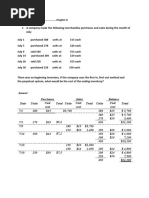

Inventories: Discussion Questions

Inventories: Discussion Questions

Download as doc, pdf, or txt

You might also like

- Van It A StatementDocument4 pagesVan It A Statementvanitakarran100% (2)

- Tis The Damn SeasonDocument4 pagesTis The Damn SeasonAmiyah100% (1)

- Megley CompanyDocument6 pagesMegley CompanyVanessa Camille Santos100% (1)

- Progress-Test-7-12-1 English FileDocument8 pagesProgress-Test-7-12-1 English Filehihihiha67% (3)

- JOURNAL Class 11 QuestionsDocument2 pagesJOURNAL Class 11 QuestionsHoyolab83% (12)

- Basic First Aid For KidsDocument43 pagesBasic First Aid For KidsG Chewie CervantesNo ratings yet

- 50 Sow Unit Piggery Business Plan Financials - USDDocument15 pages50 Sow Unit Piggery Business Plan Financials - USDonward marumuraNo ratings yet

- FCE Test 1Document20 pagesFCE Test 1ballesz0% (2)

- Stock Portfolio Tracker: Apr-24-2021 12:00 AMDocument18 pagesStock Portfolio Tracker: Apr-24-2021 12:00 AMSubirBhowmikNo ratings yet

- Practice ProblemDocument6 pagesPractice ProblemThe GentlemanNo ratings yet

- Break Even Analysis in ExcelDocument6 pagesBreak Even Analysis in ExcelKeuangan BLGNo ratings yet

- Topic 4.2 Chapter 12 Purchasing and Supply Chain Analysis Tools and TechniquesDocument12 pagesTopic 4.2 Chapter 12 Purchasing and Supply Chain Analysis Tools and Techniquesdiepbangdao7a1No ratings yet

- Break Even Analysis in ExcelDocument6 pagesBreak Even Analysis in Excelblack wolfNo ratings yet

- Chapter 10 Answer KeyDocument58 pagesChapter 10 Answer Keyjocelyn palacioNo ratings yet

- Group 5 - Terminal Report Sample 1Document6 pagesGroup 5 - Terminal Report Sample 1chronixlesNo ratings yet

- Financial Study RevisedDocument20 pagesFinancial Study RevisedDAISY MAE GURRO NAMOCNo ratings yet

- UTS KitDocument14 pagesUTS KitVinka AmaliaNo ratings yet

- Exhibit 1: Income StatementDocument16 pagesExhibit 1: Income StatementAbhishek GuptaNo ratings yet

- Excel WorkbookDocument1 pageExcel Workbookffjb884844No ratings yet

- 4 6008342639294811136Document11 pages4 6008342639294811136Tiwalola TejumolaNo ratings yet

- ASSSSWERDocument5 pagesASSSSWERChwchw ChwNo ratings yet

- 3rd Task operDocument53 pages3rd Task operarseny626No ratings yet

- Advanced Financial ManagementDocument8 pagesAdvanced Financial ManagementKRATOS GAMINGNo ratings yet

- Break Even AnalysisDocument5 pagesBreak Even Analysisumama mohsinNo ratings yet

- MGMT 562 Exam SpreadsheetDocument11 pagesMGMT 562 Exam Spreadsheettesapo4391No ratings yet

- HubSpot - Financial Planning TemplatesDocument7 pagesHubSpot - Financial Planning TemplatesericandmichelletrueNo ratings yet

- Taller N 2Document7 pagesTaller N 2Fotos MontseNo ratings yet

- Act. 1 Evidencia 2Document6 pagesAct. 1 Evidencia 2Luis Gerardo OrtizNo ratings yet

- Economic Batch Quantity (EBQ) : Prepared By: Talha Majeed Khan (M.Phil) Lecturer UCP, Faculty of Management StudiesDocument15 pagesEconomic Batch Quantity (EBQ) : Prepared By: Talha Majeed Khan (M.Phil) Lecturer UCP, Faculty of Management StudieszubairNo ratings yet

