Pgold

Pgold

Download as docx, pdf, or txt

You might also like

- TOWs and SpaceDocument3 pagesTOWs and Spacesyeda ramshaNo ratings yet

- SMC Company ProfileDocument2 pagesSMC Company ProfileAldrin CabangbangNo ratings yet

- 2Document9 pages2Murali GopalanNo ratings yet

- CPM and Porters 5 ForcesDocument10 pagesCPM and Porters 5 ForcesGeloApostolNo ratings yet

- Running Head: Vertical Integration of Zhangzidao 1Document8 pagesRunning Head: Vertical Integration of Zhangzidao 1DenizNo ratings yet

- Case 3: Culture Gap: ReferenceDocument2 pagesCase 3: Culture Gap: Referencerizalyn leritNo ratings yet

- PrulifeDocument30 pagesPrulifeJ'Carlo CarpioNo ratings yet

- Puregold'S Strategy: Company DescriptionDocument32 pagesPuregold'S Strategy: Company DescriptionLeighgendary CruzNo ratings yet

- PuregoldDocument9 pagesPuregoldCarmina BacunganNo ratings yet

- The Impact of Tertiary Education To The Employment Rate in The PhilippinesDocument4 pagesThe Impact of Tertiary Education To The Employment Rate in The PhilippinesTrish BernabeNo ratings yet

- Pure GoldDocument5 pagesPure GoldKeithlyn KellyNo ratings yet

- Dua Ghani 23131: Supermarket WarehousingDocument3 pagesDua Ghani 23131: Supermarket WarehousingDuaNo ratings yet

- Supermarkets in The Philippines AnalysisDocument2 pagesSupermarkets in The Philippines AnalysisAndrea YvestroNo ratings yet

- Case Study Puregold and SavemoreDocument54 pagesCase Study Puregold and SavemoreJIng JhingNo ratings yet

- Dela Cruz4aomfinalpaperDocument98 pagesDela Cruz4aomfinalpaperDesmond WilliamsNo ratings yet

- Proposed Strategic Plan For San Miguel Food and Beverage Inc. BSBA HRM 3BDocument31 pagesProposed Strategic Plan For San Miguel Food and Beverage Inc. BSBA HRM 3BRoan James TolentinNo ratings yet

- PUREGOLD Marygracerizza Mae RizzalieDocument3 pagesPUREGOLD Marygracerizza Mae RizzalieRizza Mae CabigasNo ratings yet

- PESTLE Analysis of SingaporeDocument3 pagesPESTLE Analysis of Singaporejason LuvNo ratings yet

- Mascarina - Final Strama PaperDocument106 pagesMascarina - Final Strama Paperjuzzcam.14No ratings yet

- Econ Midterm MontereyDocument3 pagesEcon Midterm MontereyArnold NiangoNo ratings yet

- New Era University: International Business PlanDocument50 pagesNew Era University: International Business PlanNesly Ascaño CordevillaNo ratings yet

- Social Venture Plan PDFDocument15 pagesSocial Venture Plan PDFJowanna Clairusse Castillo NambioNo ratings yet

- Sample Outline of A Strama PaperDocument1 pageSample Outline of A Strama PaperErica CaliuagNo ratings yet

- Balance ScorecardDocument2 pagesBalance ScorecardNorie FernandezNo ratings yet

- Production Management-Final Combined)Document14 pagesProduction Management-Final Combined)Ronnie GutierrezNo ratings yet

- De Guzman-Rose Ann-UrcDocument5 pagesDe Guzman-Rose Ann-UrcRose Ann De GuzmanNo ratings yet

- Strama Paper Finalcopy 1 10 PDF FreeDocument136 pagesStrama Paper Finalcopy 1 10 PDF FreeMichelle AquinoNo ratings yet

- Manila Bulletin Publishing Corporation Sec Form 17a 2018Document128 pagesManila Bulletin Publishing Corporation Sec Form 17a 2018Kathryn SantosNo ratings yet

