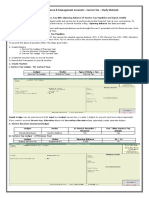

Arrears of Salary - Taxability & Relief Under Section 89

Arrears of Salary - Taxability & Relief Under Section 89

Download as pdf or txt

You might also like

- Fake PaystubDocument1 pageFake PaystubBrandon CarpenterNo ratings yet

- Serv Let ControllerDocument1 pageServ Let ControllerParas PareekNo ratings yet

- Pay Details: Taxable Gross 248.22Document1 pagePay Details: Taxable Gross 248.22ArtemisNo ratings yet

- Payment of Tax, PAYE and Employment IncomeDocument20 pagesPayment of Tax, PAYE and Employment IncomeRavihara D.G.KNo ratings yet

- TaxOptimizer© From TaxSpannerDocument14 pagesTaxOptimizer© From TaxSpanneryeswanthNo ratings yet

- Unit 3 Use of E Tax CalculatorDocument2 pagesUnit 3 Use of E Tax CalculatorSayan MitraNo ratings yet

- Private Limited Complinace PlanDocument5 pagesPrivate Limited Complinace PlanKumar NivasNo ratings yet

- How To Save Tax For FY 2016 17 PDFDocument47 pagesHow To Save Tax For FY 2016 17 PDFsampathkumarNo ratings yet

- Common Errors Made While Filing GST ReturnsDocument4 pagesCommon Errors Made While Filing GST Returnssukumar basuNo ratings yet

- Act, 1964Document9 pagesAct, 1964syed shabbirNo ratings yet

- Returns PDFDocument109 pagesReturns PDFKrishna VamsiNo ratings yet

- Note 2916304 WHT CookbookDocument11 pagesNote 2916304 WHT CookbookSwetha ReddyNo ratings yet

- Auto Tax Calculator Version 15.0 (Blank) FY 2020-21Document18 pagesAuto Tax Calculator Version 15.0 (Blank) FY 2020-21Deepak DasNo ratings yet

- Income Tax - Income Tax Guide 2023, Latest NewsDocument34 pagesIncome Tax - Income Tax Guide 2023, Latest NewsnandiniNo ratings yet

- Session 5 TDSDocument67 pagesSession 5 TDSsinthiakarim17No ratings yet

- Taxguru - In-All About DEFERRED TAX and Its Entry in BooksDocument8 pagesTaxguru - In-All About DEFERRED TAX and Its Entry in Bookskumar45caNo ratings yet

- How To Save Tax For Fy 2018 19Document55 pagesHow To Save Tax For Fy 2018 19Vinit Bhavsar 7No ratings yet

- TAX 2 Group 1 Handout PDFDocument6 pagesTAX 2 Group 1 Handout PDFMi-young SunNo ratings yet

- TAX & VAT Deduct - Bill - GuideDocument47 pagesTAX & VAT Deduct - Bill - GuideRuhul AminNo ratings yet

- Acntng Opng (Document4 pagesAcntng Opng (jkifmaNo ratings yet

- Salary 1Document32 pagesSalary 1Divyansh JalkhareNo ratings yet

- Corporate Accounting AssignmentDocument5 pagesCorporate Accounting AssignmentMd.Mahmudul HasanNo ratings yet

- Solutions For GST Question BankDocument55 pagesSolutions For GST Question BankVarun VardhanNo ratings yet

- Deduction of Tax at Source - Income-Tax Deduction From Salaries Under Section 192 of The Income-Tax Act, 1961 During The Financial Year 2008-2009Document70 pagesDeduction of Tax at Source - Income-Tax Deduction From Salaries Under Section 192 of The Income-Tax Act, 1961 During The Financial Year 2008-2009rhldxmNo ratings yet

- Acct 304 ProjectDocument12 pagesAcct 304 ProjectAryan DasNo ratings yet

- Introduction To The Australian Taxation System and Calculation of Income TaxDocument63 pagesIntroduction To The Australian Taxation System and Calculation of Income TaxNicsNo ratings yet

- Eturns: This Chapter Will Equip You ToDocument52 pagesEturns: This Chapter Will Equip You ToShowkat MalikNo ratings yet

- Base Value TDS VDS As Per Tax Act 2023 & VAT Act 2012 TaebDocument42 pagesBase Value TDS VDS As Per Tax Act 2023 & VAT Act 2012 TaebprashantakpmgNo ratings yet

