - CHR Employees v. CA - Baquilod PDFDocument2 pages1 - CHR Employees v. CA - Baquilod PDFNica Cielo B. LibunaoNo ratings yet

- 8.cir V Roh Auto ProductsDocument2 pages8.cir V Roh Auto ProductsQuengilyn QuintosNo ratings yet

- Transportation Law Notes 1Document23 pagesTransportation Law Notes 1BerniceAnneAseñas-ElmacoNo ratings yet

- Sto Tomas Vs SalacDocument1 pageSto Tomas Vs SalacJenNo ratings yet

- Carabeo vs. CADocument10 pagesCarabeo vs. CALeane Leandra SNo ratings yet

- No, The Case of Anna, The Owner of A Drugstore Which Was Established by Her Ancestors Way BackDocument2 pagesNo, The Case of Anna, The Owner of A Drugstore Which Was Established by Her Ancestors Way BackkatNo ratings yet

- Land Bank Vs SantiagoDocument10 pagesLand Bank Vs SantiagoPaulo Miguel GernaleNo ratings yet

- YHT Realty v. CADocument2 pagesYHT Realty v. CAKaren Ryl Lozada BritoNo ratings yet

- Dionisia Pacquiao vs. Malibao (2017)Document2 pagesDionisia Pacquiao vs. Malibao (2017)Xavier BataanNo ratings yet

- Taxation Case Digest 3Document9 pagesTaxation Case Digest 3seentherellaaaNo ratings yet

- 3y1s Tax F 1 FullshemDocument38 pages3y1s Tax F 1 FullshemWolf DenNo ratings yet

- BELGICA V OCHOADocument6 pagesBELGICA V OCHOABea Crisostomo100% (1)

- 2.sabay Vs PeopleDocument2 pages2.sabay Vs PeopleAnonymous rVdy7u5No ratings yet

- Vat Ruling No. 444-88Document1 pageVat Ruling No. 444-88Joahnna Paula CorpuzNo ratings yet

- Tax Case Digest For 8.17.19Document34 pagesTax Case Digest For 8.17.19Jayson Lloyd P. MaquilanNo ratings yet

- Cir Vs Metro Super Rama DigestDocument2 pagesCir Vs Metro Super Rama DigestKobe BryantNo ratings yet

- Labor Relations CasesDocument15 pagesLabor Relations CasesJamie JovellanosNo ratings yet

- Ormoc Sugarcane Planters - Association, Inc. v. CA - CandolitaDocument3 pagesOrmoc Sugarcane Planters - Association, Inc. v. CA - CandolitaDante CastilloNo ratings yet

- Negotiable Instruments, Torts and Damages Case Digest: BPI V. CA, China Banking Corp and Phil. Clearing Housee Corp. (1992) Our BookshelfDocument1 pageNegotiable Instruments, Torts and Damages Case Digest: BPI V. CA, China Banking Corp and Phil. Clearing Housee Corp. (1992) Our BookshelfVernis VentilacionNo ratings yet

- OCA v. Fuentes IIIDocument9 pagesOCA v. Fuentes IIIJune Vincent FerrerNo ratings yet

- July 18 - SPIT NotesDocument8 pagesJuly 18 - SPIT NotesMiggy CardenasNo ratings yet

- PNB Vs RBLDocument2 pagesPNB Vs RBLJona Myka DugayoNo ratings yet

- Ra 7905Document4 pagesRa 7905lance757No ratings yet

- 4-d Franklin-Baker-Co-vs-SSS-case-digestDocument2 pages4-d Franklin-Baker-Co-vs-SSS-case-digestKattNo ratings yet

- Pepsi Cola Bottling vs. Municipality of Tanauan 69 SCRA 460Document4 pagesPepsi Cola Bottling vs. Municipality of Tanauan 69 SCRA 460MhaliNo ratings yet

- Deregulation of The Philippine Shipping Industry: Easing Restrictions On The Cabotage LawDocument7 pagesDeregulation of The Philippine Shipping Industry: Easing Restrictions On The Cabotage Laweric-paolo-smith-6354No ratings yet

