GCC Equity Report: Research

GCC Equity Report: Research

Download as pdf or txt

You might also like

- Calaveras VineyardsDocument12 pagesCalaveras Vineyardsapi-250891173100% (4)

- PC Ch. 11 Techniques of Capital BudgetingDocument22 pagesPC Ch. 11 Techniques of Capital BudgetingVinod Mathews100% (2)

- Module 6 AND 7 AnswerDocument30 pagesModule 6 AND 7 AnswerSophia DayaoNo ratings yet

- Excel Spreadsheet For Mergers and Acquisitions ValuationDocument6 pagesExcel Spreadsheet For Mergers and Acquisitions ValuationRenold DarmasyahNo ratings yet

- As S Ignment 2: Mccaw Cellular Communications: The at & T/Mccaw Merger NegotiationDocument9 pagesAs S Ignment 2: Mccaw Cellular Communications: The at & T/Mccaw Merger NegotiationSong LiNo ratings yet

- First Resources: Singapore Company FocusDocument7 pagesFirst Resources: Singapore Company FocusphuawlNo ratings yet

- Icici Bank: Performance HighlightsDocument15 pagesIcici Bank: Performance HighlightsAngel BrokingNo ratings yet

- Bank of BarodaDocument12 pagesBank of BarodaAngel BrokingNo ratings yet

- ITC Result UpdatedDocument15 pagesITC Result UpdatedAngel BrokingNo ratings yet

- TVS Motor Result UpdatedDocument12 pagesTVS Motor Result UpdatedAngel BrokingNo ratings yet

- Idea Cellular: Performance HighlightsDocument13 pagesIdea Cellular: Performance HighlightsAngel BrokingNo ratings yet

- Bank of IndiaDocument12 pagesBank of IndiaAngel BrokingNo ratings yet

- BUY Bank of India: Performance HighlightsDocument12 pagesBUY Bank of India: Performance Highlightsashish10mca9394No ratings yet

- Allcargo Global Logistics LTD.: CompanyDocument5 pagesAllcargo Global Logistics LTD.: CompanyjoycoolNo ratings yet

- Motherson Sumi Systems Result UpdatedDocument14 pagesMotherson Sumi Systems Result UpdatedAngel BrokingNo ratings yet

- Shoppers Stop 4qfy11 Results UpdateDocument5 pagesShoppers Stop 4qfy11 Results UpdateSuresh KumarNo ratings yet

- Axis Bank Result UpdatedDocument13 pagesAxis Bank Result UpdatedAngel BrokingNo ratings yet

- Central Bank of India Result UpdatedDocument10 pagesCentral Bank of India Result UpdatedAngel BrokingNo ratings yet

- Axis Bank Result UpdatedDocument13 pagesAxis Bank Result UpdatedAngel BrokingNo ratings yet

- IDBI Bank Result UpdatedDocument13 pagesIDBI Bank Result UpdatedAngel BrokingNo ratings yet

- Axis Bank: Performance HighlightsDocument13 pagesAxis Bank: Performance HighlightsAngel BrokingNo ratings yet

- L&T 4Q Fy 2013Document15 pagesL&T 4Q Fy 2013Angel BrokingNo ratings yet

- Reliance Communication Result UpdatedDocument11 pagesReliance Communication Result UpdatedAngel BrokingNo ratings yet

- NMDC Result UpdatedDocument7 pagesNMDC Result UpdatedAngel BrokingNo ratings yet

- IDBI Bank Result UpdatedDocument13 pagesIDBI Bank Result UpdatedAngel BrokingNo ratings yet

- Yes Bank: Performance HighlightsDocument12 pagesYes Bank: Performance HighlightsAngel BrokingNo ratings yet

- HCL Technologies: Performance HighlightsDocument15 pagesHCL Technologies: Performance HighlightsAngel BrokingNo ratings yet

- Dena Bank Result UpdatedDocument11 pagesDena Bank Result UpdatedAngel BrokingNo ratings yet

- Dena Bank Result UpdatedDocument10 pagesDena Bank Result UpdatedAngel BrokingNo ratings yet

- Tulip Telecom LTD: Results In-Line, Retain BUYDocument5 pagesTulip Telecom LTD: Results In-Line, Retain BUYadatta785031No ratings yet

- UCO Bank: Performance HighlightsDocument11 pagesUCO Bank: Performance HighlightsAngel BrokingNo ratings yet

