Target Corporation - Simple Operating Model: General Assumptions

Target Corporation - Simple Operating Model: General Assumptions

Download as xlsx, pdf, or txt

You might also like

- BigTech Analysis - Example AnswerDocument22 pagesBigTech Analysis - Example AnswerÚdita ShNo ratings yet

- Colgate Financial ModelDocument34 pagesColgate Financial ModelRendy Oliver Mariano PonoNo ratings yet

- Is Excel Participant - Simplified v2Document9 pagesIs Excel Participant - Simplified v2Yash JasaparaNo ratings yet

- Apple & RIM Merger Model and LBO ModelDocument50 pagesApple & RIM Merger Model and LBO ModelDarshana MathurNo ratings yet

- Financial Model - Colgate Palmolive (Unsolved Template) : Prepared by Dheeraj Vaidya, CFA, FRMDocument35 pagesFinancial Model - Colgate Palmolive (Unsolved Template) : Prepared by Dheeraj Vaidya, CFA, FRMahmad syaifudinNo ratings yet

- Acco 365 Review Class QuestionsDocument31 pagesAcco 365 Review Class QuestionsHeyue XiaoNo ratings yet

- Solutions and Test Bank For Fundamentals of Financial Management 16th Edition 16e by Eugene F BrighamDocument68 pagesSolutions and Test Bank For Fundamentals of Financial Management 16th Edition 16e by Eugene F BrighamDiệp Phạm HồngNo ratings yet

- 3 Statement Model - BlankDocument6 pages3 Statement Model - BlankAina Michael100% (1)

- IBIG 06 01 Three Statements 30 Minutes BlankDocument5 pagesIBIG 06 01 Three Statements 30 Minutes BlankSiddesh NaikNo ratings yet

- 107 10 DCF Sanity Check AfterDocument6 pages107 10 DCF Sanity Check AfterDavid ChikhladzeNo ratings yet

- Financial Modelling Assessment - 3s Lumber CompanyDocument5 pagesFinancial Modelling Assessment - 3s Lumber CompanySharaz AliNo ratings yet

- SELFDocument7 pagesSELFSIDDHANT CHUGHNo ratings yet

- UntitledDocument11 pagesUntitledJames BondNo ratings yet

- IBIG 06 01 Three Statements 30 Minutes CompleteDocument5 pagesIBIG 06 01 Three Statements 30 Minutes CompletenisNo ratings yet

- Walmart Inc. - Operating Model and Valuation - Cover Page and NavigationDocument24 pagesWalmart Inc. - Operating Model and Valuation - Cover Page and Navigationmerag76668No ratings yet

- Walmart Inc. - Operating Model and Valuation - Cover Page and NavigationDocument24 pagesWalmart Inc. - Operating Model and Valuation - Cover Page and NavigationKate RuzevichNo ratings yet

- Walmart Inc. - Operating Model and Valuation - Cover Page and NavigationDocument25 pagesWalmart Inc. - Operating Model and Valuation - Cover Page and NavigationKate RuzevichNo ratings yet

- Drivers: FY 19 FY 20 FY 21 FY 22Document6 pagesDrivers: FY 19 FY 20 FY 21 FY 22Ammon BelyonNo ratings yet

- 04 06 Public Comps Valuation Multiples AfterDocument19 pages04 06 Public Comps Valuation Multiples AfterShanto Arif Uz ZamanNo ratings yet

- 101 01 90 Minute Case Study Otis CompleteDocument12 pages101 01 90 Minute Case Study Otis CompleteisabellazhovNo ratings yet

- 1/29/2010 2009 360 Apple Inc. 2010 $1,000 $192.06 1000 30% 900,678Document18 pages1/29/2010 2009 360 Apple Inc. 2010 $1,000 $192.06 1000 30% 900,678X.r. GeNo ratings yet

- Alzona Corporation: General AssumptionsDocument2 pagesAlzona Corporation: General Assumptionschintan desaiNo ratings yet

- MNI ValuationDocument17 pagesMNI ValuationBhardwaj VarmaNo ratings yet

- Is Excel Participant - Simplified v2Document9 pagesIs Excel Participant - Simplified v2dikshapatil6789No ratings yet

- Is Excel Participant Samarth - Simplified v2Document9 pagesIs Excel Participant Samarth - Simplified v2samarth halliNo ratings yet

- Colgate Financial Model SolvedDocument36 pagesColgate Financial Model SolvedSundara MoorthyNo ratings yet

- Exxaro Tiles LTD Model 2024Document10 pagesExxaro Tiles LTD Model 2024rakaggarwal03No ratings yet