- 15 Garcia V Comelec - Art10s3Document5 pages15 Garcia V Comelec - Art10s3Tanya IñigoNo ratings yet

- Alvarez Vs Guingona - G.R. No. 118303. January 31, 1996Document8 pagesAlvarez Vs Guingona - G.R. No. 118303. January 31, 1996Ebbe DyNo ratings yet

- HIKINEX Sales Account Executive JDDocument2 pagesHIKINEX Sales Account Executive JDClaire SumicadNo ratings yet

- Sea-Land Service v. CA 357 SCRA 441Document2 pagesSea-Land Service v. CA 357 SCRA 441Kyle DionisioNo ratings yet

- Republic Vs MambulaoDocument1 pageRepublic Vs MambulaoJayNo ratings yet

- 07 CIR Vs Algue INCDocument3 pages07 CIR Vs Algue INCjamNo ratings yet

- 1 Cir, vs. Pilipinas Shell Petroleum CorporationDocument32 pages1 Cir, vs. Pilipinas Shell Petroleum CorporationChristineNo ratings yet

- Ra 9497Document41 pagesRa 9497Laarni De VeraNo ratings yet

- Insular Bank of Asia & America Vs IACDocument2 pagesInsular Bank of Asia & America Vs IACPatricia TaduranNo ratings yet

- Kepco Vs CirDocument1 pageKepco Vs CirMatthew ChandlerNo ratings yet

- Villanueva Vs BalaguerDocument13 pagesVillanueva Vs BalaguerJani MisterioNo ratings yet

- Joaquin v. DrilonDocument6 pagesJoaquin v. DrilonNenzo CruzNo ratings yet

- United Cadiz Sugar Farmers Association Multi-Purpose Cooperative v. CommissionerDocument6 pagesUnited Cadiz Sugar Farmers Association Multi-Purpose Cooperative v. CommissionerEryl YuNo ratings yet

- Commissioner of Internal Revenue Vs Central Luzon Drug Corporation GR No 159647Document36 pagesCommissioner of Internal Revenue Vs Central Luzon Drug Corporation GR No 159647Tamara Bianca Chingcuangco Ernacio-TabiosNo ratings yet

- White Gold Marine Services Vs Pioneer InsuranceDocument2 pagesWhite Gold Marine Services Vs Pioneer InsuranceCarmii HoNo ratings yet

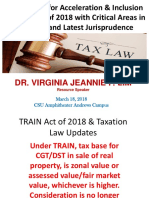

- TRAIN Act of 2018 & Taxation Law UpdatesDocument21 pagesTRAIN Act of 2018 & Taxation Law UpdatesPafra BariuanNo ratings yet

- Commissioner v. British Overseas Airways Corp., 149 SCRA 395, G.R. No. L-65773-74, April 30, 1987Document4 pagesCommissioner v. British Overseas Airways Corp., 149 SCRA 395, G.R. No. L-65773-74, April 30, 1987Agnes Bianca MendozaNo ratings yet

- CIR v. AcesiteDocument2 pagesCIR v. AcesiteATRNo ratings yet

- TAN V CADocument2 pagesTAN V CARaven Claire MalacaNo ratings yet

- Fisher v. Yangco Steamship CoDocument3 pagesFisher v. Yangco Steamship CosakaskajbNo ratings yet

- 7.-Republic vs. Kawashima TextimeMfg, G.R. No. 160352, July 23, 2008Document1 page7.-Republic vs. Kawashima TextimeMfg, G.R. No. 160352, July 23, 2008Christopher AdvinculaNo ratings yet

- Alejandro B. Ty v. Aurelio C. Trampe, GR No. 117577Document3 pagesAlejandro B. Ty v. Aurelio C. Trampe, GR No. 117577Shierly Ba-adNo ratings yet

- Ang Vs Associated BankDocument1 pageAng Vs Associated BankFranz Henri de GuzmanNo ratings yet

