This document contains 22 statements related to determining residential status and taxability of income in India. 12 of the statements are false, including statements related to once being a resident always being one, residential status being determined solely by citizenship, and foreign income treatment for ordinary residents and non-residents. 10 statements are true, including those related to income deemed to accrue or arise in India always being taxable, residential status changing yearly, and an Indian citizen can be non-resident.

This document contains 22 statements related to determining residential status and taxability of income in India. 12 of the statements are false, including statements related to once being a resident always being one, residential status being determined solely by citizenship, and foreign income treatment for ordinary residents and non-residents. 10 statements are true, including those related to income deemed to accrue or arise in India always being taxable, residential status changing yearly, and an Indian citizen can be non-resident.

This document contains 22 statements related to determining residential status and taxability of income in India. 12 of the statements are false, including statements related to once being a resident always being one, residential status being determined solely by citizenship, and foreign income treatment for ordinary residents and non-residents. 10 statements are true, including those related to income deemed to accrue or arise in India always being taxable, residential status changing yearly, and an Indian citizen can be non-resident.

This document contains 22 statements related to determining residential status and taxability of income in India. 12 of the statements are false, including statements related to once being a resident always being one, residential status being determined solely by citizenship, and foreign income treatment for ordinary residents and non-residents. 10 statements are true, including those related to income deemed to accrue or arise in India always being taxable, residential status changing yearly, and an Indian citizen can be non-resident.

1. Once a person is a resident in a previous year he shall be deemed to be resident for

subsequent previous years.

2. Once a person is a resident for a source of income in a particular year he shall be deemed to be resident for all other sources of income in the same previous year.

3. A resident in India cannot become resident in any other country for the same assessment year.

4. Residential status is to be determined on the basis of stay in India during assessment year.

5. Incomes which accrue or arise outside India but are received directly into India are taxable only in case of resident.

6. Income deemed to accrue or arise in India is taxable in case of all the assessees.

7. Income which accrues or arise outside India from a business controlled from India is taxable case of only not ordinarily resident.

8. Income which accrues or arises outside India and also received outside India is taxable in case of both ordinarily resident and not ordinarily resident.

9. Total income of a person is determined on the basis of his citizenship in India.

10. Residential status of a person may change from year to year.

11. An Indian citizen may be a non-resident in India.

12. Residential status is important in deciding whether indian income of a person is taxable or not.

13. A person is deemed to be of "Indian origin", if his father was born in Pakistan in 1927.

14. A person is deemed to be of "Indian origin", if his mother was born in Nepal.

15. A person is deemed to be of "Indian origin", if his grandmother was born in Bangladesh

Tripathi Online Educare

1 in 1945.

16. A person is deemed to be of "Indian origin", if his grandfather was born in Sri Lanka in 1957.

17. While counting the number of days for determining residential status, a stay in a cruise boat anchored in the Mumbai Port is treated as stay in India.

18. Indian income is taxable in all cases, whether of an ordinary resident, or a not-ordinary resident, or a non-resident.

19. Foreign income of an ordinary resident is wholly taxable.

20. Foreign income of non-resident is not taxable at all.

21. Income accruing outside India will be deemed to be received in India if it is included in a balance sheet prepared in India.

22. If an income is included in the total income of a person on the basis of accrual, it may be included again on the basis of its receipt in subsequent period.

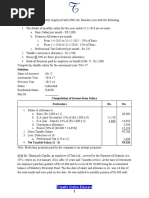

5. False; all the assesses 7. False; both ordinarily resident and not ordinarily resident 8. False; resident only 9. False; residential status in India 12.False; residential status is important in deciding whether foreign income of a person is taxable or not. 21. False; Income accruing outside India will not be deemed to be received in India merely because cannot be included again on the basis of its receipt in subsequent period (Explanation 2 to S.5)