MRF Limited Fundamental Analysis

MRF Limited Fundamental Analysis

Download as pdf or txt

You might also like

- Kalyan Jewellers HSBC 3oct2022Document33 pagesKalyan Jewellers HSBC 3oct2022Ankk Tenderz100% (1)

- Sale Smart's+Financial+Ratios+PackDocument23 pagesSale Smart's+Financial+Ratios+PackDenisa ZahariaNo ratings yet

- Hindalco'S Acquisition of Novelis: The Making of A GiantDocument11 pagesHindalco'S Acquisition of Novelis: The Making of A GiantHarshShahNo ratings yet

- Mahindra PESTELDocument2 pagesMahindra PESTELankushvictor100% (1)

- Business Marketing Term 5: PGDM 2017-19: Submitted byDocument8 pagesBusiness Marketing Term 5: PGDM 2017-19: Submitted bySaurabh Singh0% (1)

- Britannia Industries Financial ReportDocument15 pagesBritannia Industries Financial ReportKunal DesaiNo ratings yet

- Organistion Study MRFDocument81 pagesOrganistion Study MRFAkhil ThomasNo ratings yet

- Relaxo DistributionDocument19 pagesRelaxo DistributionamitmadaanNo ratings yet

- History and Development of Amul Indusries Pvt. Ltd.Document79 pagesHistory and Development of Amul Indusries Pvt. Ltd.asn8136No ratings yet

- The Indian Tyre IndustryDocument11 pagesThe Indian Tyre Industryshivi yoloNo ratings yet

- Apollo Tyres and BKTDocument25 pagesApollo Tyres and BKTKoushik G Sai100% (1)

- Arvind MillsDocument52 pagesArvind Millszsjkc20No ratings yet

- Report On Motivation With Reference To J K TyreDocument89 pagesReport On Motivation With Reference To J K TyreChandan ArmorNo ratings yet

- Automotive Tyre Manufacturers' Association (ATMA)Document21 pagesAutomotive Tyre Manufacturers' Association (ATMA)flower87No ratings yet

- Naina Arvind MillsDocument28 pagesNaina Arvind MillsMini Goel100% (1)

- Final Report Passenger CarsDocument20 pagesFinal Report Passenger CarsAditya Nagpal100% (2)

- On Nirma CaseDocument36 pagesOn Nirma CaseMuskaan ChaudharyNo ratings yet

- Be - Term 2 B 36 2019Document6 pagesBe - Term 2 B 36 2019santosh vighneshwar hegdeNo ratings yet

- Reliance Industries HardDocument51 pagesReliance Industries HardSiddhi JainNo ratings yet

- Industry Analysis: Ultratech CementDocument3 pagesIndustry Analysis: Ultratech CementMohit MantryNo ratings yet

- Ralson (India) LimitedDocument11 pagesRalson (India) LimitedAmit KumarNo ratings yet

- Air India: Product and Brand ManagementDocument34 pagesAir India: Product and Brand ManagementRaman Khatkar100% (1)

- Presentation On F&G Retail in IndiaDocument81 pagesPresentation On F&G Retail in Indiamigpatel7970100% (1)

- Eic-Itc Kirti SabranDocument14 pagesEic-Itc Kirti Sabrankirti sabranNo ratings yet

- Force TractorDocument77 pagesForce Tractorshreestationery2016No ratings yet

- Swot Analysis of MaruthiDocument4 pagesSwot Analysis of Maruthisvpriya233282No ratings yet

- Docslide - Us HR Training Britannia Shruti ProjectDocument76 pagesDocslide - Us HR Training Britannia Shruti Projectsaurabhty87No ratings yet

- Automobile IndustryDocument15 pagesAutomobile Industryanoop_mishra1986No ratings yet

- Company Brief PDFDocument18 pagesCompany Brief PDFSansha BolarNo ratings yet

- Corporate Finance - MRF CompanyDocument24 pagesCorporate Finance - MRF CompanyAneesh GargNo ratings yet

- Sugarcane Industry: Indian Institute of Plantation Management-Bengaluru KarnatakaDocument31 pagesSugarcane Industry: Indian Institute of Plantation Management-Bengaluru KarnatakaMohit SharmaNo ratings yet

- BritanniaDocument14 pagesBritanniaNidHi KulKarniNo ratings yet

- Tyre Industry AnalysisDocument14 pagesTyre Industry AnalysisRickMartinNo ratings yet

- FastrackDocument18 pagesFastrackTanmoy Guha100% (1)

- HDFC FinalDocument19 pagesHDFC FinalLavina JainNo ratings yet

- Classmate 1Document11 pagesClassmate 1Shivam Maurya100% (1)

- 1.1 Introduction About The StudyDocument37 pages1.1 Introduction About The StudyArun Kumar100% (1)

- Arvind Mills Strategic FactorsDocument2 pagesArvind Mills Strategic Factorsnitz mNo ratings yet

- Aditya Birla Fashion - Motilal Oswal - AR AnalysisDocument24 pagesAditya Birla Fashion - Motilal Oswal - AR Analysisvipul sharmaNo ratings yet