- Chapter 3 PA IIDocument8 pagesChapter 3 PA IIMule AbuyeNo ratings yet

- Draw A Chart Showin Tax Structure in IndiaDocument55 pagesDraw A Chart Showin Tax Structure in IndiaShubh ShahNo ratings yet

- Solutions For GSTDocument54 pagesSolutions For GSTtannerushivakumar77No ratings yet

- Tax Deducted at SourceDocument5 pagesTax Deducted at SourceRajinder KaurNo ratings yet

- Draw A Chart Showin Tax Structure in IndiaDocument106 pagesDraw A Chart Showin Tax Structure in IndiagamingNo ratings yet

- Naya' Form 3Cd: 1. Non-Compliance With Provisions of Tax Deduction at Source (Clause 27) : Delays andDocument6 pagesNaya' Form 3Cd: 1. Non-Compliance With Provisions of Tax Deduction at Source (Clause 27) : Delays andrakeshca1No ratings yet

- Individual Txation FY 203 24Document44 pagesIndividual Txation FY 203 24Smarty ShivamNo ratings yet

- Nepal TaxDocument7 pagesNepal Taxsanjay kafleNo ratings yet

- Ey Ireland Early Payment of 2020 Excess Randd Tax CreditsDocument5 pagesEy Ireland Early Payment of 2020 Excess Randd Tax CreditsharryNo ratings yet

- New Tax Regime User Guide No Comp Plan Revised1Document14 pagesNew Tax Regime User Guide No Comp Plan Revised1Anantha Krishna ReddyNo ratings yet

- What Next After T.Y. Bcom ?: - Join Our Smart Tax Accountant Course and Have A Job Within 5 MonthsDocument12 pagesWhat Next After T.Y. Bcom ?: - Join Our Smart Tax Accountant Course and Have A Job Within 5 MonthsSONUNo ratings yet

- Comprehensive Guide For Income Tax Returns FY 20-21Document34 pagesComprehensive Guide For Income Tax Returns FY 20-21mayuresh pingale100% (1)

- FTA Guide For New VAT RegistrantDocument24 pagesFTA Guide For New VAT RegistrantNADEEM AKBAR MIRANINo ratings yet

- VAT ReturnsDocument39 pagesVAT ReturnsTaha AhmedNo ratings yet

- Mat and AmtDocument18 pagesMat and AmtParth UpadhyayNo ratings yet

- 2017 - 2018 Supreme Court DecisionsDocument1,412 pages2017 - 2018 Supreme Court DecisionsJerwin DaveNo ratings yet

- Taxation Management Notes Tax Year 2020Document61 pagesTaxation Management Notes Tax Year 2020Ramsha ZahidNo ratings yet

- 3 - Topic 3-2 Introduction To GST in Xero - 3 Xcel FileDocument28 pages3 - Topic 3-2 Introduction To GST in Xero - 3 Xcel FileAnvir Polton BBA GeneralNo ratings yet

- Income TaxDocument4 pagesIncome Tax༒മരിയാർ ഭൂതം-MB༒No ratings yet

- FNSBKG404 7: Activity 2Document2 pagesFNSBKG404 7: Activity 2nattyNo ratings yet

- Module 04 Income Tax Compliance RevisedDocument25 pagesModule 04 Income Tax Compliance RevisedSly BlueNo ratings yet

- VAT Registration in UAEDocument15 pagesVAT Registration in UAETaha AhmedNo ratings yet

- GST Summary Book by CA Yogesh Verma SirDocument90 pagesGST Summary Book by CA Yogesh Verma SirŚańthôsh Ķūmař P100% (1)

- Accounting For Taxes On IncomeDocument18 pagesAccounting For Taxes On IncomeVikas TirmaleNo ratings yet

- Chapter 1 - Introduction To GST: Applicability of Utgst ActDocument7 pagesChapter 1 - Introduction To GST: Applicability of Utgst ActSoul of honeyNo ratings yet

- 16 Summer 2018 BT SADocument8 pages16 Summer 2018 BT SApabloescobar11yNo ratings yet

- Equalisation LevyDocument20 pagesEqualisation LevyAmal P TomyNo ratings yet

- PAYE - A Final Deductions Tax System GuidelineDocument13 pagesPAYE - A Final Deductions Tax System GuidelineKhoabane ManoNo ratings yet

