100% found this document useful (1 vote)

2K viewsEPS Practice Problems

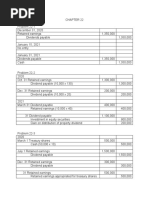

The document contains 8 practice problems related to calculating earnings per share (EPS). Problem 1 indicates that diluted EPS is calculated for companies with complex capital structures. Problems 2 through 7 walk through examples of calculating basic and diluted EPS using financial information provided, such as number of shares, convertible securities, and net income. Problem 8 determines whether a convertible bond or preferred stock is dilutive or anti-dilutive based on their impact on EPS. The document provides the calculations and reasoning for each problem.

Uploaded by

mikeCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

100% found this document useful (1 vote)

2K viewsEPS Practice Problems

The document contains 8 practice problems related to calculating earnings per share (EPS). Problem 1 indicates that diluted EPS is calculated for companies with complex capital structures. Problems 2 through 7 walk through examples of calculating basic and diluted EPS using financial information provided, such as number of shares, convertible securities, and net income. Problem 8 determines whether a convertible bond or preferred stock is dilutive or anti-dilutive based on their impact on EPS. The document provides the calculations and reasoning for each problem.

Uploaded by

mikeCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

/ 8