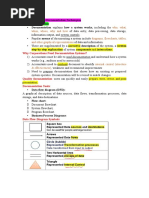

Group 2

Group 2

Download as pdf or txt

You might also like

- Chapter 3 Systems Documentation TechniquesDocument6 pagesChapter 3 Systems Documentation TechniquesChenyi Gu100% (1)

- Ais Chapter 6Document15 pagesAis Chapter 6lyzel kayeNo ratings yet

- Ais-Documenting Accounting Information SystemDocument23 pagesAis-Documenting Accounting Information SystemHarold Dela Fuente100% (1)

- FlowchartsDocument6 pagesFlowchartsIna PascariNo ratings yet

- Foundational Concepts of The AISDocument3 pagesFoundational Concepts of The AISNikki RunesNo ratings yet

- Prepare and Interpret Technical DrawingDocument5 pagesPrepare and Interpret Technical DrawingDwin Rosco75% (4)

- Flow Chart of A Management SystemDocument7 pagesFlow Chart of A Management SystemScribdTranslationsNo ratings yet

- AIS Chapter 3Document38 pagesAIS Chapter 3bisrattesfaye100% (1)

- Flowchart DiagramDocument11 pagesFlowchart Diagramhafsatbashir04No ratings yet

- Flowchart TechniquesDocument2 pagesFlowchart TechniquesVijay GondhaleNo ratings yet

- Order 887074 FinalDocument7 pagesOrder 887074 Finalmeglain11No ratings yet

- Tools For Quality ImprovementDocument64 pagesTools For Quality Improvementmuzammil21_adNo ratings yet

- FlowchartDocument25 pagesFlowchartMichelle Anne Dalupang DayagNo ratings yet

- Mid-II Important QsDocument20 pagesMid-II Important QsPratik AdhikaryNo ratings yet

- Flowchart For Computer ScienceDocument6 pagesFlowchart For Computer ScienceVengaiChisevaNo ratings yet

- FlowchartsDocument13 pagesFlowchartsAkhila SNo ratings yet

- Screenshot 2023-12-08 at 9.53.18 AMDocument22 pagesScreenshot 2023-12-08 at 9.53.18 AMMdyasinhridoy846No ratings yet

- Analysis of Techniques For Procedure DesignDocument19 pagesAnalysis of Techniques For Procedure DesignScribdTranslationsNo ratings yet

- Process MappingDocument4 pagesProcess MappinganurajNo ratings yet

- Flow Charts: Symbols: Start or End of The ProgramDocument5 pagesFlow Charts: Symbols: Start or End of The ProgramAshwani RanaNo ratings yet

- Chapter Three AISDocument9 pagesChapter Three AISmohammedNo ratings yet

- FlowchartDocument8 pagesFlowchartlacsonaltheamargarett28No ratings yet

- Chapter 29Document9 pagesChapter 29Samonte JemimahNo ratings yet

- Primary Documentation Methods (Cont'd)Document13 pagesPrimary Documentation Methods (Cont'd)Reggie de CastroNo ratings yet

- Data Analysis Analyzing Data - Flowcharting: Return To Table of ContentsDocument3 pagesData Analysis Analyzing Data - Flowcharting: Return To Table of ContentsApam BenjaminNo ratings yet

- A System Flowchart Is A ConcreteDocument2 pagesA System Flowchart Is A Concretemonikakothari1No ratings yet

- What Is A Process FlowchartDocument6 pagesWhat Is A Process FlowchartAnonymous icVUXalaVNo ratings yet

- Flow Chart Definition: What Is FlowchartDocument9 pagesFlow Chart Definition: What Is FlowchartRamakrishna KaturiNo ratings yet

- Mba - Iii Sem Internal Audit & Control - MF0004 Set - 2Document26 pagesMba - Iii Sem Internal Audit & Control - MF0004 Set - 2Dilipk86No ratings yet

- Tutorial G04: Using Charts and Diagrams: By: Jonathan ChanDocument5 pagesTutorial G04: Using Charts and Diagrams: By: Jonathan Changnu_linuxaholicNo ratings yet

- Chapter 6 Flowcharting RTRTDocument18 pagesChapter 6 Flowcharting RTRTredearth292950% (2)

- (Compressed) Process Defined ApplicationDocument2 pages(Compressed) Process Defined Applicationvsquare55No ratings yet

- Flow Chart DefinitionDocument9 pagesFlow Chart DefinitionFarooqNo ratings yet

- Tools For Quality ImprovementDocument65 pagesTools For Quality ImprovementThiago LealNo ratings yet

- Flowcharts: Rajesh P Mca Iii Sem Bangalore UniversityDocument16 pagesFlowcharts: Rajesh P Mca Iii Sem Bangalore UniversityYuvraj ReddyNo ratings yet

- 016 Health Care Quality ToolsDocument6 pages016 Health Care Quality ToolsphilipNo ratings yet