- Practice Problems For Exam #2Document5 pagesPractice Problems For Exam #2aifarNo ratings yet

- ASSINGMENTDocument2 pagesASSINGMENTBlaise WillieNo ratings yet

- Financial Plan Performance Daily LogDocument8 pagesFinancial Plan Performance Daily LogLeslie TabuzoNo ratings yet

- BreakEvenPointAnalysis and Selling PriceDocument8 pagesBreakEvenPointAnalysis and Selling PriceAnonymous zOo2mbaVANo ratings yet

- Exercise Ch6Document7 pagesExercise Ch6Yu SunaNo ratings yet

- Designer Lamp Project Blank SpreadsheetDocument4 pagesDesigner Lamp Project Blank SpreadsheetAnna BudaevaNo ratings yet

- G2 FS FinalDocument8 pagesG2 FS Finalxs2zdvr6wpNo ratings yet

- Taimoor Shahzad 265100 ME10D EE Assignment 01Document3 pagesTaimoor Shahzad 265100 ME10D EE Assignment 01Get-Set-GoNo ratings yet

- Food Truck Financial ProjectionsDocument68 pagesFood Truck Financial ProjectionsAmy Bersalona-DimapilisNo ratings yet

- Project NPV Sensitivity AnalysisDocument54 pagesProject NPV Sensitivity AnalysisAsad Mehmood100% (3)

- 3.1.2 - Basics Part 2 - BeginDocument14 pages3.1.2 - Basics Part 2 - Beginyasshh090No ratings yet

- Ramit - HomeWork PSA5Document8 pagesRamit - HomeWork PSA5NidhiNo ratings yet

- Amortizacion PDFDocument1 pageAmortizacion PDFFrancisco Antonio Olivas PérezNo ratings yet

- SJI2 Round 1 ProposalDocument4 pagesSJI2 Round 1 Proposalmarcus.ng.chen.kyeNo ratings yet

- Inventories and Cost of Sales: QuestionsDocument71 pagesInventories and Cost of Sales: QuestionsChaituNo ratings yet

- Arizona Microbrewery, Inc.: An Instructional Case On Management Decision MakingDocument5 pagesArizona Microbrewery, Inc.: An Instructional Case On Management Decision MakingAlia ShabbirNo ratings yet

- Arizona MicrobreweryDocument7 pagesArizona MicrobreweryInès ChougraniNo ratings yet

- Budgeting Template 2020-21 - KRT & CO, Chartered AccountantsDocument40 pagesBudgeting Template 2020-21 - KRT & CO, Chartered AccountantsMuhammad ShameerNo ratings yet

- INVENTORIES ExerciesDocument7 pagesINVENTORIES Exerciesmemedodoms7No ratings yet

- Inventory As Money NewDocument11 pagesInventory As Money New।। SultanNo ratings yet

- HW COmpuTINGDocument11 pagesHW COmpuTINGkossedmytroNo ratings yet

- Stoddart Farm CompletedDocument21 pagesStoddart Farm CompletedTara TaraNo ratings yet

- SUMa PRODUCToDocument8 pagesSUMa PRODUCToherlopbaldoNo ratings yet

- Copy of My Templates_2(1)Document42 pagesCopy of My Templates_2(1)draco.precipice25No ratings yet

- Copy of Book2(1)(AutoRecovered)Document8 pagesCopy of Book2(1)(AutoRecovered)Mac MNo ratings yet

- Inventory Valuation MethodsDocument10 pagesInventory Valuation Methodssalwa khan100% (5)

- MDT-Bang Quan Ly VonDocument23 pagesMDT-Bang Quan Ly VonMichael ZuiNo ratings yet

- Micro Eportfolio Monopoly Spreadsheet Data - SPG 18 1Document3 pagesMicro Eportfolio Monopoly Spreadsheet Data - SPG 18 1api-334921583No ratings yet

- Financial Aspect of Jute Mallow BiscuitDocument6 pagesFinancial Aspect of Jute Mallow Biscuitjanesupang19No ratings yet

- Inventory Valuation TutorialDocument4 pagesInventory Valuation TutorialSalma HazemNo ratings yet