- 07c Low-Cost Carriers in India SpiceJets PerspectiveDocument4 pages07c Low-Cost Carriers in India SpiceJets PerspectiveSubhadra Haribabu100% (1)

- Project Report On The Genesis of Hindustan Unilever Limited (HUL)Document44 pagesProject Report On The Genesis of Hindustan Unilever Limited (HUL)swapnil panmandNo ratings yet

- Premium Bike Market in IndiaDocument5 pagesPremium Bike Market in Indiaarun_gauravNo ratings yet

- Project Report ON Fundamental Analysis of Indian Automobile IndustryDocument31 pagesProject Report ON Fundamental Analysis of Indian Automobile IndustryJenny Johnson100% (1)

- Globalization of Indian Automobile IndustryDocument25 pagesGlobalization of Indian Automobile IndustryAjay Singla100% (2)

- Change Management in Mrf...Document84 pagesChange Management in Mrf...Arun_Shankar_K_52390% (1)

- Tata Consumer - CFS Analysis COMPLETEDocument10 pagesTata Consumer - CFS Analysis COMPLETEPratham MalhotraNo ratings yet

- Scorpio PPT BY AMGSSDocument26 pagesScorpio PPT BY AMGSSGaurav DeshwalNo ratings yet

- CEAT Limited: Navigation SearchDocument5 pagesCEAT Limited: Navigation SearchImran MohammedNo ratings yet

- Group-3 - Tata Bluescope Case - BWDocument21 pagesGroup-3 - Tata Bluescope Case - BWAnkit Bansal100% (2)

- Tata Motors JLR Group 6Document36 pagesTata Motors JLR Group 6Anirban ChakrabortyNo ratings yet

- Initiating Coverage - Indian Hume Pipe Co.Document38 pagesInitiating Coverage - Indian Hume Pipe Co.rroshhNo ratings yet

- Tata Motors PresentationDocument39 pagesTata Motors PresentationSarita GoelNo ratings yet

- COMPANY Profile & Industry Profile - 230912 - 000923Document4 pagesCOMPANY Profile & Industry Profile - 230912 - 000923dhanushvaryadhanuNo ratings yet

- Itc OmDocument31 pagesItc Omreddevil911No ratings yet

- Industry ProfileDocument20 pagesIndustry ProfileShanu shriNo ratings yet

- Voltas 1Document85 pagesVoltas 1Kuldeep Batra100% (1)

- Tata - BSL Final.Document15 pagesTata - BSL Final.Shubham MishraNo ratings yet

- Economics Assignment Impact of COVID-19 On Indian EconomyDocument5 pagesEconomics Assignment Impact of COVID-19 On Indian EconomyAbhishek SaravananNo ratings yet

- The Impact of Covid-19 On The Indian Economy.Document22 pagesThe Impact of Covid-19 On The Indian Economy.Mahira SarafNo ratings yet

- Eic AnalysisDocument17 pagesEic AnalysisJaydeep Bairagi100% (1)

- Heteroscedastcity - Cross SectionalDocument1 pageHeteroscedastcity - Cross SectionalMaryNo ratings yet

- International Trade 1. What Are The Top Exported Items From Taiwan? 2019-2020Document2 pagesInternational Trade 1. What Are The Top Exported Items From Taiwan? 2019-2020MaryNo ratings yet

- Sample Size 100 Sample Number of Defects P UCL LCLDocument9 pagesSample Size 100 Sample Number of Defects P UCL LCLMaryNo ratings yet

- Cogs 3. P&L A/c: Particulars Amount RevenueDocument1 pageCogs 3. P&L A/c: Particulars Amount RevenueMaryNo ratings yet

- Income Statement Particulars Amount RevenueDocument1 pageIncome Statement Particulars Amount RevenueMaryNo ratings yet

- X Bar Chart: Sample Size 5 A2 0.577 D3 0 D4 2.114 1 2 3 4 5 AverageDocument3 pagesX Bar Chart: Sample Size 5 A2 0.577 D3 0 D4 2.114 1 2 3 4 5 AverageMaryNo ratings yet

- Final SumsDocument12 pagesFinal SumsMaryNo ratings yet

- Dutt Company (PG No 483) : Cash Flow From Operating ActivitiesDocument3 pagesDutt Company (PG No 483) : Cash Flow From Operating ActivitiesMaryNo ratings yet

- Timeline 0 1 2 3 4 5 6 7 8 RDDocument2 pagesTimeline 0 1 2 3 4 5 6 7 8 RDMaryNo ratings yet

- Abhijit Company (PG No 483) : Cash Flow From Operating ActivitiesDocument4 pagesAbhijit Company (PG No 483) : Cash Flow From Operating ActivitiesMaryNo ratings yet

- Navin Packaging LTD: Share Capital A/cDocument4 pagesNavin Packaging LTD: Share Capital A/cMaryNo ratings yet

- Sikandhar Company (PG No 484) : Cash Flow From Operating ActivitiesDocument6 pagesSikandhar Company (PG No 484) : Cash Flow From Operating ActivitiesMaryNo ratings yet

- Problem 5.1Document3 pagesProblem 5.1MaryNo ratings yet

- Date Purchase Issue Balance: Problem 5.7 LifoDocument5 pagesDate Purchase Issue Balance: Problem 5.7 LifoMaryNo ratings yet

- Kapoor Software LTD CRCTD AnswerDocument9 pagesKapoor Software LTD CRCTD AnswerMaryNo ratings yet

- Problem 5.9: Product Group IDocument1 pageProblem 5.9: Product Group IMaryNo ratings yet

- LEISURE ON JULY 31STDocument4 pagesLEISURE ON JULY 31STMaryNo ratings yet

- Group Assignment MN 3042 Financial Accounting Group AssignmentDocument3 pagesGroup Assignment MN 3042 Financial Accounting Group AssignmentSenthooran SrikandarajNo ratings yet

- Public Sector Accounting Cat1 March 2022Document4 pagesPublic Sector Accounting Cat1 March 2022hasfa konsoNo ratings yet

- Report On Violations (RMO 15-2018)Document12 pagesReport On Violations (RMO 15-2018)Christian Albert HerreraNo ratings yet

- Interim and Segment ReportingDocument6 pagesInterim and Segment Reportingallforgod19No ratings yet

- Faa Bba Sem I - Unit 1 and 2Document14 pagesFaa Bba Sem I - Unit 1 and 2kochars321No ratings yet

- User Manual - : Title: Module NameDocument13 pagesUser Manual - : Title: Module NamesrinivasNo ratings yet

- See It, Understand It, Use It: Accounting DefinitionsDocument29 pagesSee It, Understand It, Use It: Accounting Definitionsbha27111992No ratings yet

- Zra Commission of Inquiry - Final ReportDocument117 pagesZra Commission of Inquiry - Final ReportChola MukangaNo ratings yet

- Challenge Exam Study Material 2013Document85 pagesChallenge Exam Study Material 2013iluvhuggies100% (1)

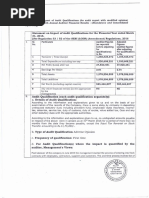

- Standalone Statement On Impact of Audit Qualifications For The Period Ended March 31, 2016 (Company Update)Document2 pagesStandalone Statement On Impact of Audit Qualifications For The Period Ended March 31, 2016 (Company Update)Shyam SunderNo ratings yet

- vAD1-Piotroski F Score Spreadsheet FreeDocument4 pagesvAD1-Piotroski F Score Spreadsheet FreesatishcreativeNo ratings yet

- Aurobindo Pharma Final Report PDFDocument18 pagesAurobindo Pharma Final Report PDFAbhimanyu HedaNo ratings yet

- 2024-04-17-ORAN - PA-PriceTarget Research-ORANGE Investment Status Report-107661749Document70 pages2024-04-17-ORAN - PA-PriceTarget Research-ORANGE Investment Status Report-107661749Jerónimo BedoyaNo ratings yet

- Financial Statement AnalysisDocument3 pagesFinancial Statement AnalysisAsad Rehman100% (1)

- Syllabus: Cambridge IGCSE AccountingDocument21 pagesSyllabus: Cambridge IGCSE AccountingilovethelettermNo ratings yet

- BudgetDocument8 pagesBudgetjasim ansariNo ratings yet

- Annual: For The Year Ended 31 December 2019Document184 pagesAnnual: For The Year Ended 31 December 2019ирина щурNo ratings yet

- 09 Southwest AirDocument13 pages09 Southwest AirmskrierNo ratings yet

- ZF Commercial Vehicle Control Systems India Limited: 18 Annual Report 2022Document202 pagesZF Commercial Vehicle Control Systems India Limited: 18 Annual Report 2022Anh TranNo ratings yet

- Toaz - Info Question 1 Solution PRDocument4 pagesToaz - Info Question 1 Solution PRCmNo ratings yet

- FundafinDocument5 pagesFundafinvarinay1611No ratings yet

- Intercompany TransactionsDocument7 pagesIntercompany TransactionsJulie Mae Caling MalitNo ratings yet

- FM No3Document2 pagesFM No3siti louNo ratings yet

- Cash Management at MarutiDocument68 pagesCash Management at MarutiEshaNo ratings yet

- Current LiabilitiesDocument20 pagesCurrent LiabilitiesM Dwi PadilaNo ratings yet

- Accounting Worksheet Number OneDocument4 pagesAccounting Worksheet Number OneJevoun Tyrell100% (1)

- Chap 1 IntroductionDocument32 pagesChap 1 IntroductionShaaru TharshiniNo ratings yet

- Ratio AnalysisDocument11 pagesRatio AnalysisPrashant BhadauriaNo ratings yet

- Waterfall Chart: Total Revenues - Company Total Revenues - CategoryDocument10 pagesWaterfall Chart: Total Revenues - Company Total Revenues - CategoryEvert TrochNo ratings yet