- Canara Bank, 1Q FY 2014Document11 pagesCanara Bank, 1Q FY 2014Angel BrokingNo ratings yet

- Itnl 4Q Fy 2013Document13 pagesItnl 4Q Fy 2013Angel BrokingNo ratings yet

- Reliance Communication: Performance HighlightsDocument11 pagesReliance Communication: Performance HighlightsAngel BrokingNo ratings yet

- Bank of Baroda Result UpdatedDocument12 pagesBank of Baroda Result UpdatedAngel BrokingNo ratings yet

- Canara Bank Result UpdatedDocument11 pagesCanara Bank Result UpdatedAngel BrokingNo ratings yet

- State Bank of India: Performance HighlightsDocument15 pagesState Bank of India: Performance HighlightsRaaji BujjiNo ratings yet

- Hindalco: Performance HighlightsDocument15 pagesHindalco: Performance HighlightsAngel BrokingNo ratings yet

- Shriram City Union Finance: Healthy Growth, Elevated Credit Costs HoldDocument9 pagesShriram City Union Finance: Healthy Growth, Elevated Credit Costs HoldRohit ThapliyalNo ratings yet

- UCO Bank: Performance HighlightsDocument11 pagesUCO Bank: Performance HighlightsAngel BrokingNo ratings yet

- Bank of India Result UpdatedDocument12 pagesBank of India Result UpdatedAngel BrokingNo ratings yet

- Oriental Bank of CommerceDocument11 pagesOriental Bank of CommerceAngel BrokingNo ratings yet

- ICICI Bank Result UpdatedDocument16 pagesICICI Bank Result UpdatedAngel BrokingNo ratings yet

- Syndicate Bank Result UpdatedDocument11 pagesSyndicate Bank Result UpdatedAngel BrokingNo ratings yet

- Bank of Baroda, 1Q FY 2014Document12 pagesBank of Baroda, 1Q FY 2014Angel BrokingNo ratings yet

- Investor Presentation: Q2FY13 & H1FY13 UpdateDocument18 pagesInvestor Presentation: Q2FY13 & H1FY13 UpdategirishdrjNo ratings yet

- KEC International Result UpdatedDocument11 pagesKEC International Result UpdatedAngel BrokingNo ratings yet

- Dena Bank, 1Q FY 2014Document11 pagesDena Bank, 1Q FY 2014Angel BrokingNo ratings yet

- Blue Dart Express LTD.: CompanyDocument5 pagesBlue Dart Express LTD.: CompanygirishrajsNo ratings yet

- Bajaj Auto: Performance HighlightsDocument12 pagesBajaj Auto: Performance HighlightsAngel BrokingNo ratings yet

- Allahabad Bank Result UpdatedDocument11 pagesAllahabad Bank Result UpdatedAngel BrokingNo ratings yet

- Canara Bank: Performance HighlightsDocument11 pagesCanara Bank: Performance HighlightsAstitwa RathoreNo ratings yet

- CIL (Maintain Buy) 3QFY12 Result Update 25 January 2012 (IFIN)Document5 pagesCIL (Maintain Buy) 3QFY12 Result Update 25 January 2012 (IFIN)Gaayaatrii BehuraaNo ratings yet

- Axis Bank: Performance HighlightsDocument13 pagesAxis Bank: Performance HighlightsAngel BrokingNo ratings yet

- Punjab National Bank: Performance HighlightsDocument12 pagesPunjab National Bank: Performance HighlightsAngel BrokingNo ratings yet

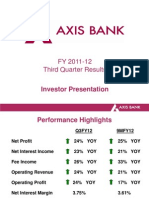

- FY 2011-12 Third Quarter Results: Investor PresentationDocument34 pagesFY 2011-12 Third Quarter Results: Investor PresentationshemalgNo ratings yet

- BIMBSec-Digi 20120724 2QFY12 Results ReviewDocument3 pagesBIMBSec-Digi 20120724 2QFY12 Results ReviewBimb SecNo ratings yet

- Ashok Leyland Result UpdatedDocument13 pagesAshok Leyland Result UpdatedAngel BrokingNo ratings yet

- Bosch 1qcy2014ru 290414Document12 pagesBosch 1qcy2014ru 290414Tirthajit SinhaNo ratings yet

- Tech Mahindra, 7th February, 2013Document12 pagesTech Mahindra, 7th February, 2013Angel BrokingNo ratings yet