- Accounting 2 FinalDocument21 pagesAccounting 2 Finalapi-3731801No ratings yet

- CH 12Document49 pagesCH 12Natasya SherllyanaNo ratings yet

- URC Risk ManagementDocument3 pagesURC Risk ManagementAngel Mingo ManahanNo ratings yet

- San Miguel Pure Foods CompanyDocument4 pagesSan Miguel Pure Foods CompanyErica Mae VistaNo ratings yet

- Strama 1 QuizDocument3 pagesStrama 1 QuizMark Roger II HuberitNo ratings yet

- Market Feasibility Puregold SupermarketDocument24 pagesMarket Feasibility Puregold SupermarketPrincess MarceloNo ratings yet

- International MarketingDocument6 pagesInternational MarketingJeff RamosNo ratings yet

- Mercury Drug CorporationDocument5 pagesMercury Drug CorporationLiDdy Cebrero Belen0% (1)

- DocstestingnielDocument67 pagesDocstestingnielelrosimo100% (2)

- Shell Ems - EditedDocument14 pagesShell Ems - EditedGeovanie LauraNo ratings yet

- Mini STRAMA Paper OutlineDocument11 pagesMini STRAMA Paper OutlineViancaNo ratings yet

- Aboitizpower Believes in The Power of BalanceDocument18 pagesAboitizpower Believes in The Power of BalanceHaclOo BongcawilNo ratings yet

- Strama C1Document6 pagesStrama C1Renée Kristen CortezNo ratings yet

- FinalsDocument3 pagesFinalsapi-535591806No ratings yet

- ActivityDocument2 pagesActivityDaniela AvelinoNo ratings yet

- Swot Analysis Questionnaire First Interviewee (PNB)Document21 pagesSwot Analysis Questionnaire First Interviewee (PNB)Dezza Mae GantongNo ratings yet

- BBFriendsCo StraMa PaperDocument135 pagesBBFriendsCo StraMa PaperChristine Joy MauroNo ratings yet

- Value Chain Analysis of LICDocument7 pagesValue Chain Analysis of LICROHIT KUMAR SINGHNo ratings yet

- Phoenix Petroleum PhilippineDocument2 pagesPhoenix Petroleum PhilippinetwometersNo ratings yet

- TNT PestleDocument2 pagesTNT PestleArshad AzeemNo ratings yet

- Final StramaDocument75 pagesFinal StramaChristian Jay Patiño Orpano100% (1)

- Danica StramaDocument5 pagesDanica StramaDanica GabuatNo ratings yet

- Case Study No. 2 - International BusinessDocument4 pagesCase Study No. 2 - International BusinessJullie Kaye Frias DiamanteNo ratings yet

- (PNB) Company BackgroundDocument1 page(PNB) Company BackgroundAlbert Ocno Almine100% (2)

- Vista LandDocument2 pagesVista LandDPS1911No ratings yet

- Jollibee'S Value Chan Analysis: InfrastructureDocument1 pageJollibee'S Value Chan Analysis: InfrastructureAlexandria EvangelistaNo ratings yet

- McDonalds & BK Case Study 2Document10 pagesMcDonalds & BK Case Study 2Babar100% (2)

- 2014 Sarap Sample StramaDocument82 pages2014 Sarap Sample StramaAnonymous ic2CDkF0% (1)

- JFC Case StudyDocument66 pagesJFC Case StudyJulianna GomezNo ratings yet

- Lazada Case StudyDocument2 pagesLazada Case StudyJanine Caldito100% (1)

- CC StramaDocument40 pagesCC Stramaamcagirl100% (2)

- CSR of DMCI HoldingsDocument5 pagesCSR of DMCI HoldingsChloe JangNo ratings yet

- 1. Topic 1 Introduction to Entrepreneurship_newDocument41 pages1. Topic 1 Introduction to Entrepreneurship_newdonnaNo ratings yet

- Winning Markets Through Market-Oriented Strategic PlanningDocument25 pagesWinning Markets Through Market-Oriented Strategic PlanningPhD ScholarNo ratings yet