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2animecommunity04100% (1)

- Microsoft Investment AnalysisDocument4 pagesMicrosoft Investment AnalysisdkrauzaNo ratings yet

- Please Click On The Link For The Report:: cm09MjgDocument2 pagesPlease Click On The Link For The Report:: cm09Mjgneil5mNo ratings yet

- BigTech - Excel TemplateDocument21 pagesBigTech - Excel TemplateAjay GuptaNo ratings yet

- Balkrishna Industries LTD: Investor Presentation February 2020Document30 pagesBalkrishna Industries LTD: Investor Presentation February 2020PIBM MBA-FINANCENo ratings yet

- Finance Final Pitch General ElectricDocument8 pagesFinance Final Pitch General Electricbquinn08No ratings yet

- BIWS Atlassian 3 Statement Model - VFDocument8 pagesBIWS Atlassian 3 Statement Model - VFJohnny BravoNo ratings yet

- IS Excel Participant (Risit Savani) - Simplified v2Document9 pagesIS Excel Participant (Risit Savani) - Simplified v2risitsavaniNo ratings yet

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2Medhansh ShindeNo ratings yet

- 3 Statement Model TemplateDocument5 pages3 Statement Model TemplateAbdullah khanNo ratings yet

- Chapter 3 Problem 15: Aquatic Supplies Co. INCOME STATEMENT ($ Millions) 2017 AssumptionsDocument9 pagesChapter 3 Problem 15: Aquatic Supplies Co. INCOME STATEMENT ($ Millions) 2017 AssumptionsShaharyar AsifNo ratings yet

- Q4 FY24 Financial TablesDocument10 pagesQ4 FY24 Financial Tablesgentlerain0602No ratings yet

- Horizontal Analysis Formula Excel TemplateDocument5 pagesHorizontal Analysis Formula Excel Templatesexy samuelNo ratings yet

- Activity 3 123456789Document7 pagesActivity 3 123456789Jeramie Sarita SumaotNo ratings yet

- SFH Rental AnalysisDocument6 pagesSFH Rental AnalysisA jNo ratings yet

- FTNT - Q2'21 Investor Slides FinalDocument14 pagesFTNT - Q2'21 Investor Slides FinalJOhnNo ratings yet

- Estados Financieros Colgate. Analísis Vertical y HorizontalDocument5 pagesEstados Financieros Colgate. Analísis Vertical y HorizontalXimena Isela Villalpando BuenoNo ratings yet

- PrepzFy - LBO - VemptyDocument3 pagesPrepzFy - LBO - VemptykouakouNo ratings yet

- Emmtrix Technologies GMBH v4Document72 pagesEmmtrix Technologies GMBH v4bzboardzNo ratings yet

- Pag BankDocument22 pagesPag Bankandre.torresNo ratings yet

- Task 1 BigTech TemplateDocument5 pagesTask 1 BigTech Templatedaniyalansari.8425No ratings yet

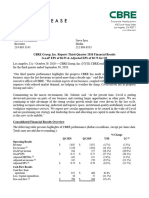

- 2020.Q3 Earnings Release FinalDocument16 pages2020.Q3 Earnings Release FinalAhmed EldessoukyNo ratings yet

- 2021 Annual Property & Casualty and Title Insurance Industry ReportDocument19 pages2021 Annual Property & Casualty and Title Insurance Industry ReporttheupashiNo ratings yet

- Maruti Suzuki ValuationDocument39 pagesMaruti Suzuki ValuationritususmitakarNo ratings yet

- Credit RatingDocument11 pagesCredit Ratingmandar1989No ratings yet

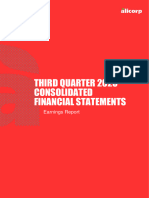

- Alicorp Earnings Report 3Q23 EN VFDocument23 pagesAlicorp Earnings Report 3Q23 EN VFADRIAN ANIBAL ENCISO ARKNo ratings yet

- XLS EngDocument21 pagesXLS EngRudra BarotNo ratings yet

- Income Statement: Financial StatementsDocument15 pagesIncome Statement: Financial StatementsMahnoorNo ratings yet

- Common Size Income StatementDocument7 pagesCommon Size Income StatementUSD 654No ratings yet

- Colgate Ratio Analysis WSM 2020 SolvedDocument17 pagesColgate Ratio Analysis WSM 2020 Solvedabi habudinNo ratings yet

- Nvidia's CFO CommentaryDocument8 pagesNvidia's CFO CommentaryTim MooreNo ratings yet