- Marubeni Corp V CirDocument3 pagesMarubeni Corp V CirTintin CoNo ratings yet

- Cases in Taxation 2Document145 pagesCases in Taxation 2MACNo ratings yet

- CIR v. BurmeisterDocument6 pagesCIR v. BurmeisterPaul Joshua SubaNo ratings yet

- (A) Full Case CIR Vs BurmeisterDocument9 pages(A) Full Case CIR Vs BurmeisterWhoopi Jane MagdozaNo ratings yet

- 128 Allied Banking Corporation v. SiaDocument5 pages128 Allied Banking Corporation v. SiaRamon EldonoNo ratings yet

- University of The Philippines College of Law - Commercial Law Review - Prof. Nilo DivinaDocument4 pagesUniversity of The Philippines College of Law - Commercial Law Review - Prof. Nilo DivinaRamon EldonoNo ratings yet

- 2 ING Bank N.V. v. CIRDocument2 pages2 ING Bank N.V. v. CIRRamon EldonoNo ratings yet

- 04 - AUF V City of AngelesDocument1 page04 - AUF V City of AngelesRamon EldonoNo ratings yet

- 05 Meralco v. City TreasurerDocument6 pages05 Meralco v. City TreasurerRamon EldonoNo ratings yet

- Intel Technology Philippines Inc. v. CIR (2007)Document37 pagesIntel Technology Philippines Inc. v. CIR (2007)Ramon EldonoNo ratings yet

- RMO No. 35-2018 DigestDocument1 pageRMO No. 35-2018 DigestRamon EldonoNo ratings yet

- REVENUE MEMORANDUM CIRCULAR NO. 62-2018 Issued On July 10, 2018 ClarifiesDocument1 pageREVENUE MEMORANDUM CIRCULAR NO. 62-2018 Issued On July 10, 2018 ClarifiesRamon EldonoNo ratings yet

- City Government of San Pablo V ReyesDocument2 pagesCity Government of San Pablo V ReyesRamon EldonoNo ratings yet

- REVENUE MEMORANDUM CIRCULAR NO. 85-2018 Issued On October 1, 2018 ClarifiesDocument1 pageREVENUE MEMORANDUM CIRCULAR NO. 85-2018 Issued On October 1, 2018 ClarifiesRamon EldonoNo ratings yet

- Risos-Vidal V COMELECDocument3 pagesRisos-Vidal V COMELECRamon EldonoNo ratings yet

- Abella V AbellaDocument3 pagesAbella V AbellaRamon EldonoNo ratings yet

- Bureau of Internal Revenue: Republic of The Philippines Department of Finance Quezon City July 17, 2018Document1 pageBureau of Internal Revenue: Republic of The Philippines Department of Finance Quezon City July 17, 2018Ramon EldonoNo ratings yet

- Compensatory Interest Presentation OutlineDocument3 pagesCompensatory Interest Presentation OutlineRamon EldonoNo ratings yet

- Delfin v. BillonesDocument3 pagesDelfin v. BillonesRamon EldonoNo ratings yet

- Aguirre v. Rana (2003)Document2 pagesAguirre v. Rana (2003)Ramon EldonoNo ratings yet

- 8 Villa Rey Transit Inc vs. FerrerDocument2 pages8 Villa Rey Transit Inc vs. FerrerRamon EldonoNo ratings yet

- 13 - Secretary of Health v. Domagas (1995)Document2 pages13 - Secretary of Health v. Domagas (1995)Ramon EldonoNo ratings yet

- Real v. Sangu Philippines, Inc. (2011)Document4 pagesReal v. Sangu Philippines, Inc. (2011)Ramon EldonoNo ratings yet

- Static Guard ContractDocument10 pagesStatic Guard ContractMohd Fazli LajakNo ratings yet

- People vs. Magpantay (C.A., 46 O.G. 1655)Document1 pagePeople vs. Magpantay (C.A., 46 O.G. 1655)victoria chavezNo ratings yet

- International Relations PresentationDocument5 pagesInternational Relations PresentationAdnan KhanNo ratings yet