- Allahabad Bank, 1Q FY 2014Document11 pagesAllahabad Bank, 1Q FY 2014Angel BrokingNo ratings yet

- ICICI Bank Result UpdatedDocument15 pagesICICI Bank Result UpdatedAngel BrokingNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Collection Agency Revenues World Summary: Market Values & Financials by CountryFrom EverandCollection Agency Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Financial Statement Analysis and Security Valuation: Related PapersDocument19 pagesFinancial Statement Analysis and Security Valuation: Related PapersIlham FajarNo ratings yet

- Agfs Part 8-V2Document15 pagesAgfs Part 8-V2ifyjoslynNo ratings yet

- Study Guide f9Document8 pagesStudy Guide f9KodwoPNo ratings yet

- 8685 - Strategic Financial ManagementDocument6 pages8685 - Strategic Financial ManagementAwais AhmedNo ratings yet

- Financial Management-Lecture 7Document26 pagesFinancial Management-Lecture 7TinoManhangaNo ratings yet

- Valuation 101: How To Do A Discounted Cashflow AnalysisDocument3 pagesValuation 101: How To Do A Discounted Cashflow AnalysisdevNo ratings yet

- Titman Ch1 3 PDFDocument87 pagesTitman Ch1 3 PDFMae Astoveza67% (3)

- 15.401 Finance TheoryDocument24 pages15.401 Finance TheoryMohamed ElmahgoubNo ratings yet

- Holistic Route SelectionDocument10 pagesHolistic Route SelectionrayzaNo ratings yet

- Cash Flow Forecast, Cost-Benefit Evaluation TechniquesDocument15 pagesCash Flow Forecast, Cost-Benefit Evaluation Techniqueswaqar chNo ratings yet

- Financial Modeling of M and ADocument9 pagesFinancial Modeling of M and Ashettymihir9No ratings yet

- Cash Flow Estimation and Risk Analysis: Answers To Selected End-Of-Chapter QuestionsDocument13 pagesCash Flow Estimation and Risk Analysis: Answers To Selected End-Of-Chapter QuestionsRapitse Boitumelo Rapitse0% (1)

- Sinnott-Armstrong W. (Ed.), Howarth R.B. (Ed.) - Perspectives On Climate Change - Science, Economics, Politics, Ethics, Volume 5 (Advances in The Economics of Environmenal Resources) (2005)Document329 pagesSinnott-Armstrong W. (Ed.), Howarth R.B. (Ed.) - Perspectives On Climate Change - Science, Economics, Politics, Ethics, Volume 5 (Advances in The Economics of Environmenal Resources) (2005)Santos Treviño100% (1)

- R.A. WILLIAMS DISTRIBUTORS LIMITED IPO AnalysisDocument13 pagesR.A. WILLIAMS DISTRIBUTORS LIMITED IPO AnalysisChevonne OatesNo ratings yet

- ValuationDocument53 pagesValuationErmiyas KebedeNo ratings yet

- 1.1 Introduction To Real Estate Markets - With SolutionsDocument27 pages1.1 Introduction To Real Estate Markets - With SolutionsLeon M. EggerNo ratings yet

- IP ValuationDocument6 pagesIP ValuationJahanvi RajNo ratings yet

- Management Control System Tata SteelDocument38 pagesManagement Control System Tata SteelPiyush MathurNo ratings yet

- Fin 4330 Hirak IDocument7 pagesFin 4330 Hirak IMatteo AlbrizioNo ratings yet

- Lecture 11 - Multinational Capital BudgetingDocument11 pagesLecture 11 - Multinational Capital BudgetingTrương Ngọc Minh ĐăngNo ratings yet

- Cost of Capital: © 2019 Mcgraw-Hill Education Limited. All Rights ReservedDocument43 pagesCost of Capital: © 2019 Mcgraw-Hill Education Limited. All Rights Reservedbusiness docNo ratings yet

- Annualized Cost: NPC TheDocument12 pagesAnnualized Cost: NPC TheSupratno ArhamNo ratings yet

- An Introduction To Valuation: Aswath DamodaranDocument40 pagesAn Introduction To Valuation: Aswath DamodaranvinagoyaNo ratings yet

- Stock ValuationDocument7 pagesStock ValuationBrenner BolasocNo ratings yet

- Bva 3Document7 pagesBva 3najaneNo ratings yet

- 28 Vasigh Erfani Aircraft ValueDocument4 pages28 Vasigh Erfani Aircraft ValueW.J. ZondagNo ratings yet