- PEZA Reportorial RequirementsDocument25 pagesPEZA Reportorial RequirementsDarioNo ratings yet

- New Tax Regime User Guide FY - 23-24Document14 pagesNew Tax Regime User Guide FY - 23-24atheena paulsonNo ratings yet

- Relationship Between Tax Compliance and Tax Dispute (Including TP Documentation)Document37 pagesRelationship Between Tax Compliance and Tax Dispute (Including TP Documentation)ryu255No ratings yet

- New Tax Regime User Guide Flexi PlanDocument14 pagesNew Tax Regime User Guide Flexi Planvigneshkumar.prNo ratings yet

- Invoice 18 EmiratesDocument1 pageInvoice 18 Emiratessiva manikandanNo ratings yet

- Accounting Under GST - An InsightDocument6 pagesAccounting Under GST - An InsightABC 123No ratings yet

- Paystubs 03.22.2024 2Document3 pagesPaystubs 03.22.2024 2RangeRoverNo ratings yet

- LescoDocument1 pageLescorizofpicicNo ratings yet

- E-Filing Brief Procedures: Ministry of Revenue Medium Taxpayers' OfficeDocument28 pagesE-Filing Brief Procedures: Ministry of Revenue Medium Taxpayers' OfficeDaniel Kfl100% (1)

- Appu Yadav PDFDocument1 pageAppu Yadav PDFPrakash KolheNo ratings yet

- Effects of Public ExpenditureDocument4 pagesEffects of Public ExpenditureRafiuddin Biplab100% (1)

- Taxes 1Document2 pagesTaxes 1HappyPurpleNo ratings yet

- Nolco QuizDocument5 pagesNolco QuizKendra LorinNo ratings yet

- ICICI Special PricingDocument1 pageICICI Special PricingsouravptuNo ratings yet

- Demerger and Its Tax ImplicationsDocument5 pagesDemerger and Its Tax ImplicationsNidheesh TpNo ratings yet

- Chapter 6: Fringe Benefit Tax: Exercise 6-2: True or False QuestionsDocument9 pagesChapter 6: Fringe Benefit Tax: Exercise 6-2: True or False QuestionsMelady Sison CequeñaNo ratings yet

- Pa Section 4843.1 - Return by Taxpayer - OCRDocument1 pagePa Section 4843.1 - Return by Taxpayer - OCRBlaiberteNo ratings yet

- Reply To OA - 1.4.2024 - 9pmDocument28 pagesReply To OA - 1.4.2024 - 9pmkabilanNo ratings yet

- TATA 1MG Healthcare Solutions Private Limited: Nagar 1 ST Road,, Chennai, 600126, IndiaDocument1 pageTATA 1MG Healthcare Solutions Private Limited: Nagar 1 ST Road,, Chennai, 600126, IndiaKumaran KingNo ratings yet

- Payroll WorksheetDocument2 pagesPayroll WorksheetGena Duresa100% (1)

- CAF2-Tax Changes by FarazDocument2 pagesCAF2-Tax Changes by Farazbroken GMDNo ratings yet

- JioMart Invoice 1700300012886Document1 pageJioMart Invoice 1700300012886shrishti guptaNo ratings yet

- OD429354308202337100Document1 pageOD429354308202337100Md.gulamNo ratings yet

- Asirvad CPVC Pipes and FittingsDocument3 pagesAsirvad CPVC Pipes and FittingsRICH DAD POOR DADNo ratings yet

- Chapter 3Document14 pagesChapter 3Fethi ADUSSNo ratings yet

- Taxation 1 ReviewerDocument5 pagesTaxation 1 ReviewerEISEN BELWIGANNo ratings yet

- Form-Ii (See Regulation 4) Postal Bill of Export - II (To Be Submitted in Duplicate)Document1 pageForm-Ii (See Regulation 4) Postal Bill of Export - II (To Be Submitted in Duplicate)mrthilagamNo ratings yet

- Direct Tax: Multiple Choice QuestionsDocument27 pagesDirect Tax: Multiple Choice QuestionsAyushman PatnaikNo ratings yet

- Paystub RealDocument1 pagePaystub Realmakeweim1ngNo ratings yet

- Aushadhidham 2074Document1 pageAushadhidham 2074K D HERBAL & UNANINo ratings yet

- Iesco Online BillDocument1 pageIesco Online BillURDU BHAINo ratings yet