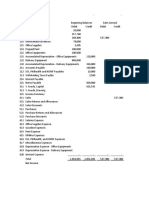

Intercompany Sale of Depreciable Assets

Intercompany Sale of Depreciable Assets

Download as pdf or txt

You might also like

- Ross Jeffries How To Get The Women You Desire Into BedDocument61 pagesRoss Jeffries How To Get The Women You Desire Into BedAndrei StoicaNo ratings yet

- Consignment SalesDocument10 pagesConsignment SalesMhelka TiodiancoNo ratings yet

- BagnpesDocument3 pagesBagnpesShiela Marie Sta AnaNo ratings yet

- VI. 80% Owned-Subsidiary: Cost Model - Full Goodwill Approach Downstream and Upstream of Property, Unrealized Gain and Realized Gain On SaleDocument3 pagesVI. 80% Owned-Subsidiary: Cost Model - Full Goodwill Approach Downstream and Upstream of Property, Unrealized Gain and Realized Gain On SaleMa'arifa HussainNo ratings yet

- Nepomuceno, Henry James B. - Ast Quiz 5Document2 pagesNepomuceno, Henry James B. - Ast Quiz 5Mitch Tokong MinglanaNo ratings yet

- Mary The Queen College of Pampanga Inc.: Agency Accounting Focus NotesDocument16 pagesMary The Queen College of Pampanga Inc.: Agency Accounting Focus NotesAllain GuanlaoNo ratings yet

- ACC110 P3Quiz2 AnswersDocument12 pagesACC110 P3Quiz2 AnswersTricia Mae FernandezNo ratings yet

- Intercompany Inventory TransfersDocument2 pagesIntercompany Inventory TransfersTriechia LaudNo ratings yet

- AC7110-4 NADCAP Rev E Audit Checklist For Resistance Welding - Spot WeldingDocument27 pagesAC7110-4 NADCAP Rev E Audit Checklist For Resistance Welding - Spot WeldingCarlos TovarNo ratings yet

- Chapter 7 Notes Question Amp SolutionsDocument7 pagesChapter 7 Notes Question Amp SolutionsPankhuri SinghalNo ratings yet

- Conso FS Part 2Document5 pagesConso FS Part 2moNo ratings yet

- 3004 Home Office and BranchesDocument6 pages3004 Home Office and BranchesTatianaNo ratings yet

- Mga Dambieee!!!!: Complete Answer Pleaseee. Thank Youuu NO. Questions Answer 1 Answer 2 If Unsure Answer 1Document12 pagesMga Dambieee!!!!: Complete Answer Pleaseee. Thank Youuu NO. Questions Answer 1 Answer 2 If Unsure Answer 1Hannah Jane UmbayNo ratings yet

- Practice Problems AcctgDocument10 pagesPractice Problems AcctgRichard ColeNo ratings yet

- Midterm Exams - Pract 2 (1st Sem 2012-2013)Document13 pagesMidterm Exams - Pract 2 (1st Sem 2012-2013)jjjjjjjjjjjjjjjNo ratings yet

- Chapter 11 Advance Accounting SolmanDocument12 pagesChapter 11 Advance Accounting SolmanShiela GumamelaNo ratings yet

- Chapter12 - AnswerDocument26 pagesChapter12 - AnswerAubreyNo ratings yet

- AFAR CHAPTER 1O Questions (AutoRecovered)Document76 pagesAFAR CHAPTER 1O Questions (AutoRecovered)Acey Fletcher Padua SyNo ratings yet

- Chapter 16 Advacc2Document60 pagesChapter 16 Advacc2AnneShannenBambaDabuNo ratings yet

- Problem 11 AFARDocument4 pagesProblem 11 AFARNorman Delirio0% (1)

- Audit Liability 04 Chapter 7Document1 pageAudit Liability 04 Chapter 7Ma Teresa B. CerezoNo ratings yet

- Ias 28 Asynch Activity 9-30-20Document1 pageIas 28 Asynch Activity 9-30-20AngeloNo ratings yet

- Intercompany Sale of PPE ActivityDocument2 pagesIntercompany Sale of PPE Activitybea kullin0% (1)

- Separate and Consolidated Dayag Part 6Document4 pagesSeparate and Consolidated Dayag Part 6NinaNo ratings yet

- Chapter 16Document27 pagesChapter 16Red Christian Palustre100% (1)

- Home Office and Branch AccountingDocument7 pagesHome Office and Branch AccountingRujean Salar AltejarNo ratings yet

- Solution Chapter 9Document15 pagesSolution Chapter 9BobslaneLlenos0% (2)

- Practice Set 1 (Modules 1 - 3) 371Document8 pagesPractice Set 1 (Modules 1 - 3) 371Marielle CastañedaNo ratings yet

- Chapter 14 Other SolutionDocument18 pagesChapter 14 Other SolutionChristine BaguioNo ratings yet