- Similar Fact Evidence 2020Document8 pagesSimilar Fact Evidence 2020Yi YingNo ratings yet

- French Revolution Diary Entries ActivityDocument3 pagesFrench Revolution Diary Entries Activityapi-345346145No ratings yet

- Gonzales V PNB, G.R. No. L-33320Document2 pagesGonzales V PNB, G.R. No. L-33320Karen Selina AquinoNo ratings yet

- A.C. No. 6942, July 17, 2013 Sonic Steel Industries, Inc., Complainant, V. Atty. Nonnatus P. CHUA, RespondentDocument4 pagesA.C. No. 6942, July 17, 2013 Sonic Steel Industries, Inc., Complainant, V. Atty. Nonnatus P. CHUA, RespondentCrystene R. SarandinNo ratings yet

- Introduction (Sri Ganesh Indestries)Document4 pagesIntroduction (Sri Ganesh Indestries)joginder1009No ratings yet

- Tam Pham Complaint W Arrest WarrantDocument6 pagesTam Pham Complaint W Arrest WarrantKristen Faith SchneiderNo ratings yet

- St. Croix County Property Transfers For Aug. 31-Sept. 6, 2020Document44 pagesSt. Croix County Property Transfers For Aug. 31-Sept. 6, 2020Michael BrunNo ratings yet

- TA DA EnglishDocument2 pagesTA DA Englishfci ag3No ratings yet

- Legal Ethics PPDocument89 pagesLegal Ethics PPcmv mendoza100% (2)

- The Sexual Harassment of Women at WorkplaceDocument29 pagesThe Sexual Harassment of Women at WorkplaceAyesha SyedNo ratings yet

- CTA FOIA May 6 2024Document13 pagesCTA FOIA May 6 2024Crains Chicago BusinessNo ratings yet

- UntitledDocument48 pagesUntitledTARCISIO CASTRO DO NascimentoNo ratings yet

- Jsusshv SjsusushevdjsosudnewhsebsDocument7 pagesJsusshv SjsusushevdjsosudnewhsebsEmmanuel BatinganNo ratings yet

- Property Law - January 2023Document3 pagesProperty Law - January 2023Mahak PamnaniNo ratings yet

- African Law Clinicians' Manual - Part 2 2013Document135 pagesAfrican Law Clinicians' Manual - Part 2 2013John ReguleNo ratings yet

- Research - Contract - Restitution MalaysiaDocument4 pagesResearch - Contract - Restitution MalaysiaLina Linamon100% (1)

- 15-11-02 Apple v. Samsung CCIA Amicus ISO Petition For en BancDocument12 pages15-11-02 Apple v. Samsung CCIA Amicus ISO Petition For en BancFlorian MuellerNo ratings yet

- Icj IccDocument4 pagesIcj IccMary Christine Formiloza MacalinaoNo ratings yet

- KUNHIMOIDEENKUTTY vs. MARAKKARA GRAMA PANCHAYATDocument14 pagesKUNHIMOIDEENKUTTY vs. MARAKKARA GRAMA PANCHAYATAnu KuttanNo ratings yet

- Void Marriages Case DoctrinesDocument5 pagesVoid Marriages Case DoctrinesBoletPascuaNo ratings yet

- Deed of Transfer2 New DupicateDocument3 pagesDeed of Transfer2 New Dupicatetsoda125No ratings yet

- LONG Yu ComplaintDocument12 pagesLONG Yu ComplaintIthacaVoiceNo ratings yet

- LLJP NotesDocument45 pagesLLJP Notes9vx9d4qnxcNo ratings yet

- Go 13Document41 pagesGo 13Arumugham .kNo ratings yet

- Gregory Lee Smith LawsuitDocument17 pagesGregory Lee Smith LawsuitThe Salt Lake TribuneNo ratings yet

- 1 TCWD Week 5 Share Global GovernanceDocument43 pages1 TCWD Week 5 Share Global Governancecaitie miracleNo ratings yet