- Intro S4HANA Using Global Bike Case Study CO-PC II en v4.1Document59 pagesIntro S4HANA Using Global Bike Case Study CO-PC II en v4.1soncss150387No ratings yet

- ACCA SBL Chap 1Document42 pagesACCA SBL Chap 1JoeyNo ratings yet

- SPPU Question Paper On Global-Strategic-Management Pattern-2019Document2 pagesSPPU Question Paper On Global-Strategic-Management Pattern-2019Sandeep ChaudharyNo ratings yet

- Harley Davidson Stock ValuationDocument43 pagesHarley Davidson Stock ValuationRahul PatelNo ratings yet

- Critical Thinking and Discussion Questions: Closing CaseDocument2 pagesCritical Thinking and Discussion Questions: Closing CaseDiana Cueva RamosNo ratings yet

- Paps 1004Document30 pagesPaps 1004Erica BueNo ratings yet

- Sample Audit ProgramDocument9 pagesSample Audit ProgramDanErwinMayoNo ratings yet

- A Comprehensive Project ReportDocument29 pagesA Comprehensive Project ReportRishu Pagrotra50% (2)

- Finalterm Examination in SS113 Entrep MindDocument3 pagesFinalterm Examination in SS113 Entrep MindLODELYN B. CAGUILLO100% (1)

- Understanding Customer Needs and Wants - AayushiAgarwalDocument5 pagesUnderstanding Customer Needs and Wants - AayushiAgarwalAayushi AgarwalNo ratings yet

- Elective 1Document2 pagesElective 1Cedie Gonzaga Alba100% (1)

- Brand Is A Product, Service, or Concept That Is Publicly Distinguished From Other ProductsDocument7 pagesBrand Is A Product, Service, or Concept That Is Publicly Distinguished From Other ProductsZarin EshaNo ratings yet

- Financial Theory and Corporate Policy - Copeland.449-493Document45 pagesFinancial Theory and Corporate Policy - Copeland.449-493Claire Marie ThomasNo ratings yet

- Rosewood Hotels and ResortsDocument5 pagesRosewood Hotels and Resortskhushi kumari100% (1)

- Olive OilDocument28 pagesOlive Oilalassadi09No ratings yet

- CSR Case Study of Tommy Hilfiger CompanyDocument15 pagesCSR Case Study of Tommy Hilfiger CompanyPrincess Aleia SalvadorNo ratings yet

- Week 4 - Segmenting, Targeting, and PositioningDocument20 pagesWeek 4 - Segmenting, Targeting, and PositioningShubhangi NigamNo ratings yet

- Starbucks Business Case StudyDocument11 pagesStarbucks Business Case StudyJenzen TseNo ratings yet

- Chapter 7 PPT Version 2Document61 pagesChapter 7 PPT Version 2islamasifNo ratings yet

- Chapter 11. VariancesDocument2 pagesChapter 11. Varianceskataraiti.koraingNo ratings yet

- IBDP Macroeconomics 3.2docxDocument21 pagesIBDP Macroeconomics 3.2docxSandeep SudhakarNo ratings yet

- Review Jurnal PDFDocument25 pagesReview Jurnal PDFTantriiNo ratings yet

- What Is The Right Supply Chain For Your Product?Document2 pagesWhat Is The Right Supply Chain For Your Product?rjaliawala100% (4)

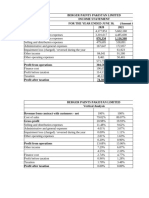

- Bergers Paints Pakistan Ltd (Financial Analysis)Document20 pagesBergers Paints Pakistan Ltd (Financial Analysis)rizwansyedali653No ratings yet

- IMC ReportDocument95 pagesIMC ReportNGOC Nguyen The MinhNo ratings yet

- Title IXDocument4 pagesTitle IXDJ ULRICHNo ratings yet

- Tutorial 6 Job Batch CostingDocument6 pagesTutorial 6 Job Batch CostingYANG YUN RUINo ratings yet

- Rural - Online 2 - SynopsisDocument14 pagesRural - Online 2 - SynopsisJignesh RathodNo ratings yet