- Use The Following Information For Question 1 and 2Document12 pagesUse The Following Information For Question 1 and 2Leah Mae NolascoNo ratings yet

- Franchise Accounting - DoneDocument3 pagesFranchise Accounting - DoneJymldy EnclnNo ratings yet

- Notes On Foreign TranslationDocument3 pagesNotes On Foreign TranslationcpacpacpaNo ratings yet

- Sample Problems For Construction AccountingDocument2 pagesSample Problems For Construction AccountingHernandez Aliah Cyril M.No ratings yet

- HFDSDHDocument8 pagesHFDSDHMary Grace Castillo AlmonedaNo ratings yet

- Business CombinationDocument10 pagesBusiness CombinationLora Mae JuanitoNo ratings yet

- Busicom Prob 6-8Document7 pagesBusicom Prob 6-8JrllsyNo ratings yet

- Cpar - P2 09.15.13Document22 pagesCpar - P2 09.15.13Leo Mark Ramos100% (1)

- Psa 550 PDFDocument9 pagesPsa 550 PDFLen AlairNo ratings yet

- Advac Solmal Chapter 13Document16 pagesAdvac Solmal Chapter 13john paul100% (1)

- Balance Sheet QUESTIONANSWERDocument19 pagesBalance Sheet QUESTIONANSWERJoyce Ann Agdippa BarcelonaNo ratings yet

- Pinnacle in House CPA Review Tuition Fee UpdatedDocument1 pagePinnacle in House CPA Review Tuition Fee UpdatedRaRa SantiagoNo ratings yet

- Cpa Review School of The Philippines ManilaDocument4 pagesCpa Review School of The Philippines Manilaxara mizpahNo ratings yet

- Abc Stock AcquisitionDocument13 pagesAbc Stock AcquisitionMary Joy Albandia100% (1)

- 07 Installment SalesDocument1 page07 Installment SalesGem Yiel33% (3)

- BUSCOM ActivityDocument14 pagesBUSCOM ActivityLerma MarianoNo ratings yet

- AdvactDocument8 pagesAdvactJay Anne Marie MontalesNo ratings yet

- Chapter 18 Part 1Document61 pagesChapter 18 Part 1Hannah KatNo ratings yet

- Problem 3&5Document17 pagesProblem 3&5panda 1No ratings yet

- AFAR02 04 Franchise AccountingDocument4 pagesAFAR02 04 Franchise AccountingNicoleNo ratings yet

- Consolidated Financial Statements - Acquistion DateDocument52 pagesConsolidated Financial Statements - Acquistion DateXavier AresNo ratings yet

- Consolidated Net IncomeDocument1 pageConsolidated Net IncomePJ PoliranNo ratings yet

- Business Combination AssignmentDocument5 pagesBusiness Combination AssignmentBienvenido JmNo ratings yet

- Chapter 3 The Government Accounting ProcessDocument10 pagesChapter 3 The Government Accounting ProcessEthel Joy Tolentino GamboaNo ratings yet

- WEEK 5 AFAR.04 Business Combination DrillDocument10 pagesWEEK 5 AFAR.04 Business Combination DrillHermz ComzNo ratings yet

- Aa 3Document4 pagesAa 3Unknown 01No ratings yet

- Home OfficeDocument4 pagesHome OfficeAries Gonzales CaraganNo ratings yet

- Advanced Accounting Part 2 Dayag 2015 Chapter 4 (2022)Document68 pagesAdvanced Accounting Part 2 Dayag 2015 Chapter 4 (2022)Mazikeen DeckerNo ratings yet

- Bsais 4JDocument18 pagesBsais 4JArjay DeausenNo ratings yet

- AP.2901 Inventories.Document9 pagesAP.2901 Inventories.Alarich CatayocNo ratings yet

- SUBJECT: Accounting 15 DESCIPTIVE TITLE: Accounting For Business CombinationDocument5 pagesSUBJECT: Accounting 15 DESCIPTIVE TITLE: Accounting For Business CombinationRajah Calica100% (2)

- Exam 2Document19 pagesExam 2SHE50% (2)

- MIDTERM EXAM FDocument14 pagesMIDTERM EXAM FJoyce LunaNo ratings yet

- ACCOUNTING FOR SPECIAL TRANSACTIONS - Installment SalesDocument25 pagesACCOUNTING FOR SPECIAL TRANSACTIONS - Installment SalesDewdrop Mae RafananNo ratings yet

- Intercompany Sale of PropertyDocument6 pagesIntercompany Sale of PropertyClauie BarsNo ratings yet

- Assignment 3Document6 pagesAssignment 3Triechia LaudNo ratings yet

- Contract of SaleDocument8 pagesContract of SaleTriechia LaudNo ratings yet

- Current Yield Capital Gains Yield Total Return: SolutionDocument1 pageCurrent Yield Capital Gains Yield Total Return: SolutionTriechia LaudNo ratings yet