- Flow ChartDocument3 pagesFlow ChartAbdul MajidNo ratings yet

- Seven Traditional Tools of QualityDocument12 pagesSeven Traditional Tools of QualitySenthil KumarNo ratings yet

- General Form TheoryDocument31 pagesGeneral Form TheoryScribdTranslationsNo ratings yet

- Chap 3Document5 pagesChap 3Kathrina Mae GulmaticoNo ratings yet

- Flow ChartDocument7 pagesFlow ChartMuhammad Atif Qaim KhaniNo ratings yet

- C 3 Ystems Ocumentation EchniquesDocument21 pagesC 3 Ystems Ocumentation EchniquesMahmoud AhmedNo ratings yet

- AIS Chapter 5Document1 pageAIS Chapter 5Fran PranNo ratings yet

- Accounting Information Systems: Study Smarter. Welcome, Guest!Document11 pagesAccounting Information Systems: Study Smarter. Welcome, Guest!complicatedsolNo ratings yet

- Accounting Information SystemDocument55 pagesAccounting Information SystemRodNo ratings yet

- Statistical Process Control For Quality ImprovementDocument8 pagesStatistical Process Control For Quality ImprovementAhmed IsmailNo ratings yet

- ch06 Accounting Systems Solution ManualDocument20 pagesch06 Accounting Systems Solution ManualLindsey Clair Royal80% (5)

- Bethany Labrador Bsit-A1: 1. What Are The Advantages of Using Flowchart?Document9 pagesBethany Labrador Bsit-A1: 1. What Are The Advantages of Using Flowchart?BETHANY LABRADORNo ratings yet

- Accounting Information SystemDocument5 pagesAccounting Information Systemaccajay2350% (2)

- Private Bus Hire: 16th June To 30th SeptemberDocument6 pagesPrivate Bus Hire: 16th June To 30th Septemberpanku_80No ratings yet

- TQM Unit 3 7 1 Tools of Quality NewDocument58 pagesTQM Unit 3 7 1 Tools of Quality NewtamilselvansambathNo ratings yet

- FlowchartDocument3 pagesFlowchartMarivic CastillanoNo ratings yet

- Practice Essay QuestionsDocument3 pagesPractice Essay QuestionsKezia SantosidadNo ratings yet

- Mysap Fi Fieldbook: Fi Fieldbuch Auf Der Systeme Anwendungen Und Produkte in Der DatenverarbeitungFrom EverandMysap Fi Fieldbook: Fi Fieldbuch Auf Der Systeme Anwendungen Und Produkte in Der DatenverarbeitungRating: 4 out of 5 stars4/5 (1)

- The Book of Choice: “The Roadmap to Better Documentation and Process Mapping”From EverandThe Book of Choice: “The Roadmap to Better Documentation and Process Mapping”No ratings yet

- 79669-Article Text-187416-1-10-20120727Document13 pages79669-Article Text-187416-1-10-20120727Analou LopezNo ratings yet

- History 42Document39 pagesHistory 42Analou LopezNo ratings yet

- Filipino TraditionsDocument7 pagesFilipino TraditionsAnalou LopezNo ratings yet

- Group 3 Report FinalDocument25 pagesGroup 3 Report FinalAnalou LopezNo ratings yet

- Group 5Document33 pagesGroup 5Analou LopezNo ratings yet

- Ias MergedDocument157 pagesIas MergedAnalou LopezNo ratings yet

- 2 Corporation Accounting Share Capital TransactionsDocument7 pages2 Corporation Accounting Share Capital TransactionsAnalou LopezNo ratings yet

- Share CapitalDocument43 pagesShare CapitalAnalou LopezNo ratings yet

- The International Monetary SystemDocument4 pagesThe International Monetary SystemAnalou LopezNo ratings yet

- Accounting For Corporations: Mcgraw-Hill/Irwin1 © The Mcgraw-Hill Companies, Inc., 2006Document67 pagesAccounting For Corporations: Mcgraw-Hill/Irwin1 © The Mcgraw-Hill Companies, Inc., 2006Analou LopezNo ratings yet

- Accounting Teaching DemoDocument29 pagesAccounting Teaching DemoAnalou LopezNo ratings yet

- MASs NOTESDocument14 pagesMASs NOTESAnalou LopezNo ratings yet

- Onerous ContractfinaleDocument8 pagesOnerous ContractfinaleAnalou LopezNo ratings yet

- Mas Notes 2Document8 pagesMas Notes 2Analou LopezNo ratings yet

- IAS 37 Onerous ContractsDocument7 pagesIAS 37 Onerous ContractsAnalou LopezNo ratings yet

- OBE AUDITING and Assurance Principle SYLLABUSDocument13 pagesOBE AUDITING and Assurance Principle SYLLABUSAnalou LopezNo ratings yet