- Category Assumptions Name Category Price - Min. Price - Max. Volume Year 1Document6 pagesCategory Assumptions Name Category Price - Min. Price - Max. Volume Year 1Evert TrochNo ratings yet

- Healthy Bread DelightDocument11 pagesHealthy Bread DelightSetty HakeemaNo ratings yet

- Biz Cafe Operations Excel - Assignment - UIDDocument3 pagesBiz Cafe Operations Excel - Assignment - UIDJenna AgeebNo ratings yet

- Sup Manuf Company Final DraftDocument18 pagesSup Manuf Company Final DraftRama NaveedNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- MajorMinor Modal InterchangeDocument2 pagesMajorMinor Modal InterchangeC Morzaht100% (1)

- Underground Steroid Handbook II Daniel Duchaine PDF 3Document2 pagesUnderground Steroid Handbook II Daniel Duchaine PDF 3sunz100% (1)

- Bug Bounty CheatsheetDocument53 pagesBug Bounty CheatsheetMichel Edi100% (1)

- ST BlaiseDocument5 pagesST BlaiseMhai LimpinNo ratings yet

- Code of Ethics For Professional TeachersDocument30 pagesCode of Ethics For Professional Teachersabegail corona100% (1)

- Fisiologi KarnitinDocument61 pagesFisiologi Karnitinmusta QiblatNo ratings yet

- Industry AnalysisDocument25 pagesIndustry AnalysisPrashant Tejwani100% (1)

- 1-SMB Sales VS OpleDocument3 pages1-SMB Sales VS OpleRen A EleponioNo ratings yet

- Sailesh V Event Marketing ReportDocument27 pagesSailesh V Event Marketing Reportsailesh vasaNo ratings yet

- Educ 102Document3 pagesEduc 102Miralyn TevesNo ratings yet

- Al Isra Wal Miraj KhutbaDocument4 pagesAl Isra Wal Miraj Khutbaabubakr parvezNo ratings yet

- Low Res Taigun Big Brochure-1Document15 pagesLow Res Taigun Big Brochure-1Aritra Fidato DasguptaNo ratings yet

- Strategic AllianceDocument12 pagesStrategic AllianceMadhura GiraseNo ratings yet

- Health Edge Insurance: Policy ScheduleDocument7 pagesHealth Edge Insurance: Policy Schedulearun saiNo ratings yet

- 250+ TOP MCQs On Software Maintenance and Answers 2023Document6 pages250+ TOP MCQs On Software Maintenance and Answers 2023WANGOH DAVID TENPORPUHNo ratings yet

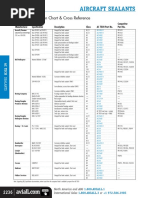

- Aircraft Sealants: Sealant Application Chart & Cross ReferenceDocument1 pageAircraft Sealants: Sealant Application Chart & Cross ReferenceYuda IswantoNo ratings yet

- Online Grading System of Pateros Technological CollegeDocument8 pagesOnline Grading System of Pateros Technological CollegeZoren DalluayNo ratings yet

- A Model of Happiness in The WorkplaceDocument12 pagesA Model of Happiness in The WorkplacenghianguyenNo ratings yet

- Real Tax Service (RTS)Document19 pagesReal Tax Service (RTS)JayaNo ratings yet

- ASKING AND RECEIVING Matthew 7:7-28 I. Asking and ReceivingDocument2 pagesASKING AND RECEIVING Matthew 7:7-28 I. Asking and ReceivingZelha RadivNo ratings yet

- Short Notes of Im - ShreyashDocument6 pagesShort Notes of Im - Shreyashdreament8No ratings yet

- Introduction To Supply Chain Management: Syed Tabish Hussain Iqra UniversityDocument54 pagesIntroduction To Supply Chain Management: Syed Tabish Hussain Iqra UniversityfarahsayaniNo ratings yet

- Natural Science 5th GradeDocument23 pagesNatural Science 5th GradeBeatriz Mata Gil33% (3)

- الترجمة الإعلامية 4Document198 pagesالترجمة الإعلامية 4kaderben392No ratings yet