- Financial Ratio AnalysisDocument32 pagesFinancial Ratio AnalysisTriechia LaudNo ratings yet

- Assignment: Triechia Laud Bsacc 3ADocument3 pagesAssignment: Triechia Laud Bsacc 3ATriechia LaudNo ratings yet

- Consolidated Financial StatementDocument5 pagesConsolidated Financial StatementTriechia LaudNo ratings yet

- Reflective Journal 2 - Initiating The ProjectDocument4 pagesReflective Journal 2 - Initiating The Projectshubham thakurNo ratings yet

- Pecb Iso 37001 Lead Implementer Exam Preparation GuideDocument16 pagesPecb Iso 37001 Lead Implementer Exam Preparation Guidemrustamov84No ratings yet

- ITC June 2023 Paper 2 Question SAMPDocument9 pagesITC June 2023 Paper 2 Question SAMPmapindukwatinotendaNo ratings yet

- P.O.B Business Finance Lesson NotesDocument4 pagesP.O.B Business Finance Lesson Notesnathaliamoses09No ratings yet

- Profit, Loss and Break-EvenDocument12 pagesProfit, Loss and Break-EvenAngelie Faith MacairanNo ratings yet

- PRD DipankarDocument53 pagesPRD Dipankarh23079No ratings yet

- Chapter 2Document43 pagesChapter 2Sara SaraNo ratings yet

- Appointment & TerminationDocument5 pagesAppointment & TerminationPaki PinguNo ratings yet

- Esk Co-Audit RiskDocument2 pagesEsk Co-Audit RiskAmeet SinghNo ratings yet

- Hospital Cost ContainmentDocument32 pagesHospital Cost Containmentcandraferdianhandri100% (1)

- Suggested Solution: BHMH2002 Introduction To Economics Individual Assignment II (S2, 2021)Document3 pagesSuggested Solution: BHMH2002 Introduction To Economics Individual Assignment II (S2, 2021)Chi Chung LamNo ratings yet

- Chapter 1, Lesson 3: Marketing Origins, Exchange, and ValueDocument22 pagesChapter 1, Lesson 3: Marketing Origins, Exchange, and ValuePrincess Camille dela PenaNo ratings yet

- 'Nitu Granzulea Silviu Mihai LU - 19.09.23Document2 pages'Nitu Granzulea Silviu Mihai LU - 19.09.23Roman ClaudiaNo ratings yet

- Kamala Shrestha ValuationDocument7 pagesKamala Shrestha Valuationkrishnachauhan.npNo ratings yet

- Visual ManagementDocument2 pagesVisual ManagementShiv PandyaNo ratings yet

- Case Application 1 An Ethical Hotel Where Disabled People Can Find Their WayDocument3 pagesCase Application 1 An Ethical Hotel Where Disabled People Can Find Their Waysmart asusualNo ratings yet

- MR Process & Problem FormulationDocument28 pagesMR Process & Problem FormulationDeepanshu KaushikNo ratings yet

- Modern Construction 1Document43 pagesModern Construction 1kaleab tassewNo ratings yet

- Criv June 2024 AmendmentsDocument16 pagesCriv June 2024 Amendmentsshivaagra6969No ratings yet

- Microsoft Certified: Power Platform App Maker Associate - Skills MeasuredDocument4 pagesMicrosoft Certified: Power Platform App Maker Associate - Skills MeasuredkarijosephNo ratings yet

- Priprema Projekata: Beograd, 13.04.2011 Tatjana VolarevDocument78 pagesPriprema Projekata: Beograd, 13.04.2011 Tatjana VolarevKriszta KovacsNo ratings yet

- Michael E. Gerber - The E-Myth Revisited - Why Most Small Businesses Don't Work and What To Do About It-HarperCollins (1995)Document286 pagesMichael E. Gerber - The E-Myth Revisited - Why Most Small Businesses Don't Work and What To Do About It-HarperCollins (1995)TBSS100% (2)

- Balaji Private Limited ReportDocument92 pagesBalaji Private Limited ReportShifanNo ratings yet

- IB Business Management Graphic Organiser Section 1 Business Organisation and Environment - 1.1 IntroductionDocument4 pagesIB Business Management Graphic Organiser Section 1 Business Organisation and Environment - 1.1 IntroductionPatt SantistevanNo ratings yet

- Programme Brief and Script Format of VideoDocument12 pagesProgramme Brief and Script Format of VideoKUMAR YASHNo ratings yet

- REAA - CPPREP4001 - Work in The Real Estate Industry Report v1.9Document31 pagesREAA - CPPREP4001 - Work in The Real Estate Industry Report v1.9weterechaseNo ratings yet

- UPK 4a COMPLETEDDocument14 pagesUPK 4a COMPLETEDHannan__AhmedNo ratings yet