- SIA Grubhub Suggested SolutionDocument1 pageSIA Grubhub Suggested SolutionAnushka GuptaNo ratings yet

- SENEA Financial AnalysisDocument22 pagesSENEA Financial Analysissidrajaffri72No ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Economic and Business Forecasting: Analyzing and Interpreting Econometric ResultsFrom EverandEconomic and Business Forecasting: Analyzing and Interpreting Econometric ResultsNo ratings yet

- 03 RecordingBusinessTransactions FinancialAccountingDocument30 pages03 RecordingBusinessTransactions FinancialAccountingTahir DestaNo ratings yet

- Advanced Accounting 4Document2 pagesAdvanced Accounting 4Tax TrainingNo ratings yet

- All Practice Set SolutionsDocument22 pagesAll Practice Set SolutionsJohn TomNo ratings yet

- LAI Report PT KAI 31 Des 2017 PDFDocument136 pagesLAI Report PT KAI 31 Des 2017 PDFPark YonhwaNo ratings yet

- Lnvesco S&P 500 ESG UCITS ETF AceDocument2 pagesLnvesco S&P 500 ESG UCITS ETF AceGeorgio RomaniNo ratings yet

- FABM-1 - Module 9 - Preparation of WorksheetDocument7 pagesFABM-1 - Module 9 - Preparation of WorksheetKJ Jones100% (3)

- J.P. Morgan Asset Management - Guide To The Markets - JP Morgan - Q3 - 2022Document71 pagesJ.P. Morgan Asset Management - Guide To The Markets - JP Morgan - Q3 - 2022Cristian IstratescuNo ratings yet

- Deepening: Accountancy, Business and Management 2Document217 pagesDeepening: Accountancy, Business and Management 2Aly CalingacionNo ratings yet

- AFB Module B CHAPTER 1Document26 pagesAFB Module B CHAPTER 1cpk200No ratings yet

- VE EFB2 Tests ProgressTest03Document3 pagesVE EFB2 Tests ProgressTest03DamMayXanhNo ratings yet

- (Format) Business Plan TemplateDocument38 pages(Format) Business Plan TemplatetaneshNo ratings yet

- AFAR-19 (Not-for-Profit Organizations)Document18 pagesAFAR-19 (Not-for-Profit Organizations)Ide VelcoNo ratings yet

- Microsoft Outlook - Memo StyleDocument9 pagesMicrosoft Outlook - Memo Stylepheunsokchea168No ratings yet

- AAA-Mar PreMock AnswerDocument16 pagesAAA-Mar PreMock Answercatch_samNo ratings yet

- Capital Budgeting: 2. Cost and Benefit AnalysisDocument12 pagesCapital Budgeting: 2. Cost and Benefit AnalysisIfraNo ratings yet

- Chapter 13 CASH FLOWDocument2 pagesChapter 13 CASH FLOWKezia N. ApriliaNo ratings yet

- Topic 7 - Financial Leverage - Part 2Document35 pagesTopic 7 - Financial Leverage - Part 2Baby Khor100% (2)

- October 2nd, 2024 - Net Realizable ValueDocument6 pagesOctober 2nd, 2024 - Net Realizable Valuesahil.rambarose001No ratings yet

- Syllabus-NewTemplate CAE 125 Financial Management BSADocument6 pagesSyllabus-NewTemplate CAE 125 Financial Management BSADonna Zandueta-TumalaNo ratings yet

- SQA Accounting Assignment 1Document7 pagesSQA Accounting Assignment 1SENITH J100% (1)

- QuizDocument3 pagesQuizSam VNo ratings yet

- Accounting Principles AbDocument36 pagesAccounting Principles Absamson mutukuNo ratings yet

- Mutual Fund AssignmentDocument7 pagesMutual Fund AssignmentBhargav PathakNo ratings yet

- Chapter 7: Audit of Intangibles and Other Assets: Internal Control Over IntangiblesDocument28 pagesChapter 7: Audit of Intangibles and Other Assets: Internal Control Over IntangiblesUn knownNo ratings yet

- ACTBFAR Reflection #1Document2 pagesACTBFAR Reflection #1KRABBYPATTY PHNo ratings yet

- SIP Project 077 - Ubaid DhansayDocument40 pagesSIP Project 077 - Ubaid Dhansayiffu rautNo ratings yet

- Edieweiss Common Application FormDocument3 pagesEdieweiss Common Application FormNitinNo ratings yet

- InteDocument3 pagesInteBarcelona, Tricia Mae F.No ratings yet