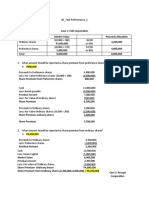

The document discusses the calculation of share premium arising from the issuance of shares. It states that the carrying amount of liability was P500,000, which was 1/4 of P2,000,000. It was reduced by the par value of shares issued of P200,000, resulting in a share premium of P300,000.

The document discusses the calculation of share premium arising from the issuance of shares. It states that the carrying amount of liability was P500,000, which was 1/4 of P2,000,000. It was reduced by the par value of shares issued of P200,000, resulting in a share premium of P300,000.

The document discusses the calculation of share premium arising from the issuance of shares. It states that the carrying amount of liability was P500,000, which was 1/4 of P2,000,000. It was reduced by the par value of shares issued of P200,000, resulting in a share premium of P300,000.

The document discusses the calculation of share premium arising from the issuance of shares. It states that the carrying amount of liability was P500,000, which was 1/4 of P2,000,000. It was reduced by the par value of shares issued of P200,000, resulting in a share premium of P300,000.