1) The document provides an exam for Cost Accounting with 8 questions. It asks students to explain terms, analyze a statement, calculate economic order quantity and order numbers, estimate overhead expenses, prepare a product mix plan, and allocate service department overheads.

2) Question 3 requires calculating economic order quantity and order numbers for a company ordering a material. It provides cost data to perform the calculations.

3) Question 5 asks students to prepare a product sales mix that maximizes net profit based on demand, cost, and price data provided for 3 products. It requires calculating the optimal mix and projecting a profit and loss statement.

1) The document provides an exam for Cost Accounting with 8 questions. It asks students to explain terms, analyze a statement, calculate economic order quantity and order numbers, estimate overhead expenses, prepare a product mix plan, and allocate service department overheads.

2) Question 3 requires calculating economic order quantity and order numbers for a company ordering a material. It provides cost data to perform the calculations.

3) Question 5 asks students to prepare a product sales mix that maximizes net profit based on demand, cost, and price data provided for 3 products. It requires calculating the optimal mix and projecting a profit and loss statement.

1) The document provides an exam for Cost Accounting with 8 questions. It asks students to explain terms, analyze a statement, calculate economic order quantity and order numbers, estimate overhead expenses, prepare a product mix plan, and allocate service department overheads.

2) Question 3 requires calculating economic order quantity and order numbers for a company ordering a material. It provides cost data to perform the calculations.

3) Question 5 asks students to prepare a product sales mix that maximizes net profit based on demand, cost, and price data provided for 3 products. It requires calculating the optimal mix and projecting a profit and loss statement.

1) The document provides an exam for Cost Accounting with 8 questions. It asks students to explain terms, analyze a statement, calculate economic order quantity and order numbers, estimate overhead expenses, prepare a product mix plan, and allocate service department overheads.

2) Question 3 requires calculating economic order quantity and order numbers for a company ordering a material. It provides cost data to perform the calculations.

3) Question 5 asks students to prepare a product sales mix that maximizes net profit based on demand, cost, and price data provided for 3 products. It requires calculating the optimal mix and projecting a profit and loss statement.

“Labour turnover should be low whereas stock turnover should be high.” (08)

Q. 3 XYZ Company produces 200 articles of X per annum. Each article of X requires 3.8 units of material Y. Some other data is given below:

Cost per unit of Y Rs. 12,500

Warehouse monthly rent Rs. 15,000 Warehouse fumigation during the year Rs. 23,000 Watchman salary per month Rs. 4,500 Per order inspection charges Rs. 10,252 Service departments factory overhead charged to Store department Rs. 10,000 Ordering department Rs. 7,050 Stock holding per annum Rs. 125 per unit Working capital cost 16% Salaries of ordering department Rs. 10,050 Broker commission on supply of Y 0.50% Per order lump sum out of pocket expenses of broker of material Y Rs. 22,048

You are required to calculate:

(a) Economic Order Quantity. (08)

(b) Number of orders per annum on the basis of Economic Order Quantity. (02) (c) Verify your answer in (b) by calculating total ordering plus carrying costs per annum: (i) Assuming higher number of orders than in (b) (03) (ii) Assuming lower number of orders than in (b) (03) (2)

Q.4 AAB Company is planning its capacity for the year 2004 at 90% of the rated capacity. For the purpose of estimating ‘other factory overhead expenses’ company uses five years history and ‘simple regression analysis’ method. Data in hand is as under:

Rated capacity 20,000

Direct labour hours at 100% capacity 25,000

Five year history of ‘Other factory overhead expenses’ is as under:

In the year 2002 other factory overhead expenses include a penalty of Rs. 12,734 on non compliance of certain labour laws.

You are required to calculate fixed and variable portions of estimated other factory overhead expenses at planned capacity. (10)

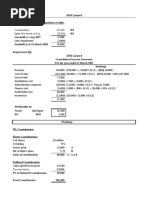

Q. 5 AAD Company’s Budgeting Department has compiled following data for decision-making:

Product Demand Average Material Labour Opening

in units sale price per unit per unit stock Rs. Rs. Rs. Units

A 1,500 318 172 76 50

B 2,200 421 172 173 50 C 3,700 280 172 32 -

Minimum order quantity of each product is 100 units. The company has Rs. 800,000 working capital in hand and a running finance line of Rs. 500,000 at 24% per annum cost.

Production lead time and sales recovery period is estimated at one year.

Administrative and marketing expenditure per annum are Rs. 152,700 and Rs. 72,842 respectively.

Opening stock carry same unit cost as given for current year.

You are required to:

(a) Prepare product sales mix that can generate maximum net profit. (08) (b) Projected Profit and Loss Statement according to your suggested product mix. (04) (3)

Q.6 Following is the data of Department B of EFG Company for December, 2003:

Work in process (opening) 8,500 units

(Completed as to material 20% and conversion cost 25%) Rs. 43,860 Work in process (ending) 11,540 units (Completed as to material 50% and conversion cost 25%) Current period transactions are: Cost transferred from Department A Rs. 45,600 Units transferred from Department A 12,000 units Units mishandled and lost before start of any process 460 units Material consumed Rs. 27,654 Conversion cost incurred Rs. 47,689 Units transferred out 7,500

Normal spoilage is 6% of units transferred out and inspection is done at the end of process. Company uses FIFO method for inventory valuation.

You are required to prepare production report of Department B showing Quantity

Schedule, Cost Charged to Department and Heads of Account where costs have been accounted for. (20)

Q.7 ABC Limited intend to commence production from July 1. They have provided following information for the first four months of operation: