0% found this document useful (0 votes)

396 viewsAnswers Are Highlighted in Yellow Color: MCQ's Subject:Introductory Econometrics

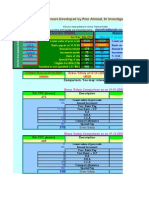

This document contains 34 multiple choice questions about introductory econometrics concepts such as the assumptions of the classical linear regression model (CLRM), consequences of violating assumptions like heteroscedasticity and autocorrelation, and issues like multicollinearity. The questions cover topics such as the assumptions required for OLS to be consistent, unbiased and efficient; consequences of violating CLRM assumptions; the meaning of heteroscedasticity and its effects; approaches to dealing with heteroscedasticity and autocorrelation; causes of autocorrelated residuals; consequences of using OLS when autocorrelation is present; remedies for near multicollinearity; and properties of the OLS estimator under multicollinearity.

Uploaded by

Majid AbCopyright

© © All Rights Reserved

Available Formats

Download as PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

396 viewsAnswers Are Highlighted in Yellow Color: MCQ's Subject:Introductory Econometrics

This document contains 34 multiple choice questions about introductory econometrics concepts such as the assumptions of the classical linear regression model (CLRM), consequences of violating assumptions like heteroscedasticity and autocorrelation, and issues like multicollinearity. The questions cover topics such as the assumptions required for OLS to be consistent, unbiased and efficient; consequences of violating CLRM assumptions; the meaning of heteroscedasticity and its effects; approaches to dealing with heteroscedasticity and autocorrelation; causes of autocorrelated residuals; consequences of using OLS when autocorrelation is present; remedies for near multicollinearity; and properties of the OLS estimator under multicollinearity.

Uploaded by

Majid AbCopyright

© © All Rights Reserved

Available Formats

Download as PDF, TXT or read online on Scribd

/ 16